FIRE Planning for IT Professionals in India: The Career Cliff Changes Everything

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

12 May 2026

The standard retirement age in India is 60. Retiring at 50 means funding 35 to 40 years of life without a salary.

That single fact changes everything: the corpus required, the withdrawal rate needed, and the risks that matter most. A 20-year conventional retirement and a 35-year early retirement are not the same financial problem. They require different numbers and different structures.

If you want a deeper background on the FIRE concept itself, FIRE in India Explained: Meaning, Math and How to Start covers the full picture.

There are three big shifts driving this:

The question is not "Is early retirement allowed?" It is "What does it actually require?"

There is no single number that works for everyone. But there are frameworks that help you land on a figure specific to your situation.

Globally, you'll hear about the "4% rule":

This came from historical US data. In India, this can be too optimistic because:

So many planners lean towards a more conservative range:

Here is what that looks like in rupees across different expense levels and timelines:

| Monthly Expense Today | Years to Age 50 | Expense at 50 | Corpus at 4% WR | Corpus at 3.5% WR |

|---|---|---|---|---|

| Rs 75,000 | 10 years | Rs 1.34L | Rs 4.03 crore | Rs 4.61 crore |

| Rs 75,000 | 15 years | Rs 1.80L | Rs 5.39 crore | Rs 6.16 crore |

| Rs 75,000 | 20 years | Rs 2.41L | Rs 7.22 crore | Rs 8.25 crore |

| Rs 1 lakh | 10 years | Rs 1.79L | Rs 5.37 crore | Rs 6.14 crore |

| Rs 1 lakh | 15 years | Rs 2.40L | Rs 7.19 crore | Rs 8.22 crore |

| Rs 1 lakh | 20 years | Rs 3.21L | Rs 9.62 crore | Rs 11.00 crore |

| Rs 1.5 lakh | 10 years | Rs 2.69L | Rs 8.06 crore | Rs 9.21 crore |

| Rs 1.5 lakh | 15 years | Rs 3.59L | Rs 10.78 crore | Rs 12.33 crore |

| Rs 1.5 lakh | 20 years | Rs 4.81L | Rs 14.43 crore | Rs 16.49 crore |

To get a clearer handle on your own financial independence number:

Inflation is the silent enemy of every early retirement plan. Even at moderate long-term inflation:

Planning to retire at 50 and live to 85 or 90 means the corpus must support continuously rising expenses, not a flat number. Investment returns after tax must, on average, stay above inflation. That is why equity exposure is not optional in an early retirement journey.

Reaching this corpus by age 50 requires a structured approach across three phases. Each has a savings rate target, an allocation approach, and a corpus milestone that signals whether the trajectory is on track.

Maximise SIP amounts after every salary increment. Term insurance and adequate health cover must be in place before increasing investment exposure. This phase is where the compounding runway is longest and the cost of delay is highest.

Map existing investments to the retirement corpus target from the table above. Calculate the gap. Begin building the short-term liquidity bucket from salary surplus rather than by selling equity.

Run the withdrawal rate stress test. Confirm the healthcare buffer is funded separately. Validate the three-bucket structure is in place before the retirement date. Clear outstanding high-cost debt before exiting salary income.

For a structured view of how asset allocation shifts as you approach retirement, the Finnovate guide covers the transition from accumulation to drawdown across each decade.

Stripping away all jargon, early retirement rests on three pillars: save aggressively, spend consciously, and invest smartly.

To retire 10-15 years earlier than usual, you cannot save like a conventional investor.

The more you save, the less you need to depend on high returns. High savings also give you a buffer if markets underperform for a few years. This means keeping EMIs under control, avoiding too many long-term fixed commitments, and resisting unnecessary lifestyle upgrades when income rises.

The gap between income and expenses is where early retirement is born. The 5-5-5 Rule for Early Retirement is a useful mental framework to structure this thinking.

Frugality for early retirement is not about suffering. It is about being intentional: spend freely on what genuinely matters, cut ruthlessly on what does not.

To support 30-40 years of retirement, money must grow faster than inflation. That means a high allocation to equity in the building phase and a gradual shift toward balanced or income-oriented portfolios as age 50 approaches.

The framework for managing withdrawals over a 35-year retirement is the three-bucket strategy. The diagram below shows how it works:

Also important: not over-tying net worth into real estate. Property in India is hard to sell quickly, often gives low rental yield (2% to 3% net), and comes with maintenance and tax costs. Real estate can be part of the plan, but it should not be the only plan.

A 35-year retirement is exposed to risks that a 20-year conventional retirement manages more easily. Three carry the most financial consequence for someone retiring at 50.

What Rs 1 lakh per month becomes in 30 years at 6% inflation. A flat withdrawal plan depletes the corpus significantly faster than an inflation-adjusted one. The post-retirement portfolio must retain partial equity exposure throughout to generate returns above inflation.

Annual medical inflation in India, materially faster than general inflation. Early retirees lose employer group health cover at exactly the point when health costs start rising. A dedicated medical buffer of Rs 35 to 50 lakh in liquid instruments sits outside the main corpus and should not be merged with it.

The reduction in corpus longevity from retiring in a year with a 25% to 30% equity drawdown versus a normal market year. The order of returns during the withdrawal phase matters as much as the long-term average. A 2 to 3-year liquidity buffer in non-equity instruments is the structural protection against this risk.

The bucket strategy divides the retirement corpus into three portions, each with a different time horizon and purpose. It is the most practical structure for managing a 35-year withdrawal period without reacting to market volatility.

Liquid mutual funds, savings accounts, short-duration debt funds. This bucket absorbs all withdrawals for the first 3 years. A market downturn in year one or two does not require selling equity. When depleted, it is refilled from the medium-term bucket.

Debt mutual funds, fixed deposits, SCSS, hybrid funds. Provides cash flow visibility for years 4 to 10 and periodically refills the short-term bucket. Modest returns above inflation without market exposure. This bucket is what allows the long-term equity bucket to remain invested through full market cycles.

Equity mutual funds, index funds, NPS equity component. Remains invested through all market conditions. A retiree at 50 who is now 60 still has 25 years of retirement ahead. This bucket is what ensures the corpus does not run out in the final decades of a 35-year retirement.

For a detailed walkthrough of how the bucket strategy works in India, the Finnovate guide covers instrument selection and bucket sizing in full.

Retiring at 50 is a 35-year plan. The FinnFit test shows whether your Investment, Goal Planning, and Insurance pillars are aligned to get you there. Or book a call to map your specific numbers.

Taking the 4% rule as a guarantee or assuming 25x expenses is automatically safe in India. A 35-year Indian retirement calls for 3% to 3.5% withdrawal and a 30x to 33x corpus. Using 25x underestimates the required corpus by 20% to 35%.

Multiple properties for rental income generate net yields of just 2% to 3% after maintenance, vacancy, and taxes. Over a 35-year retirement, a financial asset portfolio compounds significantly ahead. Illiquidity is the deeper risk: a single year's cash flow need cannot be met without a property transaction.

Dropping term life or health cover at age 45 to 48 removes protection at precisely the point it becomes expensive to replace. One major uninsured health event can liquidate 3 to 5 years of retirement savings. The cost of maintaining cover through to 50 is materially smaller than the corpus it protects.

LTCG on equity above Rs 1.25 lakh per year is taxed at 12.5%. FD interest is taxed at full slab rate. A corpus built tax-efficiently can be undermined at withdrawal if redemptions are not sequenced. SWP routing and LTCG threshold management materially improve net retirement income.

Retiring early is a long project. If the journey feels like punishment, you're unlikely to stick to it.

This keeps motivation high and reduces the feeling that "life is on hold till I retire". For more perspective on why early planning helps both now and later: 10 Benefits of Starting Retirement Planning Early.

You're not denying yourself. You're choosing fewer impulse buys today in exchange for time freedom and flexibility at 50. That mindset shift makes it easier to say no to lifestyle inflation.

Five questions. Each references a specific number or threshold from this article. A reader who can answer all five with data rather than feelings has done the structural work.

If two or more of these produce uncertainty rather than a number, the gap is structural. That is precisely what an advisory conversation is designed to surface and resolve.

Yes, it is possible. But it is not an outcome of one lucky stock pick, one mutual fund choice, or a quick fix started at 48.

It is a 15-25 year project, built on high savings, thoughtful investing, and realistic assumptions, protected with insurance, buffers, and flexibility. The corpus figures in this article are large. The timeline to build them is longer than it feels. A 30-year-old starting today with a consistent 35% savings rate has more time working in their favour than a 45-year-old with a larger current salary. The arithmetic rewards starting early more than earning more.

For further reading on the strategy side:

Retiring at 50 is not just a corpus question. It is a structure question. A SEBI-registered adviser can run the full retirement readiness check for your specific numbers: corpus, withdrawal rate, healthcare buffer, tax efficiency at withdrawal, and bucket allocation.

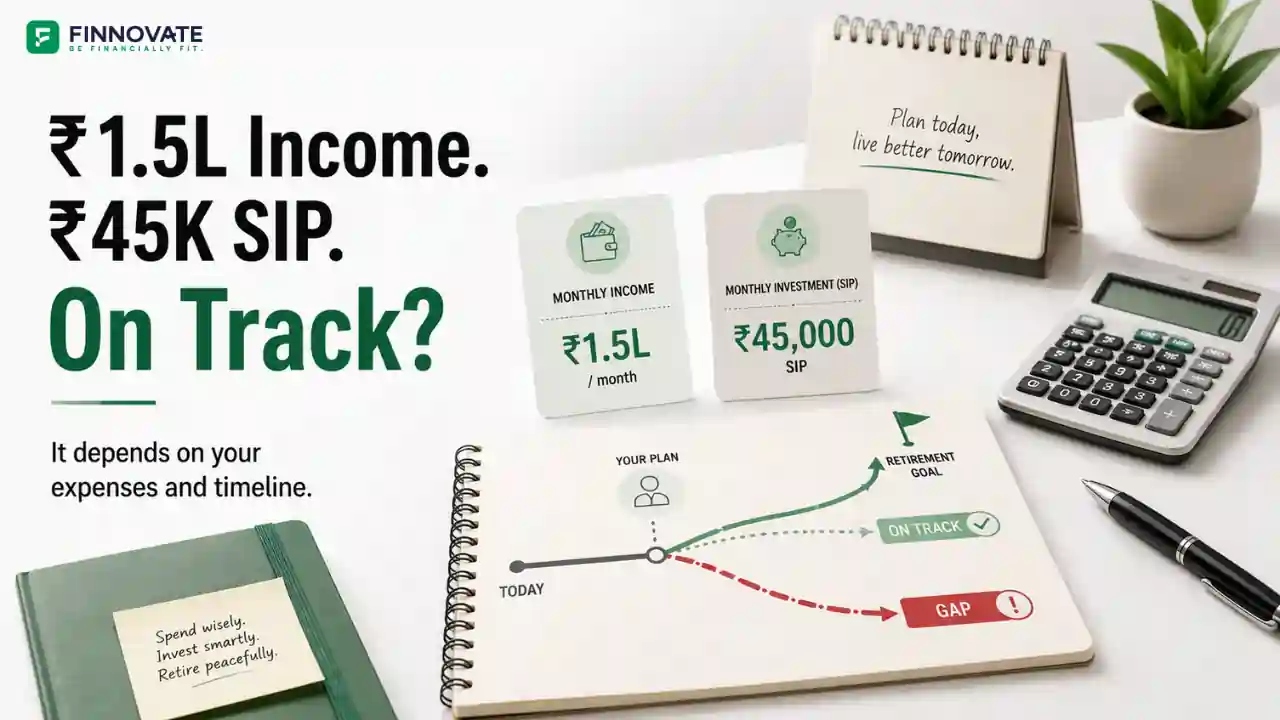

The corpus required depends on monthly expenses, years to retirement, and the withdrawal rate used. At a 4% withdrawal rate and 6% inflation, retiring at 50 with Rs 1 lakh monthly expenses today requires approximately Rs 5.37 crore for someone 10 years away and Rs 7.19 crore for someone 15 years away. At the more conservative 3.5% rate, these rise to Rs 6.14 crore and Rs 8.22 crore respectively. Please consult a SEBI-registered investment adviser to compute the figure for your specific situation.

To retire at 50, a savings rate of 35% to 50% of take-home pay during the accumulation phase is broadly referenced as the required range. Someone starting at 30 with a 40% savings rate has 20 years of compounding working in their favour. Starting at 40 typically requires 50% or higher to reach the same corpus by 50. The timeline compresses but the path remains viable.

The 30x rule states that the retirement corpus should be at least 30 times annual expenses at retirement, adjusted for inflation. It is a conservative adaptation of the US 25x rule, adjusted for India's higher structural inflation, absence of social security for private sector workers, and longer retirement durations. For early retirees targeting a 35-year retirement, a 30x to 33x corpus provides a wider margin of safety.

Sequence of returns risk is the impact of the order in which investment returns arrive during the withdrawal phase. Retiring in a year when equity markets fall significantly and drawing income during that drawdown permanently impairs the corpus compared to retiring in a positive market year with the same long-term average return. A 2 to 3-year liquidity buffer in non-equity instruments protects the equity portfolio from forced redemptions during the early years of retirement.

The three-bucket strategy divides the retirement corpus into a short-term bucket (years 1 to 3, liquid instruments), a medium-term bucket (years 4 to 10, debt and hybrid instruments), and a long-term bucket (years 10 and beyond, equity for growth). The structure ensures monthly income is available regardless of market conditions while the long-term equity bucket compounds through the later decades of a 35-year retirement.

It depends on monthly expenses and retirement duration. At a 4% withdrawal rate, Rs 5 crore is close to the required corpus for someone with Rs 75,000 monthly expenses retiring in 10 years (required: Rs 4.03 crore). For someone with Rs 1 lakh expenses retiring in 15 years, Rs 5 crore falls short of the Rs 7.19 crore required. The answer is always specific to the individual's expense level, timeline, and withdrawal rate.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

Rs 45,000 on Rs 1.5 lakh salary is a 30% savings rate. But is it enough? See corpus built ...

Use this practical framework to check if you’re ready for early retirement in India. Cov...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...