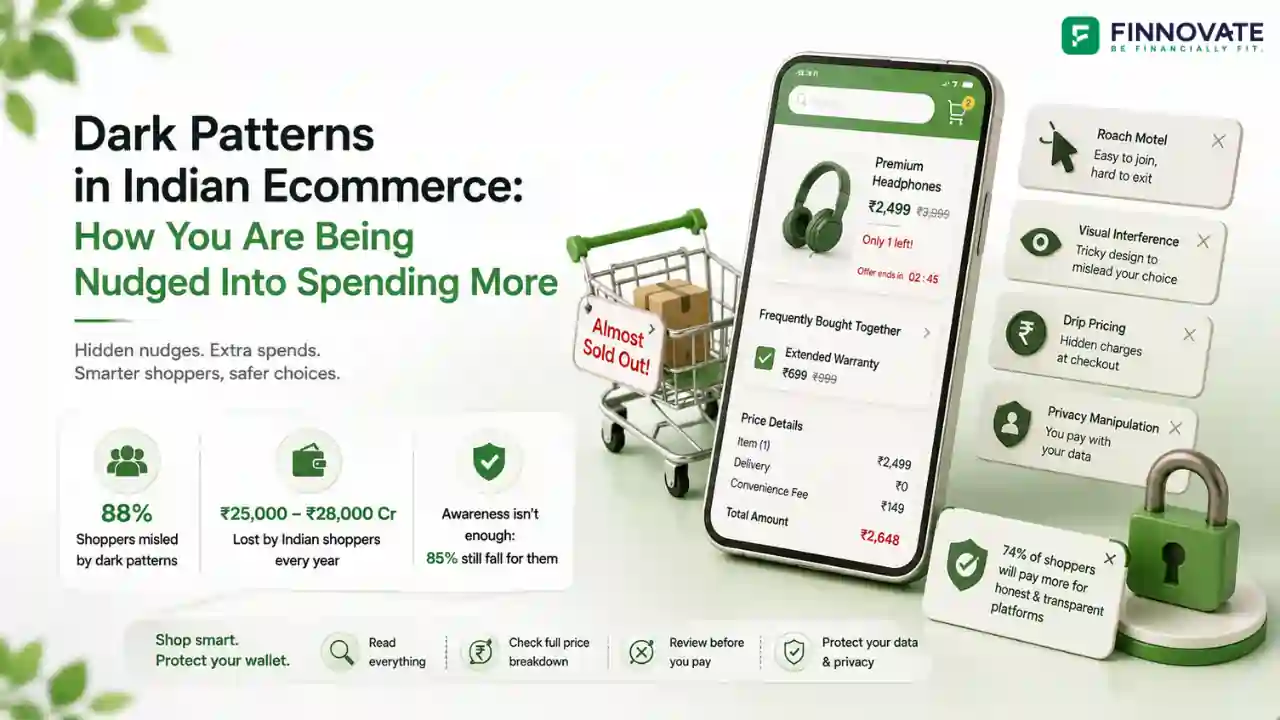

Dark Patterns in Indian Ecommerce: What They Are and How to Protect Yourself

Indian online shoppers lose ₹25,000-28,000 crore a year to dark patterns. 88% are affect...

18 June 2026

Data period: June 1 to June 13, 2026 | Source: NSDL fortnightly sectoral FPI investment data

After three consecutive months of tapering FPI equity outflows from India, the first fortnight of June 2026 delivered a sharp reversal. FPIs sold $6.70 billion (₹62,853 crore) from Indian equities in the first two weeks of June, more than double the entire May 2026 outflow of $3.44 billion and the highest fortnightly selling since March 2026. The selling was also more broad-based: 19 of 23 NSDL-tracked sectors saw net outflows, compared to 18 of 23 in May.

The trigger was a combination of unresolved geopolitical uncertainty from the Middle East peace deal's outstanding technical clauses, concerns about how long supply chain normalisation will take even after the Strait of Hormuz reopens, and a structural equity-to-debt rotation being driven by the RBI's June 2026 capital inflow measures that made Indian debt more attractive for FPIs.

Quick read

The tapering from March to May had been seen as a tentative stabilisation signal. The H1 June data erases that interpretation, at least for now. Cumulative FPI equity selling since the September 2024 peak now stands at approximately ₹2.87 lakh crore (approximately $30 billion) for 2026 alone, surpassing the entire calendar year 2025 outflow of ₹1.66 lakh crore.

| Sector (NSDL Classification) | Net Flow (USD million) | Direction |

|---|---|---|

| Financial Services (BFSI) | -1,190 | Selling: largest outflow sector |

| Oil, Gas & Fuels | -1,108 | Selling: war-linked supply chain impact |

| Automobile and Components | -955 | Selling: fuel and input cost pressure |

| Information Technology | -711 | Selling: global IT spending slowdown |

| Fast Moving Consumer Goods | -535 | Selling: inflation impact on consumption |

| Metals & Mining | -499 | Selling: reversal from recent buying trend |

| Healthcare | -475 | Selling: export sector caution |

| Capital Goods | -273 | Selling: investment cycle slowdown fears |

| Power | -272 | Selling: previous favourite now sold |

| Construction Materials | -256 | Selling |

| Consumer Services | -196 | Selling: consumption spending caution |

| Realty | -115 | Selling |

| Chemicals | -82 | Selling |

| Consumer Durables | -67 | Selling |

| Construction | -64 | Selling |

| Media & Entertainment | -24 | Selling |

| Textiles | -15 | Selling |

| Forest Materials | -1 | Selling |

| Diversified | -1 | Selling |

| Utilities | +1 | Buying: marginal |

| Services | +32 | Buying |

| Telecommunication | +39 | Buying |

| Others | +66 | Buying |

| Grand Total | -6,701 | Net selling across 19 of 23 sectors |

BFSI continues to absorb the largest share of FPI equity selling in every period of broad-based outflows. It is the most liquid sector in Indian equities, making it the natural first point of exit when FPIs need to reduce India exposure quickly. Passive index ETF rebalancing tied to India's declining MSCI EM weight is a mechanical driver layered on top of active selling. In H1 June, BFSI's $1.19 billion represented 17.8% of total outflows despite being just one of 23 sectors.

The Middle East peace deal announced in early June 2026 has not resolved the downstream supply chain issues. Insurance costs for Strait of Hormuz shipping remain elevated. Supply of oil and gas from the region is expected to take several months to return to pre-conflict volumes. Indian downstream oil companies face continued elevated input costs, while automotive manufacturers face input cost pressure from fuel and component pricing. These are not sentiment calls; they are earnings-linked selling decisions.

IT selling of $711 million reflects two concerns: global central bank hawkishness slowing enterprise IT spending, and the structural concern about AI disruption reducing the addressable market for traditional Indian IT services. Healthcare selling of $475 million reflects similar export revenue caution as global healthcare budgets face pressure. Both are externally-oriented sectors where global growth expectations directly affect earnings visibility.

Capital goods, metals, and power had been areas of selective FPI buying in April and May 2026. In H1 June, all three saw net outflows. The driver is a shift in the narrative around investment cycles: if global central bank hawkishness slows growth, then capital goods order books face pressure, metal demand softens, and power capacity expansion plans get delayed. The equity-to-debt rotation is also a factor: FPIs rotating from equities into Indian debt instruments through the FAR route are selling across the board, not just from high-conviction positions.

A development that distinguishes H1 June 2026 from earlier selling episodes is the simultaneous rise in FPI debt inflows. While FPIs sold $6.70 billion from equities, they invested over ₹13,200 crore (approximately $1.38 billion) into Indian debt securities via the Fully Accessible Route (FAR) in the same fortnight. Total FAR debt investments year-to-date reached nearly ₹28,000 crore.

| Trigger | Current Status | Market Concern |

|---|---|---|

| Middle East peace deal | Deal announced but sanctions, nuclear enrichment limits, and defreezing of Iranian funds remain unresolved | Uncertainty persists; markets are not pricing a clean resolution |

| Strait of Hormuz reopening | Reopening expected but shipping insurance costs elevated; shippers cautious about risk | Oil supply normalisation will take months; fuel cost pressure continues |

| Global central bank hawkishness | Major central banks maintain elevated rate stances; no near-term pivot signal | Growth outlook under pressure; enterprise IT spending and capital investment cycles slow |

| FPI equity-to-debt rotation | RBI's June 2026 measures made Indian debt more attractive; FAR route inflows rising | Some equity selling may be internally recycled into debt, compounding outflow appearance |

Sustained FPI selling affects sector valuations, market breadth, and rupee stability. The FinnFit Financial Fitness Test takes 3 minutes and shows you how your portfolio's sector exposure stands relative to where FPI flows are concentrated.

Take the FinnFit TestThree factors drove the acceleration. The Middle East peace deal announced in early June left key technical issues (sanctions, nuclear enrichment limits, and defreezing of Iranian funds) unresolved, sustaining uncertainty. Shipping insurance costs for the Strait of Hormuz remained elevated, keeping oil supply normalisation timelines uncertain. And global central bank hawkishness intensified growth concerns, prompting FPIs to reduce exposure to India's export-oriented and cyclical sectors.

BFSI led with $1.19 billion in net outflows, followed by Oil and Gas ($1.11 billion) and Automobiles ($955 million). IT ($711 million), FMCG ($535 million), Metals ($499 million), and Healthcare ($475 million) were the next largest outflow sectors. Capital Goods, Power, and Construction Materials, which had attracted FPI buying in April and May, all reversed to net selling in H1 June.

While selling $6.70 billion from equities, FPIs simultaneously invested over ₹13,200 crore into Indian debt via the Fully Accessible Route (FAR) in the same fortnight. The RBI's June 5, 2026 measures (including removal of G-Sec restrictions and capital gains tax exemptions) made Indian debt more attractive. This means some equity selling may be recycled into debt within India rather than repatriated, potentially reducing the net rupee outflow pressure compared to what the equity headline number suggests.

AUC (Assets Under Custody) measures the total market value of Indian equities held by FPIs. When FPIs sell stocks, AUC falls. But AUC can also rise even during selling periods if the prices of remaining FPI holdings increase due to market appreciation. In June 2026, equity AUC recovered to $719 billion despite net selling, because Indian markets partially recovered in price. AUC recovery does not signal fresh FPI buying; it reflects valuation changes on existing positions.

The two key factors cited in the brief and confirmed by analyst commentary are: resolution of the Middle East situation, specifically when oil supply normalises and Strait of Hormuz shipping returns to full capacity, bringing Brent crude back durably below $80 per barrel; and clarity on the global central bank rate path, specifically whether the US Fed signals a pivot that reduces the return advantage of holding US dollar assets over emerging market equities. Rupee stabilisation would be both a cause and effect of an FPI flow reversal. Please consult a SEBI-registered investment adviser before making any investment decision based on FPI flow data.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any securities or financial instruments. All FPI sectoral flow data referenced in this article is sourced from NSDL's fortnightly sectoral FPI investment data for H1 June 2026 (June 1 to June 13, 2026). FPI equity AUC and debt AUC figures are from NSDL data as cited in the source document and are provisional estimates subject to revision. Monthly trend data for March, April, and May 2026 is from NSDL and confirmed secondary sources. Past FPI flow patterns are not indicative of future flows or market performance. Please consult a SEBI-registered investment adviser before making any investment decision.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Indian online shoppers lose ₹25,000-28,000 crore a year to dark patterns. 88% are affect...

SEBI Chairman announced longer-term F&O contracts on June 12, 2026. But quarterly Nifty op...

India's headline CPI rose to 3.93% in May 2026, food inflation hit 4.78%, and transport in...

India's real GDP grew 7.7% in FY26. But nominal GDP in dollar terms grew roughly 2% over t...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...