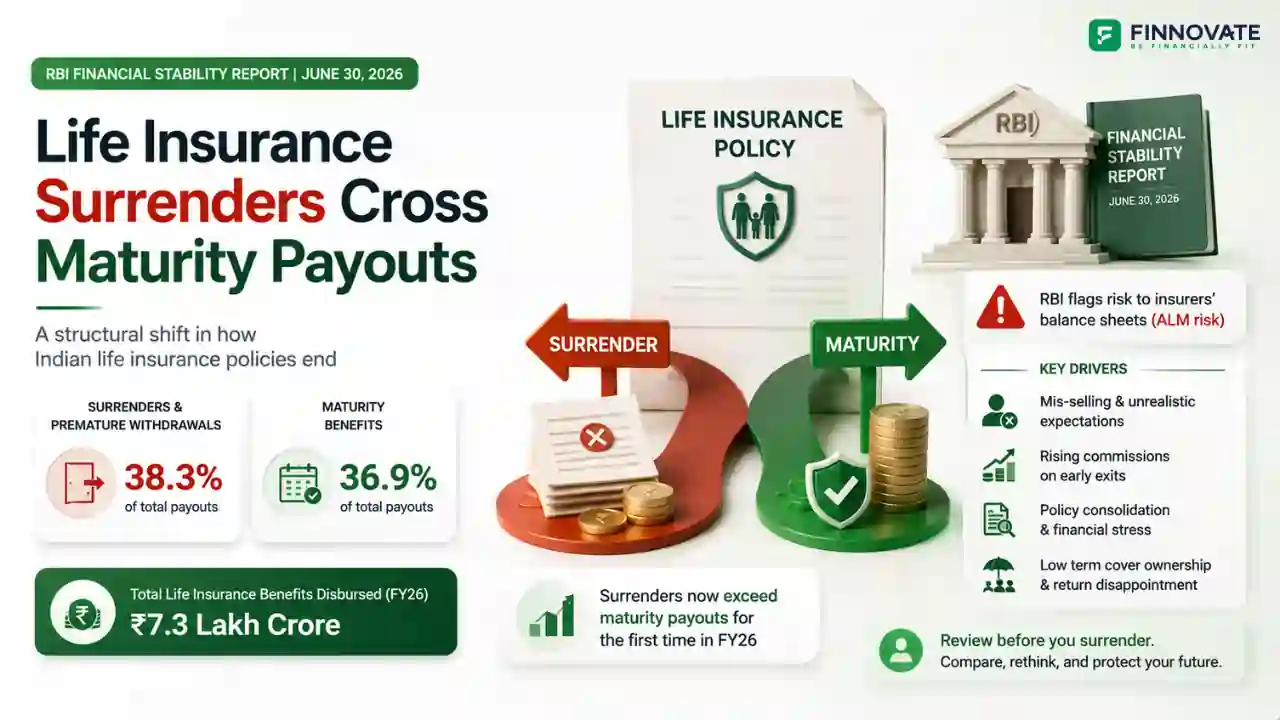

Life Insurance Surrenders Now Exceed Maturity Payouts in FY26

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

07 July 2026

Most buyers look for “something with returns.” But the primary job of life insurance is income protection. If your income stops, your family still needs to pay EMIs, school fees, and living costs. This guide compares Term Insurance, Endowment, and ULIP in simple terms and shows why keeping protection and investing separate usually wins on cover, flexibility, and costs.

(Related reads: What Is Term Insurance? | Why Insurance Is the Foundation of Financial Planning | Family Floater vs Individual Health Insurance)

If your first goal is to safeguard your family’s lifestyle, start with Term. If you want to grow wealth, do it through separate investments (e.g., mutual funds) with clear goals and low costs.

| Feature | Term Insurance | Endowment Policy | ULIP |

|---|---|---|---|

| Primary purpose | Pure risk cover (income replacement) | Forced savings + small cover | Market-linked investing with an insurance wrapper |

| Premium vs Cover | Lowest premium, highest cover | High premium, low cover | Medium–high premium, moderate cover |

| Returns | None (no maturity value) | Low–moderate (guaranteed/declared) | Market-linked (can vary widely) |

| Charges/Costs | Mainly mortality cost (low) | Distribution/admin baked into pricing | Allocation charges, policy admin, fund management charges (FMC), mortality - highest drag in early years |

| Liquidity / Lock-in | Cancel anytime (no value back) | Surrender penalties; lock-ins typical | 5-year lock-in; surrender costs early |

| Transparency & Control | Very clear (cover only) | Opaque returns vs cover trade-off | Fund choices exist but limited; switching rules apply |

| Tax (broad) | 80C on premium; no maturity | 80C; maturity usually under 10(10D)* | 80C; 10(10D) conditions apply (rules vary with premium ratios)* |

| Best for | Everyone who has dependents/liabilities | Very conservative savers who accept low cover and low returns | Investors OK with lock-in, insurer funds, and charge structure |

*Tax rules are subject to change; check current provisions before purchase.

Your premium mostly pays for mortality cost (the cost of providing life cover). Because there’s no investment element, term is cheap for large cover (₹1–3 crore or more).

A large chunk of your premium goes towards a savings/guaranteed component; what’s left for pure insurance is small. Outcome: low sum assured for the high premium paid, plus low-to-moderate maturity value over long periods.

Premium is split across allocation charges, policy admin, fund management charges (FMC), and mortality charges. Early years carry the heaviest drag; compounding is subdued upfront. Fund choice and switching rules limit flexibility versus open-ended MFs.

Note: For high-premium ULIPs (annual premium above ₹2.5 lakh), tax rules introduced in 2021 may treat maturity proceeds as capital gains rather than fully tax-free under Section 10(10D). Confirm tax treatment with product documents and a tax advisor.

These are exceptions, not the default route for most professionals with dependents and liabilities.

- Need a structured plan? Give us a Call

Option A: Term + Invest

- ₹1 crore term cover for a 30–35-year-old is usually a few hundred to ~₹1,000s per month (illustrative).

- The remaining budget goes into goal-based SIPs (equity/debt mix).

- Outcome: high protection + transparent investing with fund choice and easy rebalancing.

Option B: Endowment/ULIP

- The same total budget often buys low cover (far below ₹1 crore).

- Early-year charges/penalties and lock-in reduce flexibility and may drag returns.

- Outcome: neither sufficient protection nor optimal investing.

Takeaway: If your priority is to secure your family and build wealth efficiently, Option A is usually superior.

If you want clarity on how much insurance you actually need and how to structure protection + investments the right way, speak with a Finnovate financial planner.

Book a Free Financial Planning Consultation

No. Term is a risk transfer - you pay a small cost so a large liability (₹1–3 crore+) is covered if the worst happens. If you don’t claim, that’s success, not waste.

Some ULIPs can qualify for 80C and, under certain conditions, favourable 10(10D) treatment. But always compare total costs, lock-in, and fund options against a Term + MF route before deciding.

You can buy Term immediately (to fix protection). For the existing ULIP, weigh surrender charges, remaining lock-in, and fund performance. Sometimes going paid-up or exiting after a milestone is better. Case-by-case.

Run the IRR of the policy vs alternatives. If cover is too low and returns are weak, consider whether continued premiums are justified. Don’t leave your family under-insured.

Disclaimer: This article is for educational purposes only and not a recommendation to buy or sell any insurance product. Tax rules and product features change - please review current regulations and product documents before investing or buying insurance. Finnovate Financial Services Pvt. Ltd. is a SEBI-registered RIA offering unbiased financial planning services.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare family floater vs individual health insurance in India - costs, coverage, pros & c...

Protect income and cashflows first. See why term and health insurance form the base of a s...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...