Equity Fund AUM June 2026: Price Moves Did More Work Than Flows

Active equity fund AUM rose 3.3% to ₹37.34 lakh crore in June 2026. Price accretion of �...

15 July 2026

SEBI has announced a major update to India’s mutual fund categorisation framework through a circular dated February 26, 2026.

Two parts of this update stand out for long-term, goal-based investors:

1. SEBI has introduced a new category called Life Cycle Funds.

2. SEBI has discontinued the Solution Oriented Schemes category that previously covered retirement and children-oriented schemes as a distinct bucket.

This article breaks down what changed, how Life Cycle Funds are structured, what the key rules are (including naming and exit loads), how the glide path works, what existing investors may see next, and how Life Cycle Funds differ from commonly used fund types.

Here’s the change in one view.

| Topic | Earlier | Now |

|---|---|---|

| Goal-focused category | “Solution Oriented Schemes” category existed (children and retirement) | This category is discontinued |

| New category | Not available | Life Cycle Funds introduced |

| Product structure | Schemes used varied structures under solution-oriented labels | A structured maturity + glide path design is formally introduced as a category |

| Existing solution-oriented schemes | Fresh purchases/SIPs were allowed (scheme-specific) | Existing schemes under solution-oriented category will stop fresh subscriptions and be merged/rationalised as per SEBI framework and approvals |

SEBI’s circular - Categorization and Rationalization of Mutual Fund Schemes

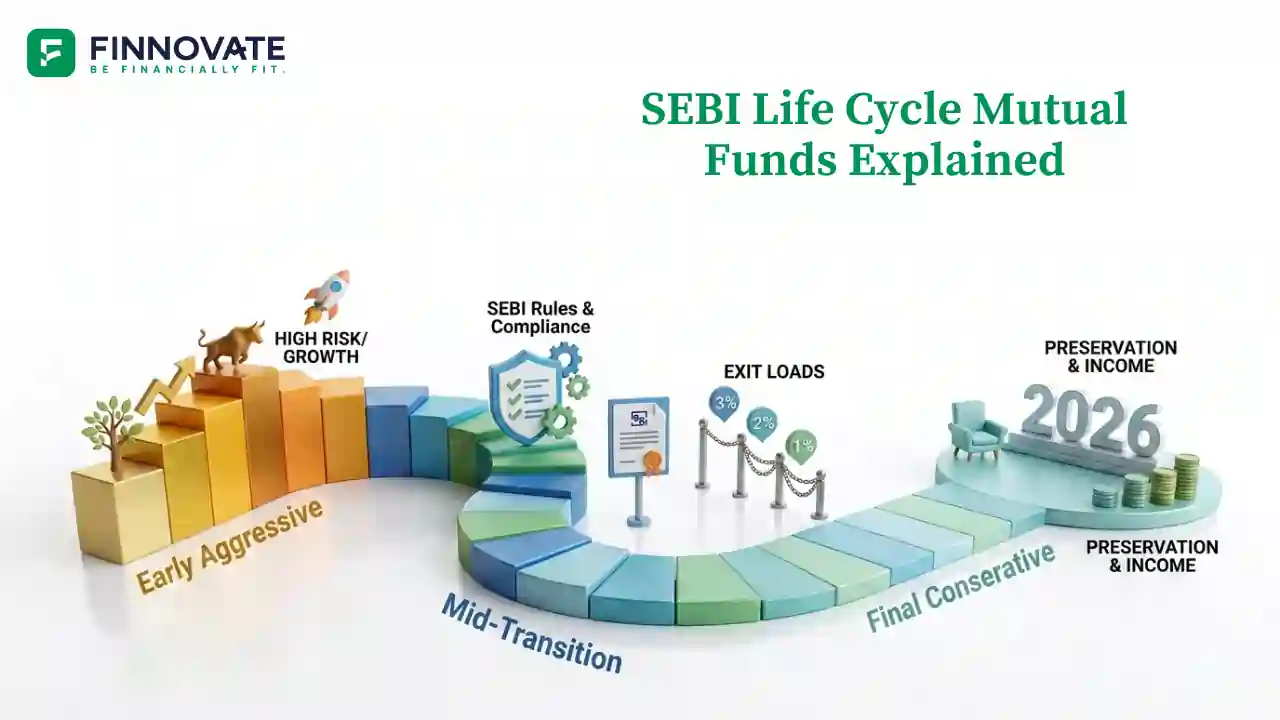

A Life Cycle Fund is a new mutual fund category designed for goal-based investing, built around two features:

1. Pre-determined maturity (a defined target maturity such as 5 years, 10 years, up to 30 years)

2. A glide path, meaning the fund’s asset mix changes as it gets closer to maturity, typically shifting from higher growth exposure earlier to higher stability exposure closer to maturity.

These are described as open-ended schemes, but their design is tied to a maturity year and time-to-maturity-based allocation approach.

Life Cycle Funds are structured with maturities from 5 years to 30 years, in multiples of 5 (5/10/15/20/25/30).

SEBI’s framework requires the maturity year to be included in the scheme name, for example “Life Cycle Fund 2045” or “Life Cycle Fund 2055.”

This rule is meant to make the investment horizon easier to identify at a glance.

Reporting on the circular notes that Life Cycle Funds will follow the benchmark framework prescribed for Multi Asset Allocation Funds.

Coverage of the SEBI framework indicates Life Cycle Funds can invest across equity and debt, and also include permitted exposure to instruments such as gold and silver ETFs, along with permitted exposures like InvITs and ETCDs (as applicable in the framework).

SEBI has prescribed a graded exit load structure for Life Cycle Funds, as widely reported:

| When units are redeemed | Exit load |

|---|---|

| Within 1 year | 3% |

| Within 2 years | 2% |

| Within 3 years | 1% |

Reporting also notes that AMCs have a cap on the number of Life Cycle Funds they can keep open for subscription at a time.

Coverage mentions provisions around handling schemes when remaining maturity becomes very low, including the possibility of merging into the nearest maturity option, subject to the defined process.

The glide path is the central design feature of this category.

The idea is that the portfolio gradually adjusts based on “time left to maturity”:

This structure aims to reduce the impact of large market moves closer to the maturity year.

The SEBI circular provides asset allocation ranges for Life Cycle Funds based on “years to maturity” and the fund’s maturity bucket (5, 10, 15, 20, 25, or 30 years). Below is the prescribed glide-path banding shown in the circular table.

| Years to maturity | Investment in Equity (%) | Investment in Debt (%) | Investment in Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 15–30 years | 65–95 | 5–25 | 0–10 |

| 10–15 years | 65–80 | 5–25 | 0–10 |

| 5–10 years | 50–65 | 5–25 | 0–10 |

| 3–5 years | 35–50 | 25–50 | 0–10 |

| 1–3 years | 20–35 | 25–65 | 0–10 |

| < 1 year | 5–20 | 25–65 | 0–10 |

Notes:

Exposure in debt instruments shall be limited to AA & above rated instruments with residual maturity less than the target maturity of the scheme.

ETCDs shall be based only on Gold/Silver.

For years to maturity less than 5 years, all Life Cycle Funds may take equity arbitrage exposure up to 50% in addition to the investment range specified for equity while ensuring that total investment in equity and equity related instruments remains within 65% - 75% in such schemes (as defined above).

Glide path concept (illustration only)

This table explains the concept. It is not a return promise.

| Time left to maturity | Typical portfolio character |

|---|---|

| 15–30 years | Higher growth orientation |

| 5–15 years | More balanced mix |

| 0–5 years | Higher stability orientation |

Some explainers have also reported example equity ranges across stages (for instance, equity being higher in long-horizon stages and reducing closer to maturity). These are typically presented as glide-path ranges within the framework rather than a guarantee of returns.

SEBI has discontinued the “Solution Oriented Schemes” category and reports indicate:

What investors may see next typically includes:

This table keeps it factual and structural.

| Feature | Old solution-oriented category | New life cycle category |

|---|---|---|

| Asset allocation design | Could vary by scheme, often not maturity-linked in a standard way | Explicit glide path design linked to time-to-maturity |

| Goal identification | Label-based (retirement/children), scheme-specific | Maturity-year-based naming (Life Cycle Fund 2045 etc.) |

| Exit load | Scheme-specific | Graded exit loads in early years, as prescribed in the framework |

| What happens now | Category discontinued | New category introduced |

This is a facts-only comparison to reduce confusion.

| Feature | Life Cycle Fund | Balanced Advantage Fund (BAF) | Aggressive Hybrid Fund | Target maturity debt fund |

|---|---|---|---|---|

| Pre-defined maturity | Yes (5–30 years in steps of 5) | No | No | Yes (series-based) |

| Asset mix changes with time-to-maturity | Yes, via glide path | Changes based on model/valuation approach, not maturity-year design | Typically within a relatively fixed hybrid mandate | Driven by debt maturity profile |

| Name indicates maturity year | Yes (maturity year in name) | No | No | Often indicates maturity/series |

| Exit load structure | Graded structure reported (3/2/1% in first 3 years) | Scheme-specific | Scheme-specific | Scheme-specific |

| Core design idea | Goal-year and time-to-maturity linked structure | Dynamic allocation style | Hybrid bracket | Maturity-driven debt strategy |

The exit load structure (3%/2%/1% in the first 1/2/3 years) is a prominent part of how this category is positioned, and it makes the cost of early redemption easy to see upfront.

The glide path means the portfolio’s risk profile changes over time inside the same scheme, based on time-to-maturity.

When a mutual fund rebalances inside the scheme, investors typically face capital gains tax when they redeem/sell their units, not because the fund manager rebalanced. Several explainers highlight this as one reason such a structure can reduce the need for investor switches across different funds for rebalancing purposes.

(Actual tax outcomes depend on when and how the investor redeems units and on prevailing tax rules.)

This update is about product structure and standardisation. It does not change the basic reality that returns depend on market performance, underlying holdings, and costs.

Take the FinnFit Test

If you want a structured view of your goals, timelines, and risk comfort, take the FinnFit Test.

It helps map goals to time horizons so investing stays linked to real-life milestones.

SEBI’s Feb 26, 2026 circular introduces Life Cycle Funds as a maturity-year-based, glide-path mutual fund category and discontinues the older solution-oriented category. For investors, the key change is a more standardised “goal-year linked” structure, where the fund name reflects the maturity year and the portfolio adjusts based on time-to-maturity, along with a clearly defined early-exit load structure.

No. SEBI has discontinued the solution-oriented category (which included retirement and children schemes as a category) and introduced Life Cycle Funds as a new category with a maturity + glide path structure.

Reported maturities range from 5 years to 30 years, in multiples of 5.

SEBI’s framework requires the maturity year in the nomenclature (for example, “Life Cycle Fund 2045”), to make the horizon easier to identify.

As reported, the exit load is graded: 3% within 1 year, 2% within 2 years, and 1% within 3 years.

No. The category defines structure (maturity + glide path), not returns. Returns still depend on markets and holdings.

These are described as open-ended schemes, so SIP availability will typically depend on the AMC’s scheme features and platform availability once schemes are launched.

Existing schemes in that category are expected to stop fresh subscriptions and then be merged/rationalised into similar schemes, subject to SEBI’s process and approvals.

Not necessarily. Even within one category, AMCs can differ in implementation choices, holdings, costs, and portfolio construction as long as they stay within the framework.

Disclaimer: This article is for informational purposes only and is based on SEBI’s circular dated February 26, 2026 and related reporting. It does not constitute investment advice or a recommendation. Please review scheme documents and consult a SEBI-registered professional for decisions specific to your situation.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Active equity fund AUM rose 3.3% to ₹37.34 lakh crore in June 2026. Price accretion of �...

Passive fund inflows rebounded to ₹16,724 crore in June 2026, with gold and silver ETFs ...

Equity fund folios grew 22.96% CAGR and AUM 29.69% over 3 years. See which of the 11 categ...

Active equity MF inflows fell 40.4% in May 2026 to ₹22,908 crore, but still drove more A...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...