How to Retire at 40 in India: Corpus, FIRE Roadmap and Investment Plan

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

20 June 2026

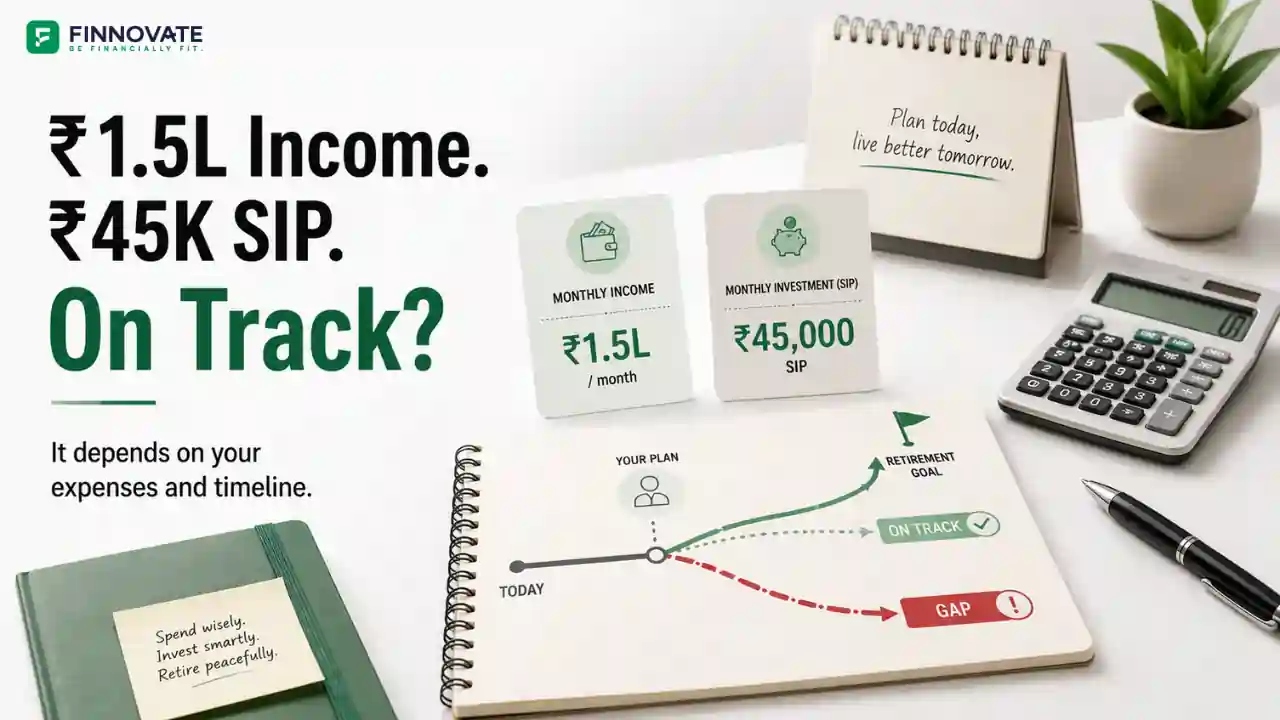

Rs 45,000 on Rs 1.5 lakh take-home is a 30% savings rate. That is above average for a salaried professional in India. Whether it is enough is a different question, and the answer depends on two numbers most people have never calculated: their actual monthly expenses and their retirement timeline.

This article runs both calculations for three expense levels and three timelines. The result is a specific, honest answer rather than a generic "invest more."

Some readers will find they are already on track. Others will find a gap and a single decision that closes most of it.

In This Article

Before running the full calculation, three quick benchmarks to orient the answer.

Rs 45,000 is a genuinely good savings rate. The rest of this article gives it a destination.

Most readers only count their SIP when thinking about retirement. EPF builds quietly in the background and is frequently underestimated. The two components together tell a materially different story than the SIP alone.

| Timeline | SIP Corpus at 12% CAGR |

|---|---|

| 15 years | Rs 2.25 crore |

| 20 years | Rs 4.45 crore |

| 25 years | Rs 8.45 crore |

| Timeline | EPF Corpus at 8.25% |

|---|---|

| 15 years | Rs 39 lakh |

| 20 years | Rs 67 lakh |

| 25 years | Rs 1.09 crore |

| Timeline | SIP | EPF | Combined |

|---|---|---|---|

| 15 years | Rs 2.25 crore | Rs 39 lakh | Rs 2.64 crore |

| 20 years | Rs 4.45 crore | Rs 67 lakh | Rs 5.12 crore |

| 25 years | Rs 8.45 crore | Rs 1.09 crore | Rs 9.54 crore |

The combined corpus figure only becomes meaningful when compared against what is actually needed. The table below shows corpus required versus corpus built across three expense levels and three timelines.

| Monthly Expenses Today | 15 Years | 20 Years | 25 Years |

|---|---|---|---|

| Rs 50,000 | Need Rs 3.59Cr Built Rs 2.64Cr Gap Rs 96L |

Need Rs 4.81Cr Built Rs 5.12Cr Surplus Rs 31L |

Need Rs 6.44Cr Built Rs 9.54Cr Surplus Rs 3.1Cr |

| Rs 75,000 | Need Rs 5.39Cr Built Rs 2.64Cr Gap Rs 2.75Cr |

Need Rs 7.22Cr Built Rs 5.12Cr Gap Rs 2.10Cr |

Need Rs 9.66Cr Built Rs 9.54Cr Gap Rs 12L |

| Rs 1 lakh | Need Rs 7.19Cr Built Rs 2.64Cr Gap Rs 4.55Cr |

Need Rs 9.62Cr Built Rs 5.12Cr Gap Rs 4.50Cr |

Need Rs 12.88Cr Built Rs 9.54Cr Gap Rs 3.34Cr |

For Rs 50,000 expenses with 20+ years, Rs 45,000 flat SIP plus EPF is already sufficient. No action needed beyond maintaining the current rate.

For Rs 75,000 expenses with 15-20 years, a gap of Rs 2.10 to 2.75 crore exists. The next section shows how one annual decision closes most of this.

For Rs 1 lakh expenses, a meaningful gap exists across all timelines. Step-up SIP significantly narrows the gap for longer horizons but a higher baseline SIP may also be needed.

A step-up SIP increases the monthly investment by 10% every year. Rs 45,000 this year becomes Rs 49,500 next year, then Rs 54,450 the year after. It is set once on the fund platform, automated, and aligned with salary increments most professionals receive annually.

| Timeline | Flat Rs 45,000 | 10% Annual Step-Up | Additional Corpus |

|---|---|---|---|

| 15 years | Rs 2.25 crore | Rs 3.91 crore | +Rs 1.66 crore |

| 20 years | Rs 4.45 crore | Rs 8.95 crore | +Rs 4.50 crore |

| 25 years | Rs 8.45 crore | Rs 19.24 crore | +Rs 10.79 crore |

Step-up SIP combined with EPF:

| Timeline | Step-Up SIP + EPF | Corpus Needed (Rs 75k exp) | Position |

|---|---|---|---|

| 15 years | Rs 4.30 crore | Rs 5.39 crore | Gap Rs 1.09Cr |

| 20 years | Rs 9.62 crore | Rs 7.22 crore | Surplus Rs 2.4Cr |

| 25 years | Rs 20.33 crore | Rs 9.66 crore | Surplus Rs 10.67Cr |

The only scenario where step-up does not fully close the gap is Rs 1 lakh monthly expenses with 15 years to retirement. That combination of high expenses and short timeline requires a higher baseline SIP rather than just a step-up.

Your SIP and corpus are one part of the picture. The FinnFit test scores your Investment, Goal Planning, Insurance, and Budgeting pillars together in under 5 minutes. Or book a call to map your specific retirement gap.

A Rs 45,000 SIP addresses wealth accumulation. It does not address four other gaps that determine whether the full financial plan holds up under real conditions.

A Rs 1.5 lakh earner needs approximately Rs 9 lakh in liquid instruments, six months of take-home, completely separate from the investment portfolio. Pulling from a SIP during an emergency triggers redemption, potential exit loads, and capital gains tax. The emergency fund is a structural buffer that keeps investments intact, not an investment itself.

A professional earning Rs 18 lakh annually needs individual term insurance of Rs 1.8 crore to Rs 2.16 crore (10 to 12 times annual income). Employer group term cover disappears the moment employment changes. Individual term insurance must be active, in force before any serious health condition arises, and sized to current income rather than the original policy year's income.

Employer group health cover exists only during employment. A hospitalisation that occurs within 3 months at a new employer can go entirely uncovered without individual health insurance. Medical inflation runs at 10% to 15% annually. A professional in their 30s buying individual health insurance is securing it before underwriting is complicated by health history.

Rs 45,000 going into three funds is savings with extra steps. Goal-based investing maps each rupee to a specific outcome: retirement corpus, child's education, home purchase down payment. Each goal has its own target amount, timeline, and appropriate instrument. The same Rs 45,000 structured into goal buckets produces measurable progress rather than a growing number with no clear destination.

Five questions. Each has a specific threshold. A reader who answers all five with a number rather than a feeling has the foundation in place.

This article ran the numbers for a Rs 1.5 lakh / Rs 45,000 SIP scenario. Your actual gap depends on your specific monthly expenses, existing corpus, EPF balance, and retirement timeline. A SEBI-registered adviser can run the full calculation for your situation.

Rs 45,000 on Rs 1.5 lakh is a strong starting point. The question this article answers is whether it is enough for your specific situation. As the sufficiency table shows, the answer varies significantly by expense level and timeline. For lower-expense readers with 20 or more years ahead, the corpus is already on track. For higher-expense readers or those closer to retirement, the gap is real but not large. In most cases, one annual decision closes or materially narrows it: setting up a 10% step-up on the existing SIP. The four gaps section is the more important checklist. A well-sized SIP with no emergency fund, no individual term cover, and no goal mapping is a number without a plan.

It depends on monthly expenses and retirement timeline. For Rs 50,000 monthly expenses with 20 years to retirement, Rs 45,000 flat SIP plus EPF already exceeds the required corpus. For Rs 75,000 expenses with 15-20 years to go, a gap of Rs 2.10 to 2.75 crore exists, largely closeable with a 10% annual step-up. For Rs 1 lakh expenses, a meaningful gap exists across most timelines. For a detailed breakdown of how monthly income targets translate to corpus requirements, see the retirement corpus guide.

At a 12% CAGR assumption using monthly compounding (ordinary annuity), Rs 45,000 per month builds approximately Rs 4.45 crore over 20 years. Combined with EPF contributions of approximately Rs 11,000 per month, the total reaches approximately Rs 5.12 crore. With a 10% annual step-up, the SIP alone builds Rs 8.95 crore over 20 years. For context on how this fits into a broader portfolio strategy, the age-based asset allocation guide covers how equity-debt mix should shift over time. Past performance is not indicative of future returns.

Yes. EPF is one of the most underestimated components of retirement planning for Indian salaried professionals. The combined employee and employer contribution compounds at the EPFO-declared rate annually. Over 20 years at Rs 11,000 per month, EPF builds approximately Rs 67 lakh. This directly reduces the gap between the SIP corpus and the required retirement figure. Current EPF balance is available via the EPFO member portal using your UAN.

A step-up SIP automatically increases the monthly SIP amount by a fixed percentage each year, typically 10%. On Rs 45,000, a 10% annual step-up increases the 20-year corpus from Rs 4.45 crore to Rs 8.95 crore, an additional Rs 4.50 crore from the same starting salary. It is set once on the fund platform and aligns savings growth with typical annual salary increments.

Rs 45,000 SIP represents a 30% savings rate of take-home, rising to approximately 34% when EPF employee contributions are included. The total monthly investment including both EPF components reaches approximately Rs 56,000, or about 37% of take-home. For a professional earning Rs 1.5 lakh, a 30-35% savings rate is broadly considered strong for retirement planning. Whether it is sufficient depends on the retirement timeline and expense level.

The starting point is identifying your actual monthly expense from 6 months of bank statements, then determining the corpus required at a 3.5% to 4% withdrawal rate for your target retirement age. The sufficiency table in this article provides a starting benchmark. Use the Finnovate FIRE Calculator to run your specific numbers. If there is a gap, a 10% annual step-up is typically the first lever to adjust. For a framework on structuring goals around this corpus target, the financial goals guide covers the goal-mapping process. Please consult a SEBI-registered investment adviser to compute the specific figure for your situation.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any securities or financial instruments. SIP corpus projections are illustrative estimates based on an assumed 12% CAGR. EPF corpus projections assume continued employment at current contribution levels and the EPFO-declared interest rate. Corpus sufficiency figures assume 6% annual inflation and a 4% withdrawal rate. All figures are indicative estimates and not guaranteed outcomes or personalised financial targets. Actual results will vary based on individual circumstances, fund performance, market conditions, and changes in tax or regulatory frameworks. Past investment performance is not indicative of future returns. Please consult a SEBI-registered investment adviser or qualified financial professional before making any financial planning or investment decision. Investments in mutual funds and other market-linked instruments are subject to market risks. Read all scheme-related documents carefully before investing.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

Use this practical framework to check if you’re ready for early retirement in India. Cov...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...