Which Equity Fund Categories Grew the Fastest Over 3 Years?

Equity fund folios grew 22.96% CAGR and AUM 29.69% over 3 years. See which of the 11 categ...

08 July 2026

Last reviewed: May 2026

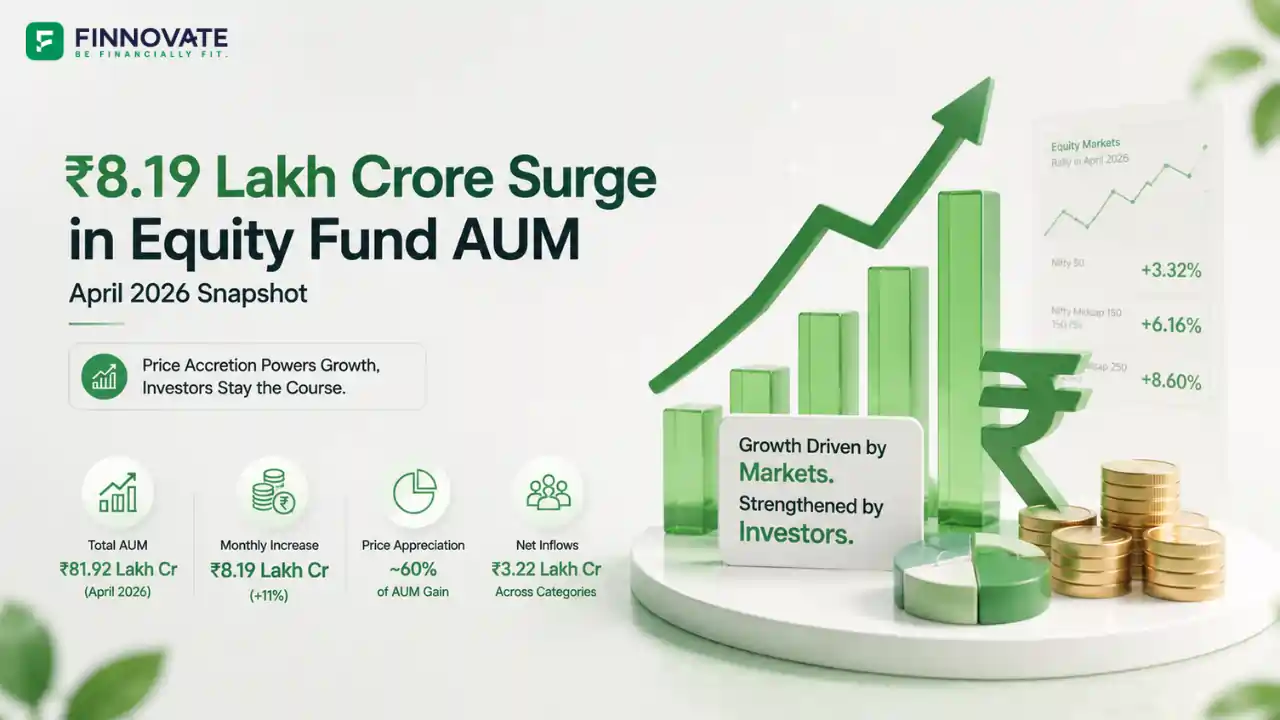

The mutual fund industry's total AUM jumped 11% in April 2026, from ₹73.73 lakh crore at March end to ₹81.92 lakh crore at April end. That is an ₹8.19 lakh crore increase in a single month. The number is striking, and it requires a specific explanation: most of this gain was not driven by fresh investor money. It was driven by rising market prices on existing holdings.

The breakdown tells the story clearly:

This is the mirror image of March 2026. In March, price damage dominated as Nifty fell sharply, reducing AUM even as investors kept putting money in. April reversed that pattern, with midcap and smallcap indices rallying sharply and lifting the value of existing equity fund holdings across the industry.

| Metric | April 2026 | March 2026 | Change |

|---|---|---|---|

| Industry AUM | ₹81.92 lakh crore | ₹73.73 lakh crore | +11% MoM |

| Industry AAUM | ₹81.94 lakh crore | ₹79.46 lakh crore | +3% MoM |

| Equity net inflows | ₹38,440 crore | ₹40,450 crore | -5% MoM |

| SIP contribution | ₹31,115 crore | ₹32,087 crore | -3% MoM |

| Debt fund flows | +₹2.47 lakh crore | -₹2.94 lakh crore | Reversal |

| Hybrid fund flows | +₹20,565 crore | -₹16,538 crore | Reversal |

| Passive fund flows | ₹20,082 crore | ₹30,767 crore | -35% MoM |

| BSE Midcap monthly return | +13.81%* | - | - |

| BSE Smallcap monthly return | +19.61%* | - | - |

When mutual fund AUM changes in a month, the change comes from two sources: fresh money flowing in or out, and the change in market value of existing holdings due to price movements. The second component is price accretion in a rising market and price damage in a falling market.

In April 2026, both components were positive but their relative sizes tell the real story. Net flows across all categories contributed ₹3.22 lakh crore to the AUM gain. The remaining ₹4.97 lakh crore came from price appreciation on existing holdings. The mid and small cap rally in April was the primary engine.

This framework matters for how monthly AUM numbers should be interpreted. A large AUM increase does not always mean a large inflow. In April 2026, it primarily means existing equity fund portfolios became more valuable because markets rose. The inverse was visible in March 2026: investors kept putting ₹40,450 crore into equity funds, but AUM fell because price damage on existing holdings overwhelmed those inflows.

What this means: When your mutual fund portfolio shows a higher value in April, most of that increase came from the market going up, not from your SIP contribution for the month. Price accretion is real wealth, but it is also reversible if markets fall.

Net equity inflows of ₹38,440 crore were 5% below March's ₹40,450 crore. This headline moderation conceals important category-level movements that a single number cannot capture.

| Equity Category | April 2026 (₹ Cr) | March 2026 (₹ Cr) | MoM | YoY vs Apr 2025 |

|---|---|---|---|---|

| Flexi Cap | 10,147.85 | 10,054.12 | +0.9% | - |

| Small Cap | 6,885 | 6,263 | +10% | +72% |

| Mid Cap | 6,551 | 6,063 | +8% | +98% |

| ELSS | (567) | (437) | Outflow | Seasonal |

| Dividend Yield | (20.58) | - | Outflow | - |

| Total Equity | 38,440 | 40,450 | -5% | +58% |

Flexi Cap funds led equity inflows for the second consecutive month at ₹10,147 crore, maintaining momentum above the ₹10,000 crore threshold. The category has now emerged as the largest equity mutual fund segment by AUM at ₹5.59 lakh crore. Its appeal in the current environment lies in structural flexibility: fund managers can allocate across large, mid, and small cap stocks without fixed mandates, allowing them to move where conditions are most favourable in a volatile market.

Small Cap and Mid Cap both grew against the headline equity flow direction. Small Cap inflows rose 10% MoM to ₹6,885 crore and Mid Cap rose 8% to ₹6,551 crore. On a YoY basis, Small Cap inflows are 72% higher and Mid Cap inflows are 98% higher than April 2025. This sustained directional growth reflects performance-led confidence: investors are directing new money toward segments that have been outperforming.

ELSS net outflows of ₹567 crore reflect a seasonal pattern rather than a fundamental shift. The three-year lock-in on ELSS investments made in April 2023 completes in April 2026, and some investors redeem on lock-in completion. April ELSS redemption pressure is a calendar event that repeats reliably each year.

The mid and small cap rally in April 2026 was exceptional in its magnitude. Midcap and smallcap benchmarks rose sharply, generating large absolute gains in a single month.

If a Small Cap fund had ₹100 crore of AUM at March end, and the underlying index rose 15-20%, that fund's AUM would be approximately ₹115-120 crore at April end from price appreciation alone, before accounting for any new inflows or redemptions. Across an industry where small and mid cap category AUMs run into tens of lakh crore, this mathematics produces very large absolute AUM gains from price accretion.

Flexi Cap funds, which hold substantial mid and small cap exposure given their dynamic allocation mandate, benefited correspondingly from this price accretion. Sectoral and thematic funds with concentrated mid cap positions also saw AUM rise substantially from market appreciation alone.

The Large Cap segment, more closely correlated with Nifty 50, saw comparatively modest price accretion relative to mid and small cap categories. This created a visible divergence in AUM behaviour: categories with higher mid and small cap exposure grew their AUM faster in April, not because they attracted more flows, but because the underlying assets appreciated more sharply.

Debt funds saw a ₹2.47 lakh crore inflow reversal in April after ₹2.94 lakh crore of outflows in March. The pattern repeats reliably every year: March sees large corporate debt redemptions for advance tax payments and financial year-end liquidity management, and April sees that money return.

A large part of the April debt inflows went into liquidity and shorter-duration categories:

Long Duration Fund, Gilt Fund, Dynamic Bond Fund, and Banking and PSU Fund all remained in outflow, showing continued caution about taking longer-duration interest-rate risk. The April debt reversal is mainly a normalisation of cash management flows, not a broad shift in favour of duration investing.

Hybrid funds reversed from ₹16,538 crore of outflows in March to ₹20,565 crore of inflows in April. This too reflects the March year-end distortion unwinding. The back-to-normal pattern in hybrid flows confirms that March was the anomaly, and April is closer to the underlying steady-state demand for balanced and dynamic allocation strategies.

What this means: The dramatic numbers in debt and hybrid, whether last month's outflows or this month's inflows, are largely institutional cash management in action. Retail SIP investors in hybrid funds experienced neither the March shock nor the April reversal in a meaningful way.

Three things are worth understanding clearly when monthly AUM numbers are dominated by price accretion rather than fresh flows.

When existing holdings appreciate, the AUM of the fund rises but the investor's average cost of acquisition does not change. A sharp small cap rally in April benefits investors in proportion to their existing holding, not their April SIP. The investor who has been running a SIP for three years benefits more from this appreciation than someone who started in March 2026. The AUM number is industry-level; the return is individual-level.

If AUM sits at ₹81.92 lakh crore at April end because of a price surge, a flat or declining market in May will show AUM moderation even if inflows remain strong. The headline number obscures the flow reality in both directions. Reading AUM in isolation from market performance leads to misinterpretation of investor behaviour.

Small Cap inflows have grown for several consecutive months, and the category's benchmark rallied sharply in April. When both fresh flows and market appreciation move in the same direction for an extended period, concentration risk and valuation risk in the category typically build simultaneously. The data does not tell investors whether current valuations are stretched. It tells them that both price and flows have moved in the same direction for several months. Please consult a SEBI-registered investment adviser before making any portfolio decisions based on category flow or performance trends.

Price accretion in April lifted portfolios with mid and small cap exposure. Whether that exposure is sized correctly for your goals, time horizon, and risk tolerance is worth reviewing. We can walk through your portfolio's category allocation in a 30-minute call.

Book a free callThe 11% month-on-month increase to ₹81.92 lakh crore was primarily driven by price accretion: rising market prices on existing equity holdings, particularly in mid and small cap segments, increased the value of the industry's existing AUM. Midcap and smallcap benchmarks rallied sharply in April. Fresh net flows contributed ₹3.22 lakh crore of the ₹8.19 lakh crore gain. The remaining gain came from mark-to-market price appreciation on holdings that were already in the fund before April began.

Price accretion refers to the increase in the market value of a mutual fund's existing holdings due to rising asset prices. When a fund holds equities worth ₹100 crore and those equities rise 10% in value, the fund's AUM becomes ₹110 crore without any fresh investor money flowing in. This is price accretion. It works in reverse too: in March 2026, Nifty fell sharply and price damage reduced AUM even as investors continued putting money in through SIPs and lump sum investments.

The 5% month-on-month dip from ₹40,450 crore to ₹38,440 crore reflects a normalisation from an elevated March, not a structural pullback. April's ₹38,440 crore is 58% higher than April 2025's ₹24,269 crore on a year-on-year basis. Small Cap and Mid Cap flows both grew month-on-month. The headline 5% dip is a single-month comparison against a particularly strong March, and the YoY data gives a more reliable picture of directional health.

Midcap and smallcap benchmarks rallied sharply in April, generating strong returns for investors already in these categories. When a segment delivers strong recent performance, it tends to attract additional allocations from investors seeking to participate in that trend. Small Cap inflows are 72% higher and Mid Cap inflows are 98% higher on a YoY basis. Please consult a SEBI-registered investment adviser before making allocation decisions based on recent category performance, as past returns do not indicate future outcomes.

March sees large corporate debt redemptions for advance tax payments and financial year-end liquidity needs, a calendar-driven pattern that repeats every year. In April, that money returns, primarily to short-duration instruments such as liquid, overnight, and money market funds. The ₹2.47 lakh crore April inflow is a normalisation of this annual cycle. The fact that long-duration debt funds remained in outflow confirms this was liquidity management, not a shift in duration conviction.

Ten years ago in April 2016, total industry AUM was ₹14.22 lakh crore. The current figure represents a nearly sixfold increase. Five years ago in April 2021, AUM was ₹32.38 lakh crore, and the current level represents a 2.5-fold increase in five years. These are long-term structural growth figures driven by increasing retail participation, SIP habit formation, and compounding returns. Monthly fluctuations driven by price accretion or price damage are part of this long-term journey.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any securities or financial instruments. Data sourced from AMFI monthly report April 2026 and AMFI official press release dated May 12, 2026. BSE index return data from publicly available sources. The price accretion estimate is approximate, calculated as total AUM change minus estimated net flows across categories. Past AUM growth, market performance, and flow patterns are not indicative of future outcomes. No investment decision should be made based solely on the contents of this article. Please consult a SEBI-registered investment adviser or qualified financial professional before making any investment decision. Mutual fund investments are subject to market risks.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Equity fund folios grew 22.96% CAGR and AUM 29.69% over 3 years. See which of the 11 categ...

Active equity MF inflows fell 40.4% in May 2026 to ₹22,908 crore, but still drove more A...

Passive fund net inflows hit just ₹362 crore in May 2026 despite 33% folio and 25% AUM g...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...