Equity Fund AUM June 2026: Price Moves Did More Work Than Flows

Active equity fund AUM rose 3.3% to ₹37.34 lakh crore in June 2026. Price accretion of �...

15 July 2026

Quick answer

Most SIPs underdeliver not because of bad markets or bad funds but because of four structural mismatches: the wrong fund category for the goal timeline, a flat SIP amount that never grew with income, exits during market corrections that eliminated the rupee cost averaging benefit, and no specific goal attached to the investment. Any one of these is enough to explain a disappointing corpus. This article explains each one and provides a 5-question audit to identify which applies to your portfolio.

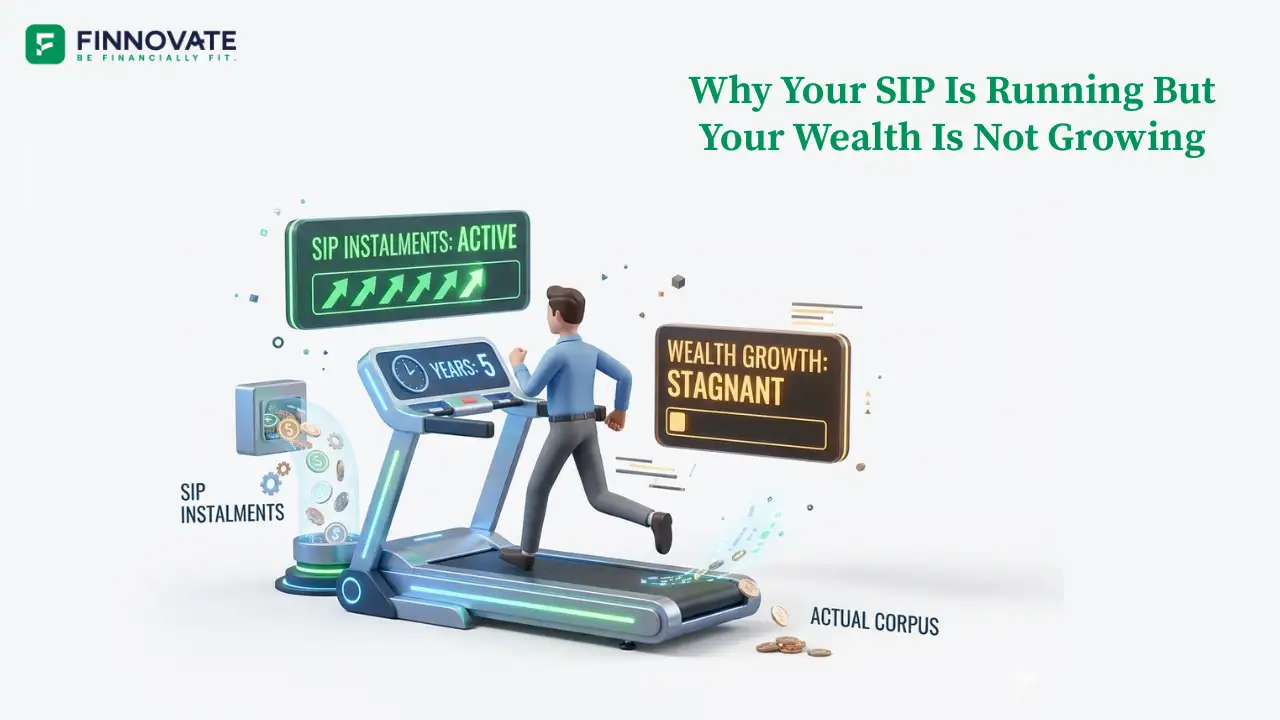

You open your investment app to check the portfolio. The SIP has been running without fail. Not a single missed instalment in five years. The amount is decent. The discipline has been real.

But the number on the screen does not feel like five years of discipline. It looks like barely more than what you put in. Maybe a little more. Not the wealth you imagined when you started.

The SIP did not fail. But something is not working. And in most cases, it is not the market.

A Systematic Investment Plan is a delivery mechanism. It moves a fixed amount of money from a bank account into a mutual fund on a set date every month. It does this reliably, automatically, without requiring any decision from the investor after setup.

What it delivers depends entirely on what it is delivering into, how much, and for how long. The mechanics are not the issue. The configuration almost always is.

The four reasons that follow account for most of that gap.

The most common foundational error in SIP investing is running an equity SIP toward a goal that is 2 to 3 years away.

Equity mutual funds are designed for long horizons. Over 7 to 10 years, they have historically compensated investors for the volatility they carry. Over 2 to 3 years, that same volatility can produce low or negative XIRR even when the fund is well-managed and the investor has done nothing wrong.

The XIRR on a 3-year equity SIP tends to be underwhelming in flat or declining markets. Not because the fund failed, but because most of the capital has had almost no time to compound. The earliest instalments have been growing for 3 years. The most recent have been growing for 30 days. The mathematical average of that range is rarely impressive in the early years.

The category mismatch explains more disappointing SIP experiences than poor fund selection ever will.

| Goal Timeline | Right Category | Wrong Category |

|---|---|---|

| Under 2 years | Liquid or ultra-short duration debt | Equity, hybrid |

| 2 to 4 years | Short-duration debt or conservative hybrid | Mid-cap, small-cap |

| 4 to 6 years | Aggressive hybrid or balanced advantage | Sectoral, thematic |

| 7 years and above | Flexi-cap, large-cap, or mid-cap index | Debt funds alone |

The investor running a 3-year equity SIP toward a house down payment is not making a bad fund choice. They are using the right vehicle on the wrong road. The correction is not to find a better equity fund. It is to match the category to the timeline. For a deeper look at how active and passive categories differ within each tier, see the Finnovate explainer on active vs passive portfolio management.

A flat SIP amount in a rising-income household is a shrinking SIP in real terms. If a professional set up a Rs 10,000 per month SIP five years ago and never revised it, that Rs 10,000 now represents a smaller share of income, a smaller share of financial capacity, and a smaller share of what the goal now costs. Income grew. The goal inflated. The SIP stayed the same.

| Scenario | Starting SIP | 20-year corpus at 12% | Total invested |

|---|---|---|---|

| Flat SIP | Rs 10,000/month | Rs 1.00 crore | Rs 24 lakh |

| 10% annual step-up | Rs 10,000/month | Rs 1.99 crore | Rs 68 lakh |

| Difference | Rs 99 lakh more | Rs 44 lakh additional |

The step-up investor puts in Rs 44 lakh more over 20 years and gets Rs 99 lakh more in return. The return on the additional investment itself compounds, producing more than double the incremental contribution in final corpus value.

There is a second dimension. A Rs 1 crore corpus accumulated over 20 years is worth approximately Rs 31 lakh in today's purchasing power at 6% annual inflation. A SIP sized for a Rs 1 crore target two decades ago is structurally underpowered for what that amount will actually mean when the goal arrives.

Each April, at the start of the financial year, is the natural moment to increase the SIP amount. Even a 5 to 10% annual increase changes the outcome materially over a long horizon. For an investor whose salary has grown but whose SIP has not, the gap between what was planned and what will be available is already significant and widens each year.

The most expensive behavioural mistake in SIP investing. And the most human one.

When a portfolio falls from Rs 18 lakh to Rs 14 lakh in three months, stopping the SIP feels like a rational response. The market is falling. Adding money to a falling position seems counterproductive. The instinct to pause is entirely understandable.

It is also structurally costly, in a specific and quantifiable way.

A fixed monthly SIP amount buys more mutual fund units when the NAV is lower. Those units purchased during a correction are the cheapest the investor will ever buy in that fund. When markets recover, those low-cost units do the most work in the portfolio. An investor who stops during a correction forfeits access to precisely the units that contribute most to the final corpus.

The investor who exits during a correction does not just miss the recovery. They miss the leverage that those correction-phase units provide on the recovery. Resuming the SIP later, at higher NAVs, means the average cost per unit is permanently higher than it would have been.

Research across the mutual fund industry consistently identifies a 4 to 5 percentage point annual gap between the returns a fund earns and the returns its investors actually receive. The entire gap is accounted for by behaviour: buying after strong periods and exiting during corrections. The fund performs. The investor underperforms the fund they are invested in.

An additional consideration: equity mutual fund units held for less than 12 months are subject to short-term capital gains tax at 20%. An investor who exits a falling SIP and re-enters later may also be triggering a tax event on whatever gains existed before the exit. For the full framework on SIP redemption tax implications, see the Finnovate article on mutual fund taxation for FY 2025-26.

A SIP with no attached goal is a savings habit. Savings habits are valuable. But a savings habit is not a financial plan.

Without a target corpus and a target date, three decisions that determine whether a SIP will build meaningful wealth cannot be made correctly.

Whether the amount is sufficient. An investor running Rs 8,000 per month toward "the future" has no way of knowing if Rs 8,000 is enough, because they do not know enough for what. If the actual goal is a Rs 50 lakh retirement contribution in 8 years, Rs 8,000 per month at 12% gets to approximately Rs 16.5 lakh. The investor is 67% short. But without a defined goal, there is no awareness of the shortfall. The SIP continues and the gap is discovered only when it is too late to correct.

Whether the category is appropriate. Category selection depends on the time remaining to the goal. Without a goal date, there is no timeline, and without a timeline, there is no basis for choosing between an equity fund and a debt fund.

When to stop, switch, or redirect. A SIP without a goal runs indefinitely by default. Some investors continue running SIPs toward goals they have already achieved, or goals that no longer exist, because nothing prompted them to stop or redirect the capital.

Goal alignment is the foundational requirement for a SIP to function as a wealth-building tool. Without it, the other three structural problems in this article are almost guaranteed to appear.

This audit takes approximately 20 minutes. It identifies which of the four structural problems applies to a portfolio and how urgently each needs to be addressed.

Does each SIP have a specific goal, a target corpus, and a target date? If the answer is no for any SIP, the amount cannot be verified as correct, the category cannot be confirmed as appropriate, and there is no mechanism to know when the job is done. Start here before any other review.

Is the fund category matched to the remaining time to the goal? Map each fund category to the time remaining until the goal's target date. Equity funds running toward goals under 3 years are misconfigured. Debt funds running toward retirement goals 15 years away are likely generating returns that will not outpace inflation over the full horizon.

Has the SIP amount increased since it was set up? If the SIP has been running for 3 or more years at the same amount and income has grown over that period, the real contribution to the goal has shrunk. A 5 to 10% annual increase is the minimum needed to keep the SIP proportionate to both income and the goal's inflating cost.

Was the SIP paused or stopped at any point during a market correction? If yes, the rupee cost averaging benefit for that period was forfeited. The portfolio's average cost per unit is permanently higher than it would have been. This does not reverse, but it informs the decision not to repeat the same response in the next correction.

What is the XIRR of each SIP, and is it being compared to the right benchmark? XIRR, not the fund's point-to-point return, is the actual personal return. A fund with 14% 5-year returns and an investor XIRR of 8% on the same fund indicates a behavioural gap, not a fund quality problem. Most investment apps display XIRR in the portfolio section. If it is materially below the fund's category average, the audit questions above will identify why.

A well-configured SIP portfolio has three consistent characteristics. None of them require a particular fund or a particular return rate. All of them require intention.

Every SIP has a named goal with a target corpus and a target date. Not "retirement" but "Rs 2.5 crore by age 60." Not "education" but "Rs 40 lakh in 12 years." The specificity is what allows every other decision to be verified against something real.

Every fund category is matched to the time remaining to its goal. The longest-horizon goals sit in equity. The nearest goals sit in debt or conservative hybrid. The category shifts as the timeline shortens, not based on market conditions but based on the goal's remaining window.

The portfolio has an annual review point. Each April, three things are checked: whether the goal's cost has changed, whether the SIP amount needs to increase, and whether any fund has consistently underperformed its benchmark over a full market cycle. The review is the mechanism that keeps a well-structured portfolio current. Without it, a well-configured portfolio in year one becomes a misaligned portfolio in year five as goals inflate, income grows, and market cycles turn.

For investors considering where passive funds fit within this structure, the Finnovate articles on passive fund flows in India and how to build a strategy around passive funds are useful references on category construction within the equity layer.

Not sure which of the four structural problems applies to your SIP portfolio?

Book a Financial Fitness CheckupThe fund's advertised return is point-to-point for one fixed investment date. XIRR is your personal return across all instalment dates and amounts. In the early years, XIRR tends to be lower because most capital has had little time to compound. If it is materially below the fund's category average, behavioural factors or a category mismatch are the most likely explanations. Please consult a SEBI-registered investment adviser for a portfolio-specific assessment.

A commonly used benchmark is 5 to 10% per year, aligned with income growth. This keeps the SIP proportionate to both income and the inflating cost of the goal. A flat SIP in a rising-income household represents a progressively smaller real contribution with each passing year.

A falling market means the same monthly amount buys more units at lower NAVs. Those units do the most work when markets recover. Stopping during a correction forfeits the cheapest units the SIP would ever buy and locks in a permanently higher average cost per unit.

Calculate the target corpus, determine years remaining, and use a SIP return calculator to find the monthly amount needed. If the current amount falls short, increase it or extend the timeline. A SEBI-registered investment adviser can run this across all goals and identify shortfalls.

Each April is the practical cadence for most investors. This aligns with the LTCG exemption reset, full-year fund performance data, and the natural window to increase SIP amounts. Mid-year reviews are worth considering after a significant life event such as a change in income, a new goal, or a major market correction.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice or a recommendation to buy or sell any financial instrument. The step-up vs flat SIP comparison is illustrative at 12% annualised return and is not a return projection. The investor return gap and Nifty bear market data are cited from industry research for illustrative purposes only. Past market behaviour is not indicative of future outcomes. Please consult a SEBI-registered investment adviser before making any investment decision. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Active equity fund AUM rose 3.3% to ₹37.34 lakh crore in June 2026. Price accretion of �...

Passive fund inflows rebounded to ₹16,724 crore in June 2026, with gold and silver ETFs ...

Equity fund folios grew 22.96% CAGR and AUM 29.69% over 3 years. See which of the 11 categ...

Active equity MF inflows fell 40.4% in May 2026 to ₹22,908 crore, but still drove more A...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...