How to Retire at 40 in India: Corpus, FIRE Roadmap and Investment Plan

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

20 June 2026

If you’ve been hearing about FIRE and wondering what it means in an Indian context, here’s the simple version: FIRE stands for Financial Independence, Retire Early. It’s not about quitting work tomorrow; it’s about building a corpus that lets your investments cover your lifestyle, so paid work becomes optional. Think of it as buying back your time - on your terms.

Interest in FIRE is rising in India for a few clear reasons: costs keep climbing, career paths are less linear, and many people want flexibility to start something of their own, take mini-sabbaticals, or simply reduce stress. This guide gives you a no-jargon explainer, the simple math behind a starting FIRE number, and 5 beginner steps to kick off - plus a calculator you can try today.

Try it now: Open the FIRE Calculator (set your monthly spend, inflation, and timeline) → FIRE Calculator

Use these to frame expectations - and to stay motivated:

Sources: Pension System Analysis 2025, India Retirement Index Study (IRIS) 4.0

Takeaway: FIRE is achievable if you start with clear expenses, realistic inflation, and a repeatable savings habit - not by chasing perfect returns.

FIRE means your investments generate enough sustainable income to cover your living expenses without relying on a paycheck. Once you reach that point, work becomes a choice. Some people continue to work (on lighter terms), others take breaks, some switch careers, and some fully retire. The idea isn’t a one-size template - it’s a spectrum.

Read: Types of FIRE in India: Lean, Fat, Coast & Barista Explained

The goal here is to build a starting point, not a perfect forecast. You’ll refine it annually.

Track expenses for 2–3 months. Convert that to annual. Use the Indian number format and focus first on essentials (housing, groceries, utilities, transport, basic healthcare, school fees if applicable). You can add discretionary items (travel, hobbies, upgrades) after you lock in the base.

Example: ₹1,00,000/month → ₹12,00,000/year.

₹ today ≠ ₹ later.

As a beginner, you can use a 6-7% rough inflation assumption for a quick estimate. Healthcare and education often run higher, but start simple; the aim is to begin and iterate.

If you plan to target FIRE in, say, 12 years, your ₹12,00,000/year today might need to be higher then. You can keep this step simple for now and refine later when you play with the calculator.

People often start with a withdrawal-rate idea. Without debating the exact number, a starter thumb-rule is:

Annual expenses × 25–33 = Starting corpus range

This range translates to a 3–4% notional withdrawal idea in the background - but treat it as a starting range, not a promise. You’ll personalize it with your lifestyle, risk comfort, and later with portfolio and withdrawal specifics (that’s for an advanced article).

In the first 5–10 years, the thing that moves your plan most is how much you save, not whether your expected return is 10% or 11%. A 1% return tweak on a small corpus is tiny; a 5–10% increase in savings rate compounds faster because you are adding more capital every month.

Pair this with the India reality: a large share of people still save only 1–15% of salary for retirement. If you’re currently in that band, nudging it up is the single easiest win you can engineer this year.

Action: Raise your savings rate by 1–2% every quarter until it starts to pinch. You’ll barely feel each step, but the compounding effect on your corpus is meaningful.

Compounding has two plain rules: start and stay consistent. You don’t need perfect timing; you need a repeatable system.

A tiny illustration (purely educational):

See your starting number now with our tool.

calculate your FIRE number with your goals in mind and build a straightforward plan you can follow - let’s begin with a call.

Set up my plan callTreat it as a starting thumb-rule, not a guarantee. Begin with expenses × 25–33 to form a range. As you progress, you’ll personalize assumptions and your portfolio. (We’ll cover deeper withdrawal approaches in a separate, advanced article.)

₹12,00,000/year × 25–33 → ₹3.0–₹4.0 crore as a starting range. This will change with your inflation, timeline, future choices, and corpus growth. Use the calculator for a quick sense check.

You build a “seed” corpus early that can grow on its own to traditional retirement even if you contribute less later so you can choose lighter work in the meantime. (We’ll link a dedicated India explainer separately.)

Tackle expensive debt first (e.g., high-rate personal or credit card debt). For lower-rate, well-secured loans, run the numbers, don’t let a poor loan dominate your monthly cash-flow.

Once or Twice a year is enough for beginners. Add a calendar reminder; avoid constant tinkering.

Disclaimer: This article is for education only and is not investment, tax, or legal guidance. The examples and calculator outputs are illustrative and for education only; they are not recommendations. Please do your own research before acting.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

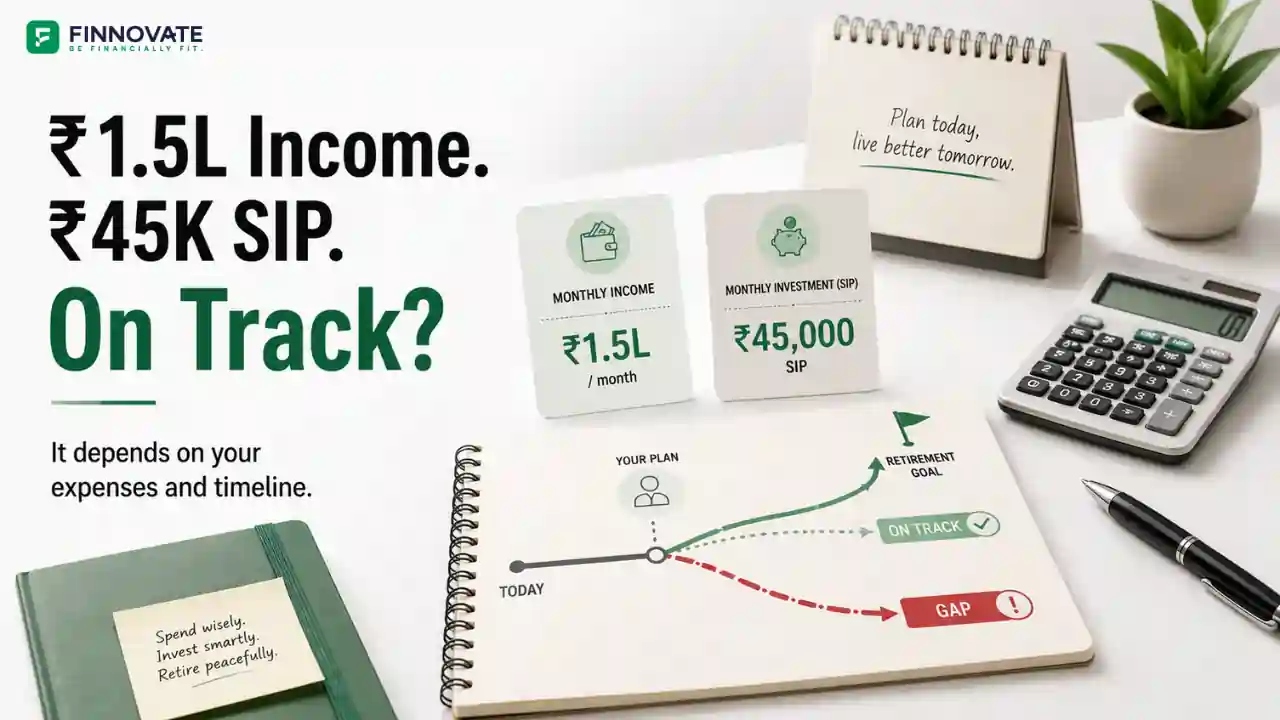

Rs 45,000 on Rs 1.5 lakh salary is a 30% savings rate. But is it enough? See corpus built ...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...