How to Retire at 40 in India: Corpus, FIRE Roadmap and Investment Plan

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

20 June 2026

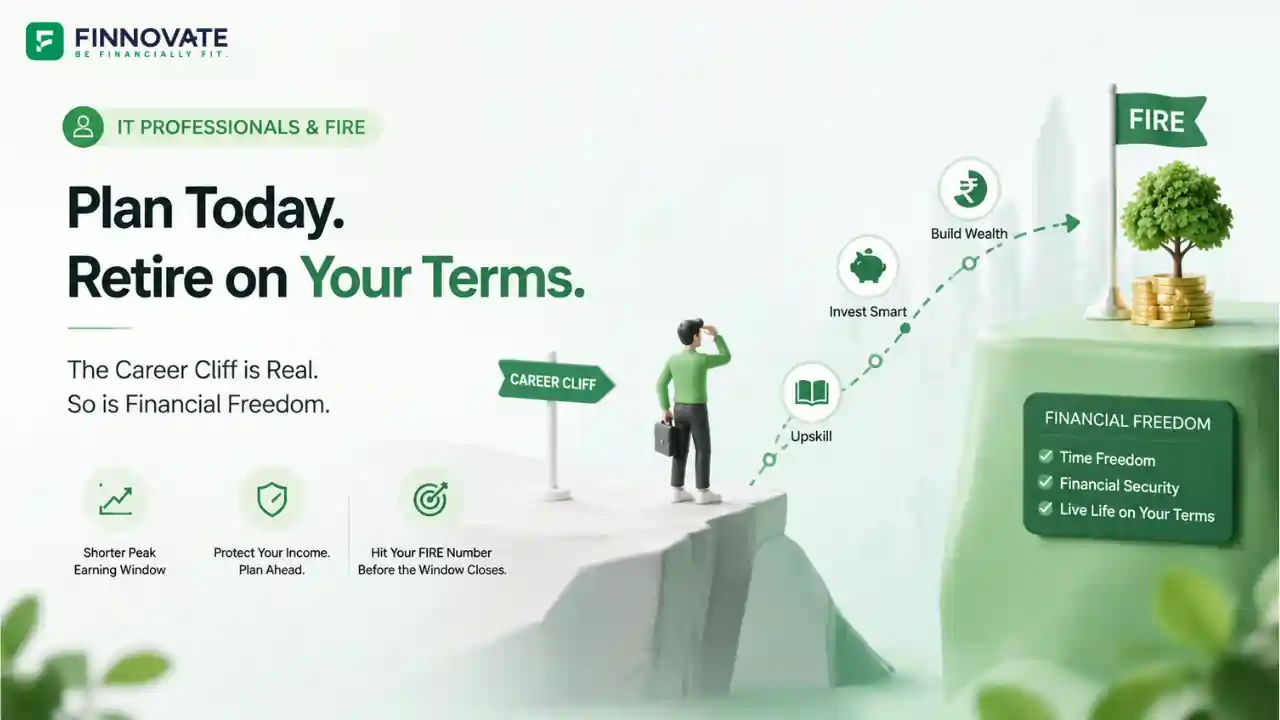

Most FIRE planning articles are written as if retirement is a date you choose. For IT professionals in India, it is also a date that can choose you.

The peak earning window in Indian IT (typically ages 28 to 43) is shorter than most FIRE plans account for. Restructuring, skill obsolescence, and cost-to-company calculations start working against seniority after 42-45. The financial plan that assumes 10 more years of peak income needs a harder look.

This article is built specifically for IT professionals: the career cliff, the FIRE number for your expense profile, the ESOP and RSU considerations, and the accumulation timeline that gets you there before the window closes.

In This Article

Three specific financial consequences of the IT career trajectory after 42-45. Not career advice. Financial implications only.

After 42-45, promotions plateau, variable pay compresses, and restructuring risk increases with seniority. A FIRE plan built on 10 more years of Rs 40-60 lakh income needs a stress test: what does the outcome look like with 6-7 years instead?

Employer group health cover ends with employment. Individual cover bought at 46-48 costs 40-60% more than at 35-38 and may exclude conditions developed in between. This is a pre-retirement action item, not a post-retirement one.

A Rs 2-3 crore home loan taken at 40 with a 20-year tenure creates a Rs 1.5-2 lakh monthly obligation that does not pause if the salary stops at 44-45. Carrying significant EMI obligations into the 42-48 age band without FIRE readiness is the highest single financial risk in this segment.

For a 40-year retirement (FIRE at 45, life to 85), the 3.5% withdrawal rate is more appropriate than the standard 4%. The 4% rule was built for a 30-year US retirement. A 40-year Indian retirement, with higher structural inflation and no social security, needs more conservative planning.

| Monthly Expenses Today | Retire at 45 (15 years) | Retire at 48 (18 years) | Retire at 50 (20 years) |

|---|---|---|---|

| Rs 1 lakh | Rs 7.19 crore | Rs 8.56 crore | Rs 9.62 crore |

| Rs 1.5 lakh | Rs 10.78 crore | Rs 12.84 crore | Rs 14.43 crore |

| Rs 2 lakh | Rs 14.38 crore | Rs 17.13 crore | Rs 19.24 crore |

These are not generic FIRE mistakes. These are the specific gaps that appear repeatedly in the IT FIRE community and that standard planning frameworks do not address.

A significant share of many IT professionals' net worth sits in employer equity: ESOPs, RSUs, ESPP. For some this exceeds 40-50% of the total portfolio. This is concentration risk, income risk, and liquidity risk in a single instrument. If the employer restructures and the stock corrects simultaneously (which is not rare in a downturn), the portfolio takes a double hit at the moment career income also comes under pressure. A FIRE plan with more than 10-15% of the total portfolio in employer equity needs a structured diversification plan before the retirement date.

NPS Tier 1 cannot be accessed before age 60. An IT professional who FIREs at 45 has 15 years of NPS lock-in. NPS should be sized as the post-60 buffer: the corpus that provides income in the later decades of retirement. The liquid investable corpus (mutual funds, direct equity, debt instruments) must cover the full 45-60 period independently. A plan that counts NPS toward the FIRE number without accounting for the lock-in has a structural gap in the early retirement years.

Many IT households are dual-income. The FIRE plan often assumes both salaries continue to the target retirement date. Both face the career cliff. If one partner exits at 43-44, the accumulation rate drops by 40-50%. A FIRE plan that has not been stress-tested on a single income has a structural dependency that needs addressing before, not after, the retirement date.

ESOPs and RSUs are not simply equity holdings. They create specific tax events at specific times that need to be planned for. Three steps in sequence:

| Stage | What Happens | Indian-Listed Shares (TCS, Infosys etc.) | Foreign-Listed Shares (Google, Amazon, Meta etc.) | Planning Action |

|---|---|---|---|---|

| Vesting | FMV on vesting date treated as perquisite income | Taxed at applicable slab rate (20% or 30%) for both. TDS deducted by employer. | Plan cash flow; large vesting in a high-bonus year pushes income into higher brackets | |

| Short-term sale | Shares sold within holding period | STCG at 20% (within 12 months) | STCG at applicable slab rate (within 24 months) | Foreign RSU STCG is materially more expensive at higher income brackets |

| Long-term sale | Shares sold beyond holding period | LTCG at 12.5% above Rs 1.25L (after 12 months) | LTCG at 12.5% (after 24 months) | Phased sell-down over 12-24 months (Indian) or 24+ months (foreign) is more tax-efficient |

| Reinvest proceeds | Sale proceeds need immediate deployment | No further tax at reinvestment. Allocation decision should be pre-decided. | Do not let lump sums sit idle in savings accounts | |

Holding RSUs from a US-listed company? The tax treatment differs significantly from Indian-listed ESOPs, especially on short-term gains. Book a call to map out your specific vesting tax strategy.

Book a Free CallReaching the FIRE corpus on an IT professional's timeline requires three distinct phases, each with a savings rate target, allocation approach, and corpus milestone.

Individual health insurance secured before age 35. Term insurance sized to current income. ESOP/RSU diversification plan in place: no more than 15% of portfolio in employer equity. Step-up SIP set to match annual salary increments.

FIRE number calculated at 3.5% withdrawal rate and verified against current corpus. NPS contributions sized as post-60 buffer, not primary FIRE corpus. Home loan on track to clear by 45. Dual-income stress test run: does the plan survive on one income for the final 4-5 years?

Short-term bucket funded (2 to 3 years of expenses in liquid instruments). Healthcare buffer of Rs 35-50 lakh funded separately. Withdrawal plan stress-tested against a 25% equity drawdown in year one. Employer equity concentration below 10%.

For a detailed view of how asset allocation shifts approaching early retirement, the Finnovate guide covers the transition from accumulation to drawdown across each decade.

An IT professional's FIRE plan has more moving parts than a standard retirement plan. The FinnFit test shows how your Investment, Insurance, and Goal Planning pillars score together in under 5 minutes. Or book a call to map your specific FIRE timeline.

Six questions specific to the IT professional's FIRE situation. Each references a number or threshold from this article.

An IT professional's FIRE plan has specific structural requirements that a standard retirement plan does not address: career cliff timing, employer equity concentration, NPS lock-in, and the dual-income dependency. A SEBI-registered adviser can map your specific corpus, ESOP concentration, NPS allocation, and career timeline into a plan that accounts for all of them.

The IT professional's FIRE plan is not more complicated than anyone else's. It is more urgent. The career cliff is not a scare tactic. It is a structural reality in Indian IT that reshapes the effective savings window. Building the FIRE structure before it becomes a necessity is the difference between choosing to leave and being left. The numbers in this article are large. The timeline to reach them is shorter than it looks. Starting earlier and saving more aggressively than feels comfortable is the one lever that makes all the others work.

The corpus required depends on monthly expenses, planned retirement age, and the withdrawal rate used. At a 4% withdrawal rate and 6% inflation, an IT professional with Rs 1.5 lakh monthly expenses targeting retirement at 45 needs approximately Rs 10.78 crore. At the more conservative 3.5% rate appropriate for a 40-year retirement, that rises to Rs 12.33 crore. For a full breakdown of how monthly expense targets translate to corpus requirements, see the retirement corpus guide. Please consult a SEBI-registered investment adviser to compute the figure for your specific situation.

The career cliff refers to the structural change in employment dynamics for IT professionals after 42-45: promotions plateau, variable pay compresses, and restructuring risk increases with seniority. The financial planning implication is that the peak earning window may be shorter than the FIRE timeline assumes. A plan built on 10 more years of peak income needs a stress test: what does the FIRE outcome look like with 6-7 years of peak income instead?

ESOPs and RSUs create three distinct decisions. At vesting, the market value is taxed as perquisite income at the applicable slab rate. After vesting, holding beyond 12 months before selling attracts LTCG at 12.5% above Rs 1.25 lakh annually, versus STCG at 20% for earlier sales. Reinvestment of proceeds into a diversified corpus is the third step. The structural principle is to keep employer equity concentration below 15% of total portfolio. Please consult a qualified tax professional for the treatment applicable to your specific ESOP and RSU scheme.

NPS Tier 1 cannot be accessed before age 60. An IT professional who retires at 45 has 15 years of NPS lock-in. The practical approach is to size NPS as the post-60 buffer while building a separate liquid corpus in mutual funds and direct equity to cover the 45-60 period independently. If NPS forms more than 20% of the total planned FIRE corpus, the plan likely has a gap in the early retirement years.

The required savings rate depends on current income, existing corpus, and the target FIRE number. For a Rs 40 lakh CTC professional targeting Rs 7 crore corpus in 15 years from zero, the required monthly SIP is approximately Rs 1.40 lakh, which is about 54% of take-home. For a Rs 60 lakh CTC professional, the same target requires approximately 40% of take-home. FIRE at 45 is financially achievable for Rs 40 lakh-plus CTC professionals who start at 28-32 and maintain high savings rates throughout.

A software engineer earning Rs 40 lakh CTC in a metro city with Rs 1.5 lakh monthly expenses targeting retirement at 45 needs approximately Rs 10.78 crore at a 4% withdrawal rate, or Rs 12.33 crore at 3.5%. Use the Finnovate FIRE Calculator to run your specific numbers. For a structured early retirement readiness framework, the early retirement readiness guide covers all six dimensions of readiness beyond corpus size.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice, tax advice, or a recommendation to buy or sell any securities or financial instruments. Corpus figures are illustrative estimates based on assumed inflation, return, and withdrawal rate parameters. They are not guaranteed outcomes or personalised financial targets. ESOP and RSU tax treatment described is general in nature and does not constitute personalised tax advice. Tax rules on ESOPs and RSUs may vary based on employer scheme design, residency status, and applicable double tax treaty provisions. Please consult a qualified tax professional for advice specific to your situation. Past investment performance is not indicative of future returns. Please consult a SEBI-registered investment adviser before making any financial planning or investment decisions. Investments in mutual funds and other market-linked instruments are subject to market risks.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

Rs 45,000 on Rs 1.5 lakh salary is a 30% savings rate. But is it enough? See corpus built ...

Use this practical framework to check if you’re ready for early retirement in India. Cov...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...