Bancassurance in India FY26: Banks Earn ₹20,000 Crore and the Risks That Come With It

Indian banks earned over ₹20,000 crore distributing insurance in FY26. HDFC Bank led at ...

28 July 2026

If one hospital bill or a sudden loss of income can undo years of SIP gains, the first step is obvious: lock the downside before chasing returns. That’s what a well-built plan does - it protects your income and cashflows first, and only then focuses on growth.

(Also read: What Is Term Insurance? (Explained for Beginners))

Compounding needs stability. If your cashflows get hit by a medical emergency or your family’s income stops, investment plans can derail overnight. That’s why a solid plan is built like a three-layer stack:

Emergency Fund → Insurance (Term + Health) → Investments

Without the first two layers, the third can be wiped out when life throws a curveball.

If your income stops, goals still remain - EMIs, school fees, elder care. Term insurance replaces your earning power for your family. It’s pure protection, not an investment.

(Explore: Term Insurance Services)

A single hospitalisation can drain hard-earned savings. Health insurance shields your cashflows from large, sudden expenses and preserves your investment plan from forced redemptions.

(Explore: Health Insurance Services)

If you have a home loan, clinic set-up loan, or have signed as a guarantor, the family shouldn’t be forced to sell assets. An adequate term cover helps keep assets intact.

What it is: A pure risk cover that pays your family a fixed sum assured if you’re not around during the policy term. No maturity value. No returns. Just income replacement.

Rule of thumb for cover:

15–20× your annual income

+ outstanding liabilities (home/education/clinic loans)

− assets already earmarked for dependents

Illustration (not a quote):

A 35-year-old with ₹20L annual income and ₹40L home loan may consider ₹3–4 crore cover, adjusted for goals and existing assets. Buy early to lock a lower premium and longer protection.

Read next: What Is Term Insurance? | How Much Term Insurance Do You Need?

Service page: Finnovate Term Insurance.

What it is: A policy that pays for covered medical costs so your investments don’t get liquidated at the worst time. For families, a family floater is often efficient; in some cases, individual covers make sense (age gaps, medical history).

Key levers to check (often missed):

Baseline thumb rule (illustrative, not advice):

Metro family: ₹10–15 lakh floater as a starting point, scaling with age, city, history, and affordability.

Read next: Family Floater vs Individual Health Insurance

Service page: Finnovate Health Insurance.

Step 1: Build the Emergency Fund

Step 2: Put Insurance in Place

Step 3: Start/Scale Investments

Once the floor is solid, automate investing (SIPs) towards goals: emergency top-ups, education, retirement. This is where compounding shines - because shocks are already covered.

Quick readiness checklist (Yes/No):

“Premiums feel wasted if nothing happens.”

You’re transferring catastrophic risk to an insurer. If a major event never occurs, that’s a good outcome - your plan worked.

“I’m young and healthy.”

That’s exactly when premiums are lowest and approvals easiest. Waiting only increases cost and risk.

“My company cover is enough.”

Employer policies are job-linked, often with low sums insured. Continuity matters. Keep a personal base plan.

Because a major medical bill or loss of income can force you to liquidate investments at the worst time. Insurance shields your plan so compounding stays uninterrupted.

Start with 15–20× annual income, add liabilities, and subtract assets earmarked for dependents. Fine-tune for goals and life stage.

Usually not. It’s job-linked, often low in sum insured, and can end when you switch jobs. Keep a personal base cover for continuity.

Floaters are efficient for young families; individual plans suit large age gaps, senior parents, or specific medical histories. Check room rent caps and sub-limits either way.

Prioritise at least a basic term and health cover first. The emergency fund handles smaller shocks; insurance covers catastrophic events.

Accidental death benefit, critical illness, and waiver of premium are commonly considered - add only if they fit your risks and budget.

Disclaimer: This article is for educational purposes only and not a recommendation to buy or sell any insurance product. Finnovate Financial Services Pvt. Ltd. is a SEBI-registered RIA offering unbiased financial planning services.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Indian banks earned over ₹20,000 crore distributing insurance in FY26. HDFC Bank led at ...

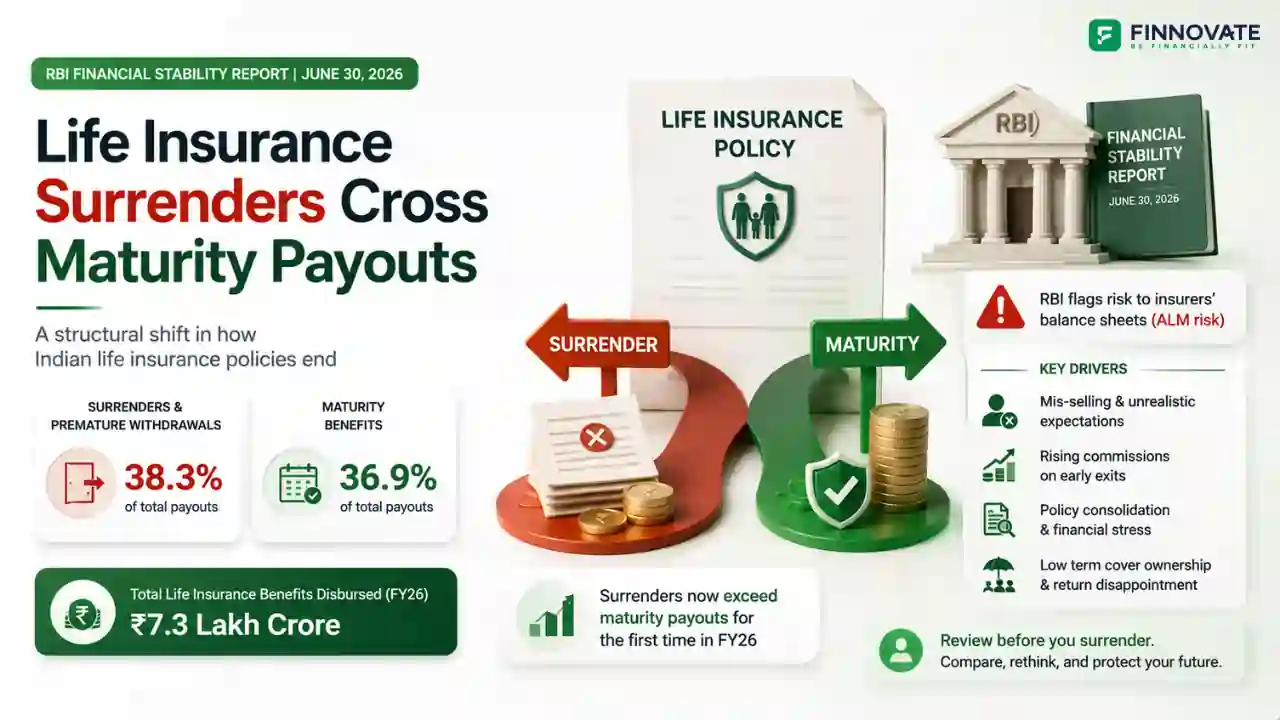

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare Term Insurance, Endowment, and ULIP in a clear, unbiased way. Understand costs, co...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...