Open Architecture in Insurance: What India's 2025 Reform Actually Changed

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

28 April 2026

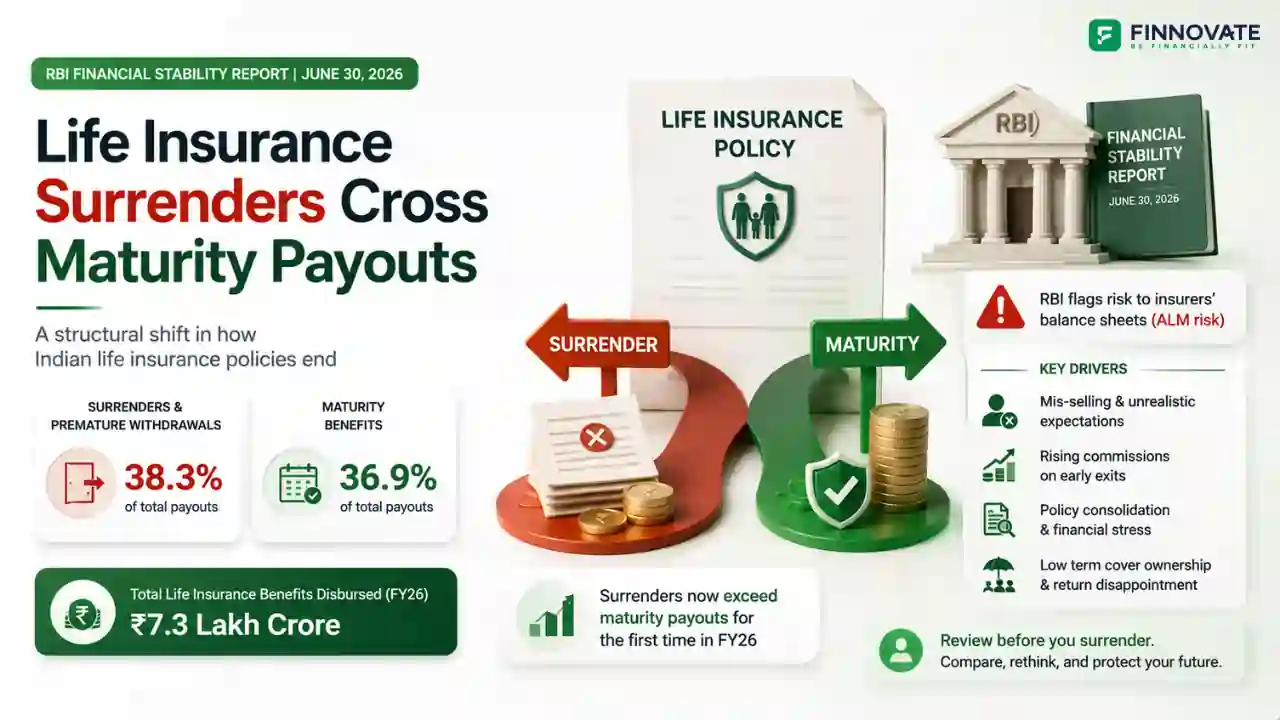

Source: RBI Financial Stability Report, June 30, 2026

The RBI's Financial Stability Report released on June 30, 2026 flagged a structural shift in how Indian life insurance policies end. In FY26, surrenders and premature withdrawals accounted for 38.3% of total life insurance payouts, edging past maturity benefits at 36.9% and death claims at 8.1%. More policyholders are now exiting policies before their term than completing them.

A life insurance surrender is the early termination of a policy before its maturity date, in exchange for a surrender value, a partial payout based on premiums paid and accumulated bonuses. It ends the death benefit immediately and typically returns less than the total premiums paid, especially in the policy's early years. The RBI's concern is not any individual exit; it is that at scale, premature exits disrupt the long-duration assumptions insurers use to manage their balance sheets.

Quick read

Surrenders and premature withdrawals as share of total life insurance payouts, highest category in FY26

Maturity benefits as share of total payouts, now in second place behind surrenders for the first time

Total life insurance benefits disbursed in FY26, up from ₹5 lakh crore in FY22, a 16.1% increase over FY25 alone

An endowment policy, the traditional with-profits life insurance plan, typically attains a surrender value after premiums have been paid continuously for three years. At this point, the policyholder can exit and receive a fraction of total premiums paid plus accumulated bonuses. The longer the policy has run before surrender, the higher the surrender value; in the early years, it is substantially less than total premiums paid.

Endowment policies permit loans against the surrender value, typically up to 90% of the accumulated amount. A meaningful number of premature terminations do not happen through formal surrender: the policyholder takes a loan, then fails to repay, and the policy lapses. The outstanding loan is adjusted against the final settlement, so the policy still ends early, coverage still lapses, and the return still falls well short of what holding to maturity would have delivered.

The RBI FSR explicitly links the surrender trend to mis-selling risk. Traditional endowment policies typically deliver annualised returns of 3% to 6% on premiums paid, rarely disclosed prominently at the point of sale. Policyholders who expected returns comparable to equity mutual funds or fixed deposits often discover the true picture only years in. When expectations meet reality, surrender becomes rational.

Private sector life insurance commission ratios roughly doubled from FY22 to FY26, reaching 9.1%. Higher commissions create stronger incentives for distributors to close new policies rather than service existing ones, which the RBI directly identifies as a driver of acquisition-cost-led mis-selling. IRDAI Chairman Ajay Seth has signalled that distribution reforms, including enhanced mandatory benefit illustrations, are being pursued.

Many households bought life insurance reactively in the early 2000s: under March tax-saving pressure, through employer group schemes, or on a recommendation, without understanding what they were buying. Over two decades this produced scattered portfolios with overlapping cover and poor value-for-cost. Surrendering these and consolidating into properly structured term insurance and investments is financially rational, and it accounts for a meaningful share of FY26 surrender activity.

The RBI's concern is specific and structural: asset-liability mismatch (ALM) risk. Life insurers invest their premium corpus in long-duration assets, deep-maturity government bonds, equity, and infrastructure, on the assumption that premium income stays stable over the full policy tenure of 15 to 30 years. When policyholders exit early at scale, insurers may need to liquidate long-duration assets ahead of schedule to fund payouts, disrupting that duration match.

| Risk Factor | Current Status | RBI's Assessment |

|---|---|---|

| Solvency ratios | Above regulatory minimum across the sector | No immediate distress: sector is financially resilient |

| Surrender trend direction | Surrenders now exceed maturity payouts as the largest category | Near-parity signals structural shift, not a one-off year |

| ALM risk for large insurers | Well-capitalised large players have buffers to manage early exits | Manageable currently but requires monitoring if trend accelerates |

| ALM risk for smaller insurers | Thinner capital buffers; fewer tools to manage duration mismatch | Elevated risk if surrenders accelerate: balance sheet stress possible |

| Commission-driven mis-selling | Private sector commission ratios doubled to 9.1% in FY26 | Directly identified as a risk driver; distribution reform underway |

The RBI's concern is systemic, but at the individual level the FY26 data often reflects rational decisions. Surrendering a policy that was mis-sold or is structurally unsuitable is not a financial error; staying in the wrong policy is. The real question is whether the surrender is happening with a plan for what replaces it, or simply as an exit from something that felt wrong.

Reviewing your existing life insurance portfolio, including coverage adequacy, policy type, and whether what you hold still serves your goals, is part of a complete financial plan. If you have policies you are uncertain about, a structured review can clarify what to keep, what to surrender, and what to replace with.

→ See how Finnovate approaches life insurance as part of a financial planThe crossover of surrenders over maturity payouts in FY26 is not a crisis indicator: solvency ratios remain above minimums and large, well-capitalised insurers have sufficient buffers. But it is a structural signal worth taking seriously, driven by two forces the RBI has named directly: mis-selling amplified by rising commissions, and rational consolidation of policies that were never suitable to begin with.

Both are addressable, one through regulatory reform of distribution incentives and the other through better financial planning at the individual level. The trend will not reverse until the underlying drivers are resolved, and the commission data suggests those drivers are, for now, getting stronger rather than weaker.

Surrendering a life insurance policy means terminating it before maturity and receiving the surrender value, a partial amount based on premiums paid and accumulated bonuses. Cover ends immediately, and in the early years the surrender value is substantially below total premiums paid. Surrender terms vary by insurer and product; verify with your insurer before deciding.

The RBI's FSR points to two drivers: mis-selling, where policyholders discover actual returns of 3% to 6% only years into the policy, and rational consolidation, where households correct decades of scattered, overlapping cover. Rising commission ratios have intensified the first driver. Both are operating simultaneously in FY26.

Insurers invest premium corpus in long-duration assets matched to policy tenures of 15 to 30 years. Large-scale early exits can force insurers to liquidate those assets ahead of schedule, disrupting asset-liability management. Smaller, less-capitalised insurers face the most risk if the trend accelerates.

It depends on the specific policy, how long it has run, and what replaces it. Surrendering a mis-sold or unsuitable policy can be the right call, provided there is a clear replacement plan: adequate term cover for protection and suitable investments for wealth accumulation. Please consult a SEBI-registered investment adviser and a qualified insurance professional before deciding.

Term insurance provides a death benefit if the insured dies within the policy term and pays nothing if they survive; it is pure protection at a relatively low premium. An endowment policy adds a savings component: premiums are higher, and it pays a maturity benefit on survival or a death benefit otherwise. Traditional endowment policies participate in the insurer's profits through bonuses, but their annualised returns are usually lower than separate term insurance plus investment.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any securities or financial instruments. Life insurance data referenced is from the RBI Financial Stability Report dated June 30, 2026, and publicly available news reporting. Surrender value mechanics, loan terms, and policy conditions vary by insurer and product; verify with your insurer before making any decision. Please consult a SEBI-registered investment adviser and a qualified insurance professional before making any decision regarding life insurance policies.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare Term Insurance, Endowment, and ULIP in a clear, unbiased way. Understand costs, co...

Compare family floater vs individual health insurance in India - costs, coverage, pros & c...

Protect income and cashflows first. See why term and health insurance form the base of a s...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...