FIRE in India Explained: Meaning, Math & How to Start

Understand what FIRE means, the mathematics behind it, and practical steps to get started on your financial independence journey.

Financial Independence, Retire Early - find your number and the savings path to get there.

Your F.I.R.E Number at Age 55

Calculating...

Your numbers are clear. Now build a strategy.

A planner can help you close this gap with a plan built around your life.

Talk to a plannerWealth Trajectory

Monthly Income at Retirement

—

per month at retirement age

Your Money Lasts Until

—

based on your savings plan

Years of Financial Freedom

—

from retirement to horizon

FIRE stands for Financial Independence, Retire Early. At its core, it is a personal finance approach where you build enough wealth to cover your living expenses for life, so that work becomes a choice rather than a necessity.

In India, the idea is gaining serious traction. Whether you want to quit the corporate grind at 45, shift to part-time work, start a business without financial pressure, or simply know you could stop working anytime without panic, FIRE gives you that number and a path to reach it.

Your FIRE number is the exact corpus you need. Once you know it, every investment decision gets sharper. You stop guessing and start moving with purpose.

Your FIRE number is the total retirement corpus that, when invested, generates enough returns to cover all your living expenses without you ever touching the principal.

The formula is straightforward:

The corpus at which a 4% annual withdrawal covers all retirement expenses indefinitely, without depleting the principal.

This is based on the 4% Safe Withdrawal Rate, which means you can withdraw 4% of a well-invested corpus each year without depleting it over a 30-year retirement. Multiplying by 25 is mathematically the same as dividing by 4%.

Quick example: If your monthly expenses at retirement will be ₹1.5 lakh (₹18 lakh/year), your FIRE Number = ₹18,00,000 × 25 = ₹4.5 crore in today's money. After accounting for 7% inflation over 20 years, the actual corpus target will be higher, which is exactly what this calculator computes for you.

To calculate your FIRE number, the first block is enough. These inputs estimate your retirement expenses and convert them into the corpus you need for financial independence.

The second block is optional for calculating the FIRE number. It works as a situation assessment, showing whether your current portfolio and monthly investments are on track to reach the target, and whether you have a gap or surplus.

The calculator first estimates your annual expenses at retirement using your monthly expenses, current age, retirement age, and inflation assumption. It then applies the FIRE multiple to show your target corpus.

After the FIRE number is known, the second section checks your progress. Enter:

The Projection card then shows annual expenses today, inflation-adjusted expenses at retirement, projected portfolio value, and either the gap to fill or projected surplus. This is the decision layer: it tells you whether to increase investments, review return assumptions, delay retirement, or keep building a margin of safety.

Rohan is 30 years old, spends ₹50,000 a month, and wants to retire at 50. He wants to know: how much does he actually need?

He enters his monthly expenses, target ages, and 7% inflation. The calculator tells him he needs ₹6.96 crore to retire at 50 and live comfortably till 85.

Rohan has ₹10 lakh invested, adds ₹25,000 per month, assumes 12% pre-retirement returns, and uses a more conservative return after retirement. The calculator projects his retirement corpus and compares it with his FIRE target.

If there is a shortfall, he can increase monthly investment, review return assumptions, push retirement age, reduce expenses, or combine these changes. If there is a surplus, the plan has a margin of safety, but it still needs periodic review for inflation, taxes, healthcare, and market risk.

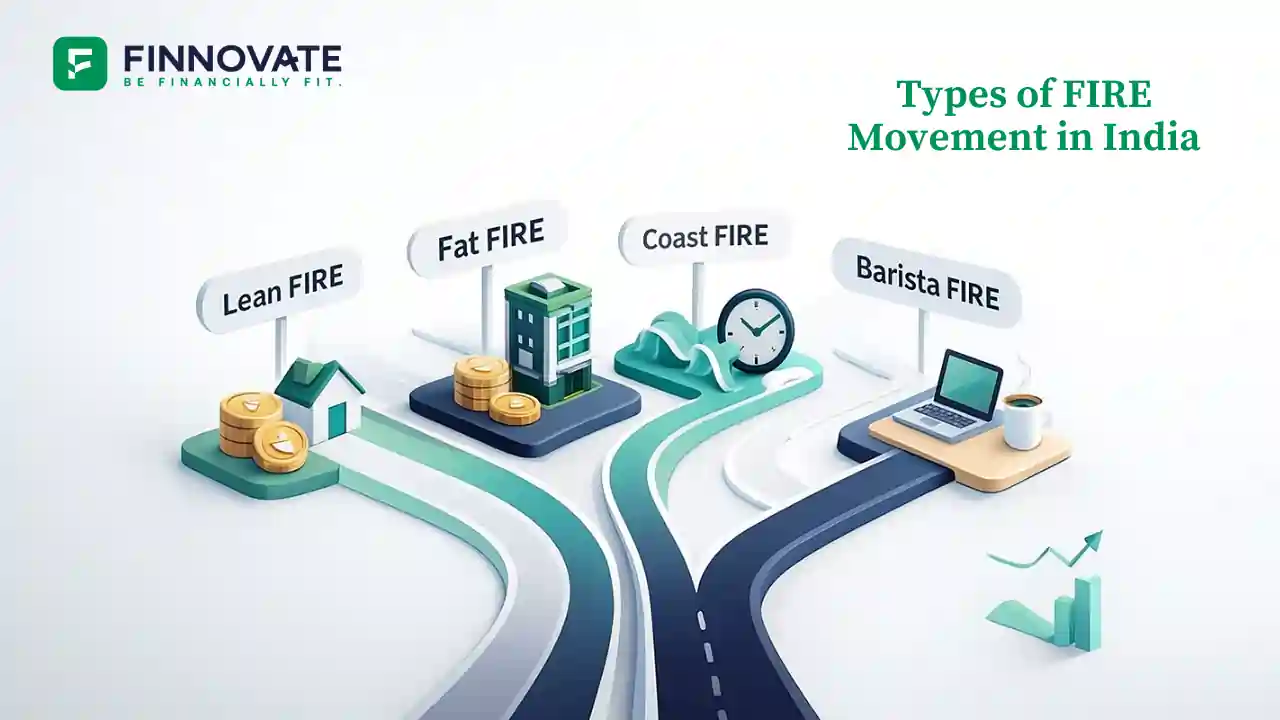

Not everyone wants the same retirement. FIRE comes in different forms depending on how much you plan to spend after you stop working.

Lean FIRE is retirement on an essentials-first budget covering housing, food, healthcare, and basic family needs. Spending stays low, so the corpus required is smaller. This calculator uses 15x your annual expenses as the Lean FIRE target.

Fat FIRE is retirement with your lifestyle fully intact, including travel, better schools, dining out, and discretionary spending without guilt. This requires a larger corpus, shown here as 50x your annual expenses.

Most people sit somewhere in between. A useful exercise: run this calculator twice, once with your current monthly spending and once with a trimmed-down essential budget. Your realistic target usually falls between the two outputs, and knowing both ends of the range helps you make a more grounded decision about when and how to retire.

The 4% rule comes from the Trinity Study (Cooley, Hubbard & Walz, 1998), which was based on US market data. It works reasonably well for the US because inflation there has historically stayed around 2 to 3%. India is a different situation.

For India, most advisors recommend a 3% to 3.5% SWR. At 3.5%, your FIRE number becomes Annual Expenses × 28.6, which is roughly 14% higher than the standard formula. This calculator uses the 4% convention as a baseline, but we recommend building a 10 to 15% buffer on top of your computed number to account for these realities.

Most salaried Indians are quietly building retirement wealth in government-backed instruments they rarely think of as FIRE corpus. PPF, NPS, and EPF can meaningfully reduce the gap between where you are and where you need to be.

Add all of these to the “Current Portfolio” field above. Doing so gives you a realistic gap or surplus rather than an inflated target that ignores wealth you have already built.

Not sure how PPF, NPS, and EPF compare? Read our detailed guide: EPF vs PPF vs NPS: Which is Better for Retirement in India?

Honestly, classic early FIRE, such as retiring in your early 40s, requires a high income, a high savings rate, and many years of disciplined investing. Not everyone can get there, and that is fine.

The FIRE framework is useful even if your goal is more moderate. Retiring at 58 with financial security and no money stress is still FIRE thinking. The calculator helps you find that number regardless of your target age.

Even if full FIRE feels out of reach, partial progress matters. Building a corpus large enough to cover half your expenses from returns means you only need to earn the other half from work. That is a significant shift in how freely you make career and life decisions.

Use the calculator as a planning simulator. Change one variable at a time, such as monthly investment, pre-retirement return, post-retirement return, inflation, or retirement age, and watch how the gap or surplus responds. Most people are closer than they expect.

The FIRE Calculator is not just for high earners with aggressive timelines. Different professionals use it in different ways depending on their situation and goals.

Revisit this calculator once a year. As your income, expenses, portfolio, inflation assumption, and return expectations change, your FIRE number and projected surplus or gap change too. Treating it as an annual review turns a one-time calculation into a proper financial independence health check.

Knowing your FIRE number is only the start. Reaching it is a long game, and a few habits separate people who get there from those who drift.

Read our expert guides on achieving financial independence