Bancassurance in India FY26: Banks Earn ₹20,000 Crore and the Risks That Come With It

Indian banks earned over ₹20,000 crore distributing insurance in FY26. HDFC Bank led at ...

28 July 2026

Premiums are rising. Hospital bills vary wildly across cities. And most families still default to “cheapest premium” instead of asking the real question: Which type of health insurance actually fits our family’s risk?

This guide breaks down Family Floater vs Individual plans in simple with examples, trade-offs, and a no-nonsense decision checklist.

(Related reads: Why Insurance Is the Foundation of Financial Planning | What Is Term Insurance? (Explained for Beginners))

Family Floater

One policy with a shared sum insured for all covered members (e.g., spouse + kids). Anyone can use the common pool during the year until it’s exhausted.

Individual Plan

Separate sum insured for each person. Each member gets their own coverage limit, independent of others’ claims.

Example A: 10L Family Floater (2 Adults + 1 Child)

- Hospitalisation #1: Mother claims ₹6L → Remaining pool ₹4L

- Hospitalisation #2 (same year): Father claims ₹5L → Policy pays ₹4L; ₹1L comes from pocket (unless restoration benefit applies - more on that below)

Example B: 5L Individual Plans (5L each for 3 members)

- Hospitalisation #1: Mother claims ₹6L → Policy pays ₹5L; ₹1L from pocket

- Hospitalisation #2 (same year): Father still has his own ₹5L intact; Child also has ₹5L intact

Key idea: Floaters are efficient when claims are infrequent and ages/risks are similar. Individual plans shine when claims are likely or risks differ a lot across members.

| Feature | Family Floater | Individual | Who benefits |

|---|---|---|---|

| Premium efficiency | Often lower total premium for young, low-risk families | Higher total premium when buying per person | Young couple + kids |

| Age-based pricing | Premium based on the oldest member | Premium priced per member | If a large age gap exists, individual avoids loading the whole family |

| Claim frequency impact | Multiple claims can exhaust shared pool | Each person’s cover is ring-fenced | Families with chronic conditions |

| NCB (No-Claim Bonus) | NCB applies to shared pool; a claim can reduce NCB for all | NCB preserved per person | Where one member claims often |

| Restoration benefit | Useful, but rules vary (same illness vs unrelated, once per year, etc.) | Also available on many individual plans | Works for both—check policy wording |

| Portability | Port as a family (admin simpler) | Port per person (customisable) | Depends on future plan changes |

| Room-rent/sub-limits | Same clauses for all members | Can customise per age/person | Tailor for senior parents |

| Upgrades | Upgrading affects entire family | Upgrade selectively | Families with mixed needs |

Tip: Avoid adding senior parents to the same floater. Their age and health can drive up premiums and exhaust the shared pool. Buy a separate senior plan for them.

Focus less on “Does it include 600 procedures?” and more on how the claim amount is calculated.

(For exact numbers, review city, age, hospital preferences, and medical history.)

Simple rule of thumb:

- Floater for young, similar-risk families who value premium efficiency.

- Individual for mixed ages, chronic conditions, or when covering seniors.

- Consider separate senior policies plus a super top-up for the family to scale intelligently.

Scenario 1: Couple 33 & 31, child 2, Mumbai

- Healthy, similar ages → Floater 15L + Super Top-Up to 25L.

- Add NCB protect if budget permits.

- Avoid room-rent caps; choose a plan with big cashless hospitals.

Scenario 2: Couple 40 & 37, parent 64 with diabetes

- Couple + child on Floater 15L.

- Buy a separate senior plan (individual) for the parent with appropriate co-pay.

- Consider super top-up to control costs.

Scenario 3: Couple 36 & 35, one partner with frequent claims

- Move to Individual 10L each to ring-fence coverage + super top-up.

- NCB remains protected for the healthier partner.

(All scenarios are illustrative, not advice.)

For young, low-risk families, a floater often costs less than buying separate individual covers. As ages and risks diverge, individual can be smarter despite a higher premium.

It helps, but read the rules carefully: Some allow restoration only for unrelated illnesses or from the next claim. Don’t rely on it as a guaranteed second cover for the same long hospitalisation.

Usually no. Seniors can drive up premiums and exhaust the shared pool. Buy separate senior plans tailored to their needs.

On a floater, an eligible claim typically reduces the shared NCB. On individual plans, only that member’s NCB is affected.

Yes, via IRDAI portability, if you apply in time (ideally 45–60 days before renewal). Pre-existing waiting credits usually carry over - subject to acceptance by the new insurer.

As a starting point: ₹10–15L for young metro families; ₹7–10L for Tier-2/3. Scale up with age, city costs, family size, and medical history. Use super top-ups to extend limits efficiently.

Disclaimer: This article is for educational purposes only and not a recommendation to buy or sell any insurance product. Finnovate Financial Services Pvt. Ltd. is a SEBI-registered RIA offering unbiased financial planning services.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Indian banks earned over ₹20,000 crore distributing insurance in FY26. HDFC Bank led at ...

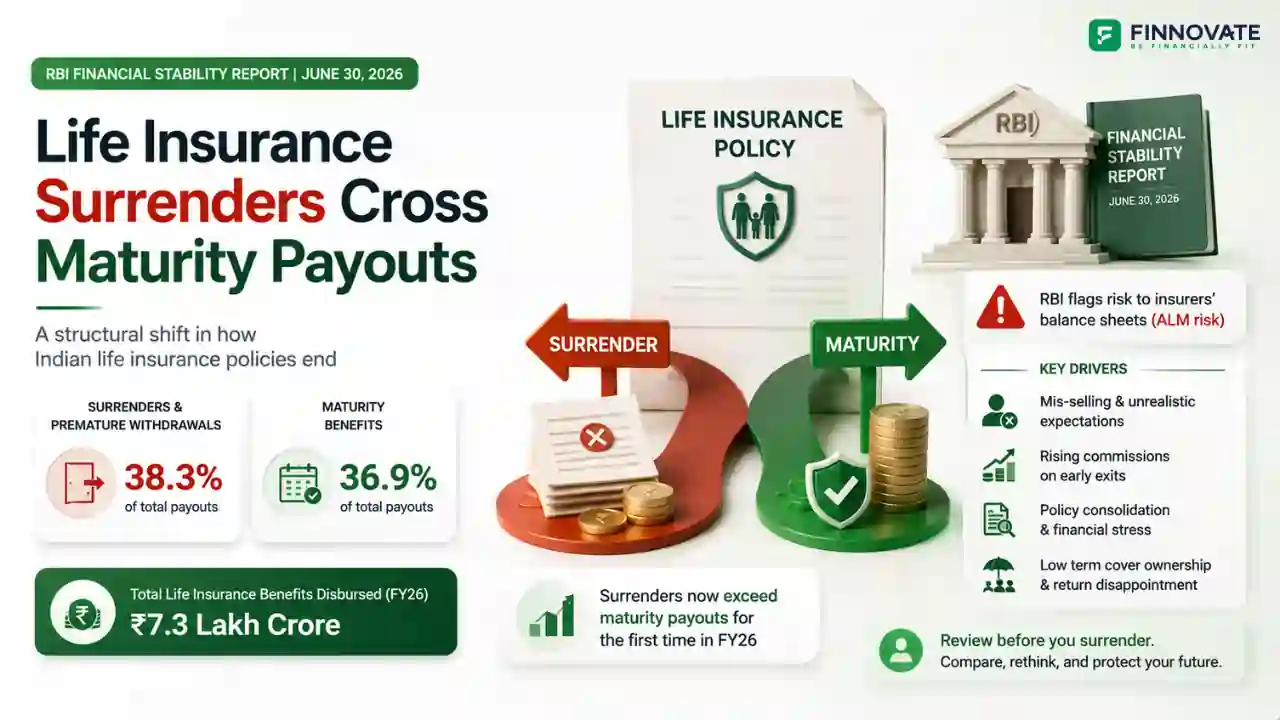

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare Term Insurance, Endowment, and ULIP in a clear, unbiased way. Understand costs, co...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...