How to Retire at 40 in India: Corpus, FIRE Roadmap and Investment Plan

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

20 June 2026

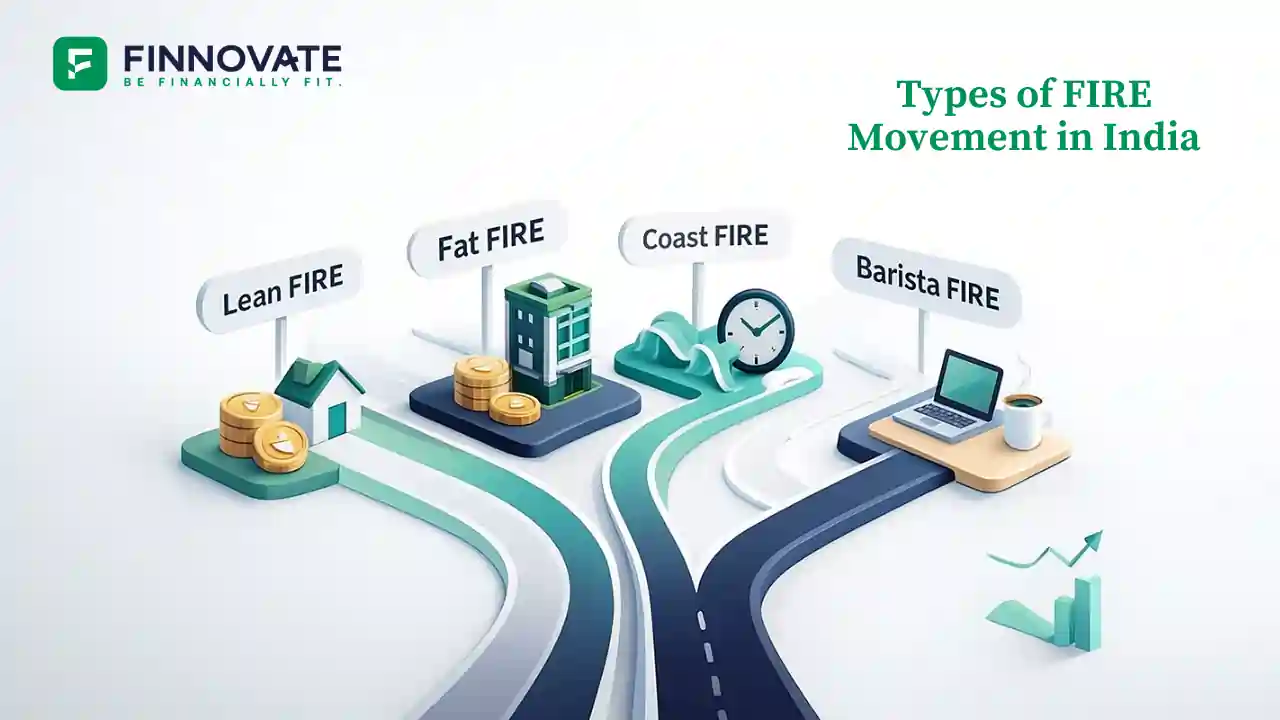

FIRE (Financial Independence, Retire Early) is not one fixed path. For some, it’s about stopping full‑time work early. For others, it’s the freedom to choose lighter work, move cities, take long breaks, or simply say “no” without money stress. This guide breaks down the four practical styles you’ll see in India: LeanFIRE, FatFIRE, CoastFIRE and BaristaFIRE.

FIRE means reaching a point where your investments can support your lifestyle so paid work becomes optional. For a fuller primer, see FIRE in India Explained: Meaning, Math & How to Start.

Your FIRE number is the total corpus you need so you can withdraw safely each year without running out of money. To size it, read How to Calculate Your Financial Freedom Number in India and test your assumptions using the calculators below.

FIRE Calculator • https://www.finnovate.in/fire-calculator

Retirement Calculator • https://www.finnovate.in/retirement-calculator

What it means: Achieving financial independence with a simple, comfortable, low‑frills lifestyle. Not extreme frugality - just choosing “enough.”

Typical lifestyle choices:

Why people choose it: Lower expenses → smaller FIRE number → earlier independence.

Who it suits: People who value time and autonomy over lifestyle upgrades and are flexible about location.

Orientation (not advice): Annual expenses × 25–28.

What it means: Financial independence without cutting back on your current lifestyle. In many cases, the aim is to retain - or improve - comfort.

Typical lifestyle choices:

Implication: Higher expenses → much larger FIRE number. This usually requires more working years, higher savings, or faster income growth.

Who it suits: High earners who want independence and comfort.

Orientation (not advice): Annual expenses × 30–35.

What it means: Save and invest aggressively early so compounding does the rest. Build a seed corpus that grows to your retirement target - then scale back forced saving.

How it works:

You’re not retired - you just stop worrying about retirement savings.

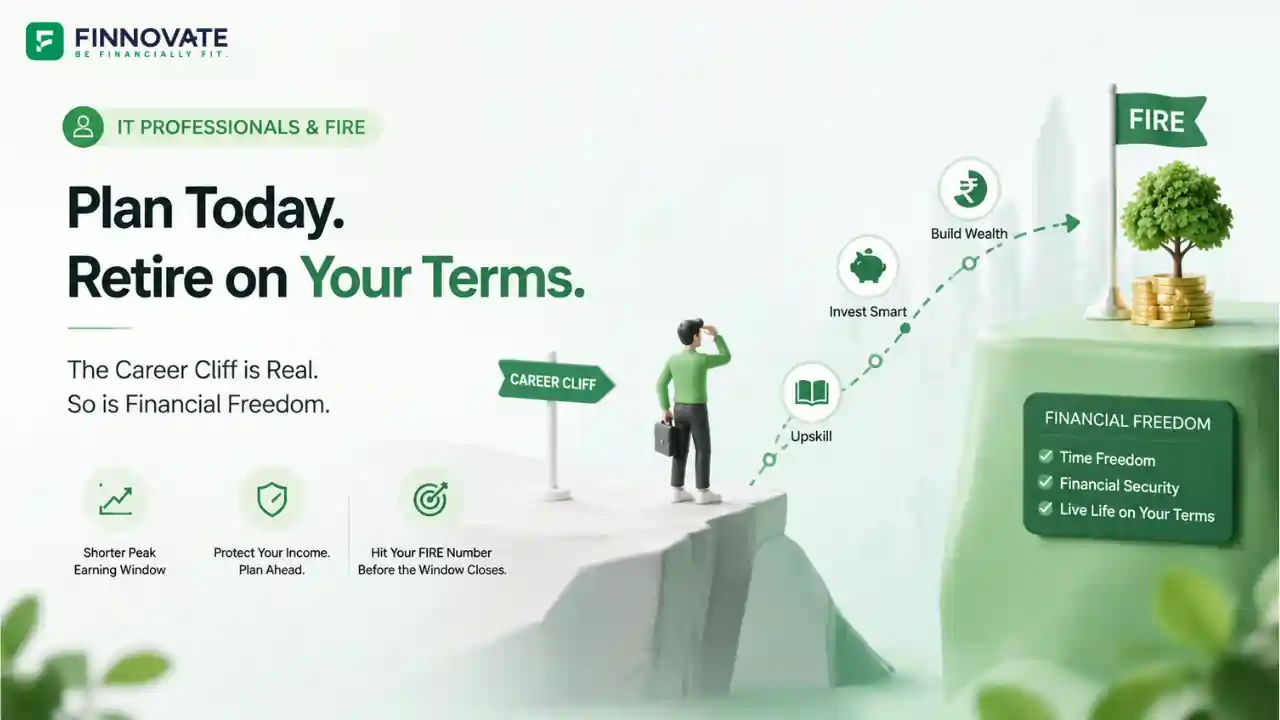

Who it suits: Early‑career high earners (corporate professionals, specialists, founders) who want flexibility in their 40s–50s.

Orientation (not advice): Build a seed corpus by early 30s that compounds to your retirement target by 55–60.

What it means: Semi‑retirement with part‑time, consulting, or flexible work. Investments cover a portion of expenses; the rest comes from controlled work you enjoy.

How it works:

Indian examples:

Who it suits: People who enjoy working but want more control, backed by a dependable corpus.

Orientation (not advice): Annual expenses × 20–28, plus consistent part‑time income.

| FIRE type | Lifestyle focus | Work pattern | Expense level vs today | Corpus needed | Best suited for |

|---|---|---|---|---|---|

| LeanFIRE | Simple, comfortable, low‑frills | Work optional; can fully retire | Lower | Smallest | Flexible on city; prefer freedom over luxury |

| FatFIRE | Comfortable/premium lifestyle | Work optional; lifestyle unchanged | Same or higher | Largest | High earners wanting comfort + independence |

| CoastFIRE | Normal retirement later; low saving stress now | Continue working; retirement savings stop after “coast number” | Similar | Corpus built early, left to grow | Young high earners seeking flexibility later |

| BaristaFIRE | Balanced lifestyle + time freedom | Part‑time, consulting, or lighter work | Moderately lower | Medium–High | People who like working but want more control |

These are orientation ranges, not recommendations. Personalise with calculators.

Disclaimer: Educational content only - not investment, tax, or legal advice. Use ranges as starting points. Personalise with calculators and review yearly.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

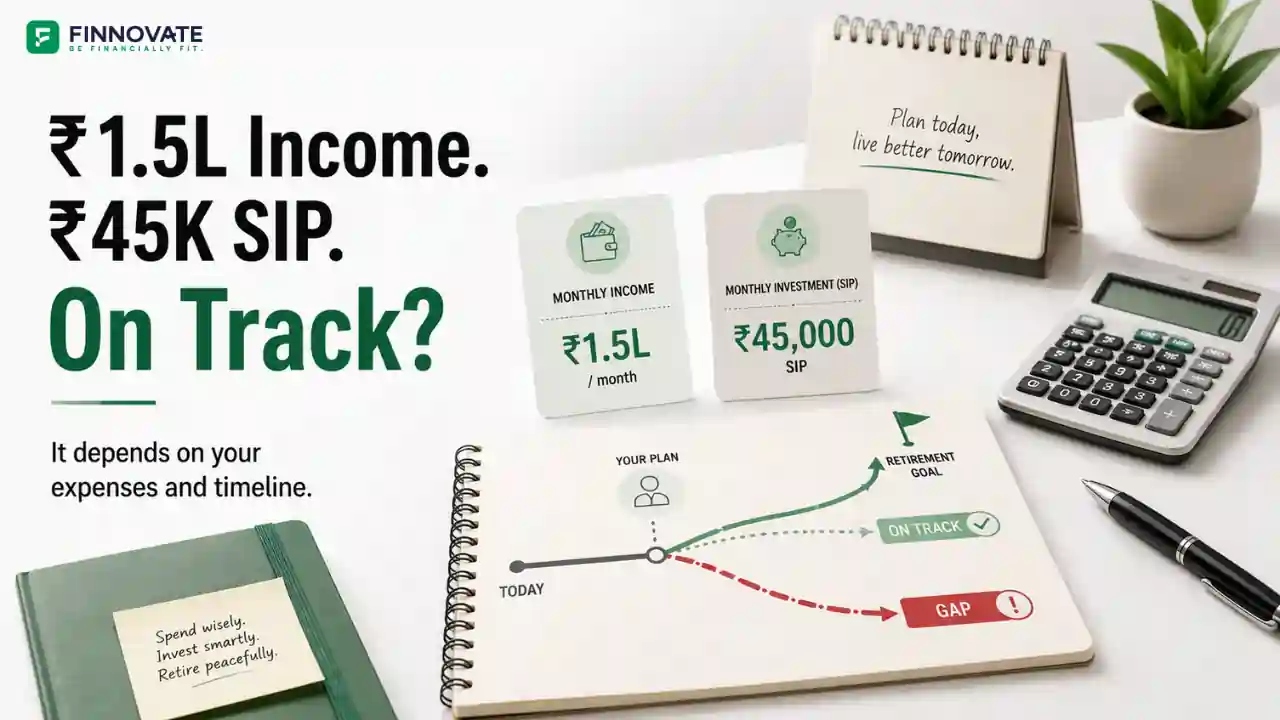

Rs 45,000 on Rs 1.5 lakh salary is a 30% savings rate. But is it enough? See corpus built ...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...