How to Retire at 40 in India: Corpus, FIRE Roadmap and Investment Plan

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

20 June 2026

Imagine waking up one day and knowing you never have to work for money again - unless you want to.

That’s the dream behind the FIRE movement - Financial Independence, Retire Early.

In this guide, we’ll explain what the FIRE number means, how to calculate it in India, and what steps you can take to reach it - all in simple, clear language.

Your FIRE number is the amount of money you need to live comfortably without working.

Once you reach this number, the returns from your investments can cover your yearly expenses, giving you the freedom to retire early or work on your own terms.

It’s based on a very simple formula:

FIRE Number = Annual Expenses × 25

But where does this “25” come from? And how can you use it for your life?

This rule is based on the idea that if you withdraw 4% of your savings each year, your money will last a lifetime - even after inflation and market ups and downs.

It’s called the 4% Rule. Here’s how it works in simple terms:

If your yearly expenses are ₹12,00,000, then 4% of ₹3 Crore = ₹12,00,000.

So if you have ₹3 Crore invested wisely, you can withdraw ₹1L per month - without running out of money.

If you're 30 today and plan to retire at 50, your future expenses will be higher due to inflation. So it’s better to plan based on what your expenses will look like 20 years from now - not just today.

The good news? You don’t need to calculate this manually - the FIRE Calculator with Inflation does it for you.

Now that you’ve got a better grip on your FI (Financial Independence) number, let’s look at what exactly counts as “expenses” in that calculation.

In India, the cost of living varies a lot. Someone in Mumbai may need more than someone in Indore. That’s why your FIRE number is personal.

| City | Monthly Spend (Example) | FIRE Number |

|---|---|---|

| Mumbai | ₹1,20,000 | ₹3.6 Cr |

| Bangalore | ₹90,000 | ₹2.7 Cr |

| Ahmedabad | ₹70,000 | ₹2.1 Cr |

| Kochi | ₹60,000 | ₹1.8 Cr |

Now that you know how to calculate your FIRE number, let’s make sure you’re calculating it correctly.

Your FIRE number depends entirely on your monthly expenses - but most people forget to include key items. If your estimate is too low, you may run out of money later. If it’s too high, you might delay your goals unnecessarily.

Let’s keep it real and practical.

These are the must-haves in any financial plan. You’ll continue to need them whether you're working or retired.

Even if you're planning a minimalist lifestyle, it's better to add a margin for these - especially if you want your retirement to be enjoyable.

Two common mistakes:

A good thumb rule is to add 10–15% buffer to your estimated expenses for unexpected costs and inflation.

To make this practical:

Don’t just guess - be intentional. This number is the foundation of your FIRE plan.

Next, let’s understand how much you need to save - and how smart investing turns this monthly expense into a solid financial future.

So now you know:

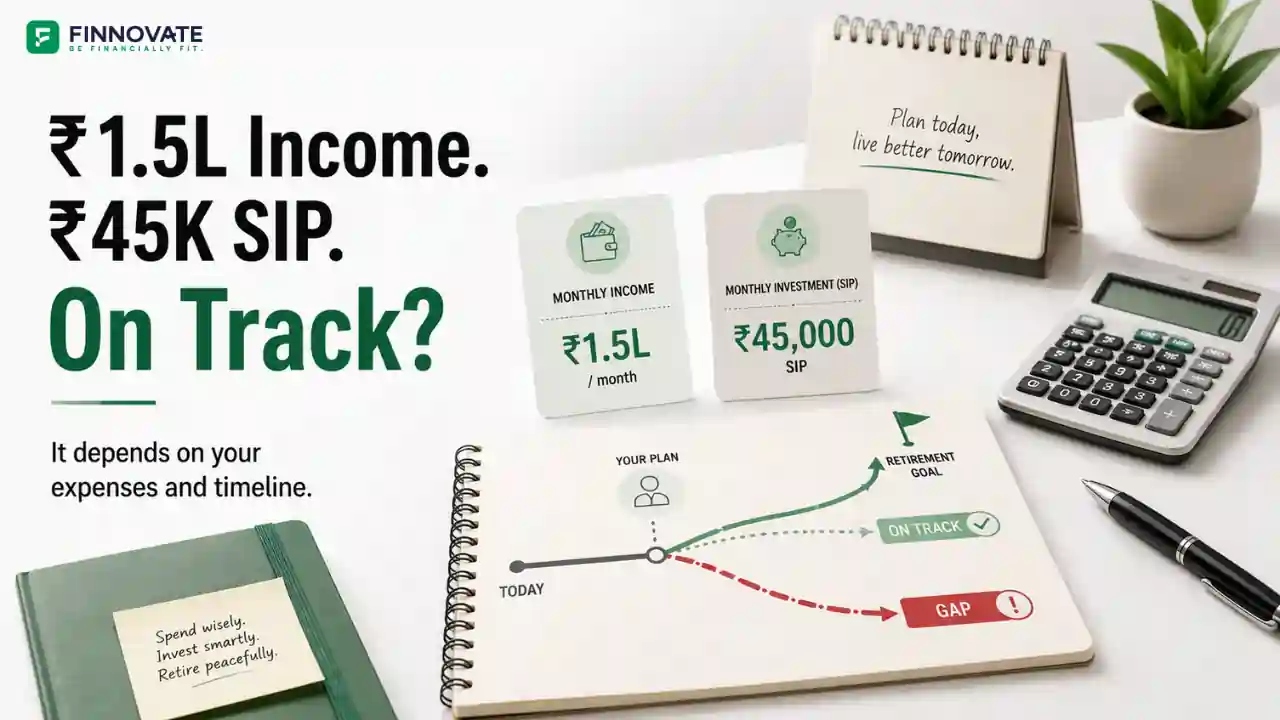

But here comes the most common question: “How much should I actually save every month to reach that number?”

Let’s break it down clearly.

Most people overestimate what they need to start with.

The truth is, small amounts grow big over time - if you stay consistent.

Here's a simple example assuming 12% annual return (which is a common long-term expectation from equity mutual funds):

| Monthly SIP | Years | Returns @12% | Final Corpus |

|---|---|---|---|

| ₹10,000 | 20 | ₹9.8L | ₹9.9L |

| ₹30,000 | 20 | ₹29.4L | ₹3 Cr |

| ₹50,000 | 15 | ₹16.5L | ₹2 Cr |

As you can see, you don’t need to save crores to build crores. You need to start, stay consistent, and stay invested. Use this SIP Calculator to plan on your future investment earnings

A step-up SIP means you increase your SIP amount every year - just like your salary grows.

For example:

This small habit can help you reach your FIRE goal 3–5 years faster, without feeling a major pinch on your lifestyle.

Here’s what happens when you stay invested and increase SIPs:

Compounding rewards the consistent - not just the rich.

Once you know how much to save, the final part is choosing the right investment options - and sticking to them with discipline.

Let’s look at how to build that FIRE strategy in action.

Knowing your FIRE number is just the beginning - the real goal is reaching it. That’s where expert guidance makes all the difference.

At Finnovate, our SEBI-registered financial advisors help you turn your FIRE number into a practical, goal-oriented investment strategy. We look at your inputs, lifestyle, and timeline to build a plan that works - and walk with you to make sure you stay on track.

Get a FREE 30-minute FIRE Consultation Call

Understand exactly what steps to take, what to invest in, and how to stay consistent toward early retirement.

Yes - many professionals are achieving it with consistent savings.

You may need to save more or retire a bit later - but it’s still doable.

No. FIRE is about freedom, not rules.

Your FIRE number is your financial finish line. Knowing it gives you control and clarity.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Retiring at 40 in India requires 30 to 40 times inflation-adjusted annual expenses - not j...

FIRE planning for IT professionals in India: corpus table for retiring at 45 vs 50, ESOP a...

Most families at 55 think their retirement plan is on track. A pre-retirement audit almost...

Rs 45,000 on Rs 1.5 lakh salary is a 30% savings rate. But is it enough? See corpus built ...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...