FIRE Planning for IT Professionals in India: The Career Cliff Changes Everything

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

12 May 2026

Retiring at 40 is possible, but it requires more than investing in a few high-performing mutual funds. You need a high savings rate, a realistic corpus, adequate protection and a withdrawal strategy designed to last potentially 45 to 50 years.

Quick answer: As a starting estimate, someone retiring at 40 may need approximately 30 to 40 times their annual expenses at retirement. A household spending ₹1 lakh per month in today's money may need roughly ₹3.6 to ₹4.8 crore in today's value, excluding children's education, a house purchase, healthcare reserves and other major goals.

Retiring at 40 does not necessarily mean that you will never work again. It means reaching a level of financial independence where employment becomes optional. Your investments and other income sources should support your lifestyle without depending on a monthly salary.

Stop working completely, move to a lower-stress career or take extended career breaks.

Consult, start a business, travel or spend more time on family and personal interests.

This is the central idea behind FIRE: Financial Independence, Retire Early. The exact amount you need depends on your age, lifestyle, inflation, existing investments, taxes, retirement duration and willingness to earn some income after 40.

Yes, but it is financially demanding because the accumulation period is short and the withdrawal period is unusually long. Someone retiring at 60 may need to fund 25 to 30 years of expenses. If you retire at 40 and live until 90, your portfolio must support around 50 years without a regular salary.

A commonly used retirement formula is:

The popular 4% rule converts this into:

However, the 4% rule was developed using historical US market data and was primarily studied for retirement periods of approximately 30 years. A person retiring at 40 may need the portfolio to last considerably longer.

| Withdrawal rate | Corpus multiplier | Planning interpretation |

|---|---|---|

| 4% | 25x annual expenses | Common starting rule |

| 3.33% | 30x annual expenses | More conservative |

| 2.86% | 35x annual expenses | Wider long-retirement buffer |

| 2.5% | 40x annual expenses | High margin of safety |

The table below shows the approximate corpus required if you were retiring today.

| Monthly expenses | Annual expenses | 25x | 30x | 35x | 40x |

|---|---|---|---|---|---|

| ₹50,000 | ₹6 lakh | ₹1.50 cr | ₹1.80 cr | ₹2.10 cr | ₹2.40 cr |

| ₹75,000 | ₹9 lakh | ₹2.25 cr | ₹2.70 cr | ₹3.15 cr | ₹3.60 cr |

| ₹1 lakh | ₹12 lakh | ₹3 cr | ₹3.60 cr | ₹4.20 cr | ₹4.80 cr |

| ₹1.5 lakh | ₹18 lakh | ₹4.50 cr | ₹5.40 cr | ₹6.30 cr | ₹7.20 cr |

| ₹2 lakh | ₹24 lakh | ₹6 cr | ₹7.20 cr | ₹8.40 cr | ₹9.60 cr |

These figures are in today's value. If age 40 is several years away, first adjust current expenses for inflation. They also exclude separate goals such as buying a house, children's education, weddings, dependent parents, major healthcare costs and business capital.

Suppose you are 30, currently spend ₹1 lakh per month and want to retire at 40. At 6% annual inflation, your projected monthly expense at 40 would be:

Your annual expense at age 40 would be approximately ₹21.49 lakh.

This is why multiplying today's expenses by 25 can underestimate the amount required at your retirement date. Inflation also continues after retirement, so a meaningful part of the portfolio must keep growing.

Model your expenses, current portfolio, retirement age and expected inflation.

Use FIRE CalculatorDecide where you will live, whether you will own or rent, how often you expect to travel and whether you intend to work occasionally. Use 12 months of bank and card statements rather than guessing.

Housing, groceries, utilities, transport, insurance and regular healthcare.

Dining, subscriptions, hobbies, domestic help and personal purchases.

Home repairs, appliances, vehicle replacement and family events.

International travel, expensive hobbies, luxury purchases and giving.

Your FIRE corpus should support recurring retirement expenses. Large one-time goals need separate funding.

| Goal | How to treat it |

|---|---|

| Regular household expenses | Include in FIRE corpus |

| Annual travel | Include if recurring |

| Children's education or wedding | Build a separate corpus |

| House purchase or business capital | Build a separate corpus |

| Parent healthcare or medical contingency | Create a separate provision |

Do not rely on one exact FIRE number. Create minimum, target and comfortable scenarios.

Controlled expenses, flexibility in weak markets and some potential part-time income.

Your expected lifestyle using reasonable inflation and return assumptions.

A larger buffer for healthcare, longevity, travel and unexpected expenditure.

Check the plan under good, average and poor market-return scenarios.

Consider a 30-year-old with ₹1 lakh of current monthly expenses, a 6% inflation assumption, no existing investments and a target of 35 times annual expenses at age 40.

This is illustrative. Actual returns will not arrive evenly. If the required investment is not affordable, increase income, reduce the target lifestyle, use annual step-ups, extend retirement to 45 or consider partial retirement.

Use the SIP Calculator to model monthly contributions and the Retirement Calculator for a conventional retirement scenario.

Assume ₹1 lakh of current monthly expenses, 6% inflation, a 35x corpus and a 10% accumulation return.

| Starting age | Years until 40 | Expenses at 40 | Target corpus | Monthly investment |

|---|---|---|---|---|

| 25 | 15 years | ₹2.40 lakh | ₹10.07 cr | ₹2.41 lakh |

| 30 | 10 years | ₹1.79 lakh | ₹7.52 cr | ₹3.64 lakh |

| 35 | 5 years | ₹1.34 lakh | ₹5.62 cr | ₹7.20 lakh |

An earlier start gives your investments more time to compound and leaves more room to correct mistakes.

A FIRE portfolio needs growth before retirement and stability as retirement approaches. It may combine diversified domestic equity, suitable international exposure, high-quality fixed income, EPF or PPF, limited gold and cash for near-term needs.

Retiring at 40 may require investing 40 to 70% of take-home income, depending on your age, income and existing assets. Focus first on housing, vehicles, education, lifestyle upgrades, vacations and debt.

Cost control should be intentional, not a lifetime of deprivation. A FIRE plan that makes your working years miserable is unlikely to remain sustainable.

Prioritise credit-card balances, personal loans, consumer loans and expensive vehicle debt. A manageable home loan does not always require immediate repayment, but entering retirement without large mandatory EMIs gives you more flexibility during market downturns.

Build personal cover independent of your employer, consider a super top-up and create a separate medical reserve.

Maintain appropriate cover while dependants rely on your income or future financial contributions.

Your earning ability is a major asset during accumulation. Disability can disrupt the plan without causing death.

Check waiting periods, exclusions, deductibles, room-rent conditions and claim requirements.

The order of returns matters when you are withdrawing money. A major decline immediately after retirement can force you to sell more units at depressed prices, permanently weakening the portfolio. This risk is most dangerous during the first five to ten years.

Approximately 2 to 3 years of essential expenses in suitable low-volatility and liquid assets.

Money required over roughly years 4 to 10, using suitable high-quality debt and hybrid assets.

Assets for expenses more than ten years away, retaining meaningful equity exposure for growth.

Replenish and rebalance the buckets periodically rather than treating the setup as permanent.

Explore how withdrawals may work using the SWP Calculator.

Usable retirement income is what remains after tax, investment costs and inflation. Your strategy should determine which account to use first, when to realise gains, how to rebalance tax-efficiently and how locked retirement assets fit into early retirement.

Irregular costs, repairs, premiums and family support are frequently missed.

The 4% rule is a historical framework, not a promise of indefinite portfolio survival.

A plan requiring 15% every year has little margin for volatility or error.

Medical costs can rise differently from general household inflation.

Using the retirement corpus for education, weddings or property weakens sustainability.

Test whether the plan works after a 25 to 30% fall in the equity component.

One property, employer stock, small-cap portfolio or business creates concentration risk.

Work supplies routine, identity and social interaction. Retirement must replace them thoughtfully.

If full retirement at 40 requires an unrealistic corpus, financial independence can still be approached gradually. Finnovate's guide to the types of FIRE in India explains these paths in more detail.

Your existing investments can potentially grow into a conventional retirement corpus while you earn only for current expenses.

Investments cover part of your expenses while flexible or part-time work covers the rest.

You retire with a controlled lifestyle and relatively low recurring expenses.

You build a larger corpus for higher spending, travel and a wider margin of safety.

For many professionals, flexible work after 40 is more practical than eliminating earned income completely. Even ₹50,000 of monthly consulting income can materially reduce early withdrawals.

Before leaving your job permanently, test the plan for 6 to 12 months.

₹5 crore may be sufficient for some households and inadequate for others.

Sustainability depends on longevity, asset allocation, tax, housing, healthcare, family responsibilities, spending flexibility and potential part-time income. Read the detailed analysis: Is ₹5 crore enough to retire?

Retiring at 40 in India is possible, but it is not achieved through one product, one mutual fund or one simple formula.

Start by calculating inflation-adjusted annual expenses. Evaluate a range of approximately 30 to 40 times those expenses rather than treating 25x as a guaranteed answer. Then add separate provisions for healthcare, housing, children and other major goals.

Your strategy must address both sides of retirement: accumulating the corpus and withdrawing from it safely. High savings, diversified investments, adequate insurance, tax planning and flexibility during weak markets matter more than chasing the highest return.

Retirement is not determined by whether you have ₹2 crore, ₹5 crore or ₹10 crore. It is determined by whether your assets can reliably support the life you want for as long as you may live.

Review the corpus, withdrawal strategy, healthcare buffer and investment structure together.

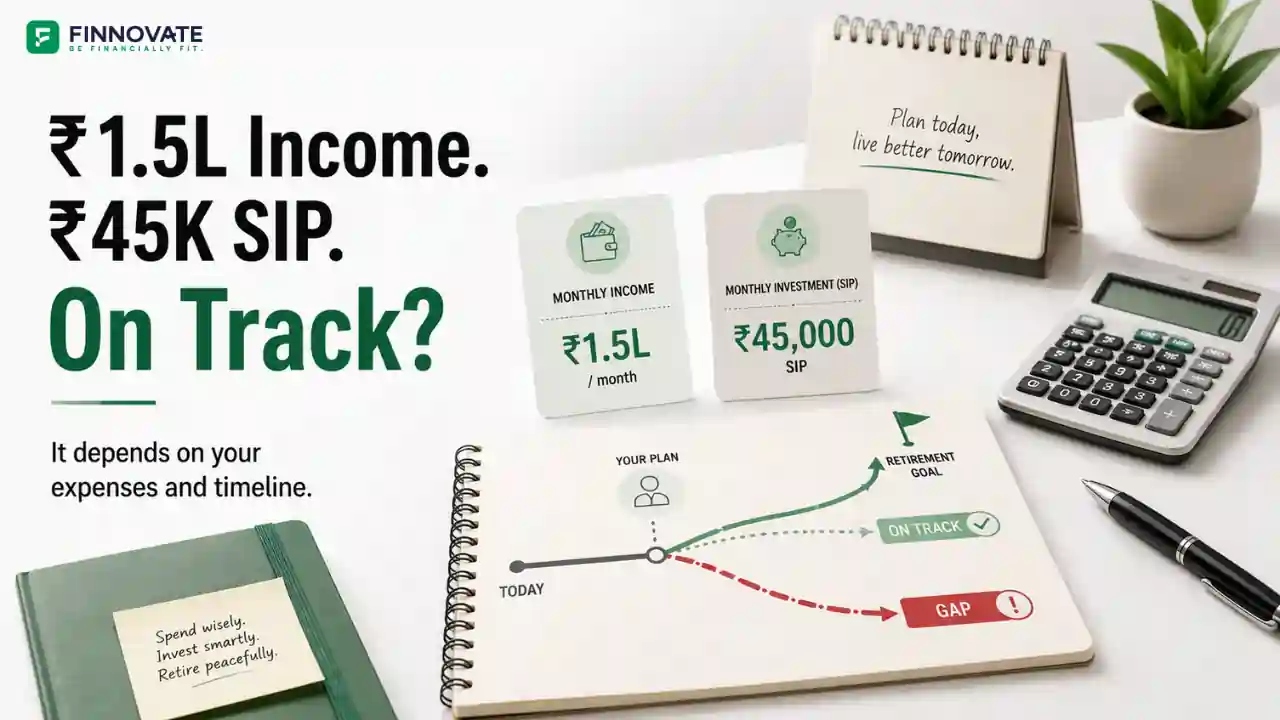

Explore Retirement PlanningA starting range is approximately 30 to 40 times your inflation-adjusted annual expenses at retirement. Someone needing ₹12 lakh annually may require roughly ₹3.6 to ₹4.8 crore in today's value, excluding separate goal and healthcare corpuses.

The 25x rule assumes a 4% initial withdrawal rate and is a useful starting point. However, retiring at 40 may create a 45 to 50 year withdrawal period, so a more conservative multiplier, spending flexibility and detailed scenario testing may be necessary.

It depends on your current age, target corpus, existing investments and expected return. For illustration, a 30-year-old targeting ₹7.52 crore in ten years from zero would need to invest approximately ₹3.64 lakh per month at an assumed 10% annual return.

At a 3% initial withdrawal rate, ₹3 crore supports approximately ₹9 lakh annually before tax. It may work for a low-cost lifestyle with controlled housing expenses, but may be insufficient for a high-expense urban household or significant family obligations.

For most households, ₹1 crore is unlikely to fund a complete 45 to 50 year retirement. At a 3% withdrawal rate, it provides approximately ₹3 lakh annually before tax. It may instead support Coast FIRE, Barista FIRE or partial financial independence.

There is no single best investment. A FIRE portfolio usually needs diversified equity for long-term growth, high-quality fixed income for stability, liquidity for near-term expenses and appropriate insurance for protection.

Entering retirement without large EMIs improves flexibility. However, immediate repayment is not always financially optimal. Consider the loan's cost, tax treatment, remaining tenure, liquidity and your comfort with debt.

A self-occupied house should not automatically be counted as spendable FIRE corpus because it does not directly fund monthly expenses. Include it only if you have a practical plan to sell, downsize, rent it out or otherwise generate income from it.

Review it at least annually and after major changes in income, expenses, family responsibilities, tax rules, health or market conditions. Recalculate the corpus as your lifestyle becomes clearer.

This article is for educational purposes only. All calculations are illustrative and do not represent guaranteed returns or a universally safe withdrawal rate. Investment returns, inflation and tax rules may differ from the assumptions used. Please consider consulting a SEBI-registered investment adviser and qualified tax professional before making retirement or investment decisions.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

Rs 45,000 on Rs 1.5 lakh salary is a 30% savings rate. But is it enough? See corpus built ...

Use this practical framework to check if you’re ready for early retirement in India. Cov...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...