Bancassurance in India FY26: Banks Earn ₹20,000 Crore and the Risks That Come With It

Indian banks earned over ₹20,000 crore distributing insurance in FY26. HDFC Bank led at ...

28 July 2026

We all insure our car, our phone, even our travel plans.

But what about the income that keeps all of it running?

That’s where term insurance comes in - the simplest, purest form of life insurance designed to protect your family if something happens to you. It doesn’t give returns. It gives security - a financial safety net for your loved ones when they need it most.

In simple: Term insurance replaces your income when you’re not around to earn it.

(Also read: Why Insurance Is the Foundation of Financial Planning)

Term insurance is a pure protection plan. It provides a fixed payout - called the sum assured - to your family (nominee) if the insured person passes away during the policy term.

You choose:

If you survive the policy period, nothing is paid out - because it’s not an investment plan, it’s a protection plan.

Example:

If you buy a ₹1 crore term plan for 25 years and pay ₹1,000 per month, your family gets ₹1 crore if something happens to you during that period.

That’s it. No hidden charges, no complicated bonuses - just straightforward financial security.

(Next read: How Much Term Insurance Do You Need?)

Let’s simplify it in four steps:

If you survive the term, the policy ends. You’ve effectively transferred the risk of income loss to the insurer.

Most insurers in India are regulated by IRDAI (Insurance Regulatory and Development Authority of India), ensuring consumer protection and transparent claim processes.

Note:

While choosing a plan, check the Claim Settlement Ratio (CSR) of the insurer. A CSR above 95% means the insurer has honoured most claims.

Whether you’re a doctor, a salaried professional, or a business owner - your income supports more than just your lifestyle. It funds your family’s dreams.

Let’s see a few examples:

"Your income protects your family’s lifestyle - term insurance protects your income."

For professionals, it’s not optional; it’s the foundation of responsible financial planning.

Here’s why term insurance is one of the smartest financial moves:

(Learn more: Family Floater vs Individual Health Insurance)

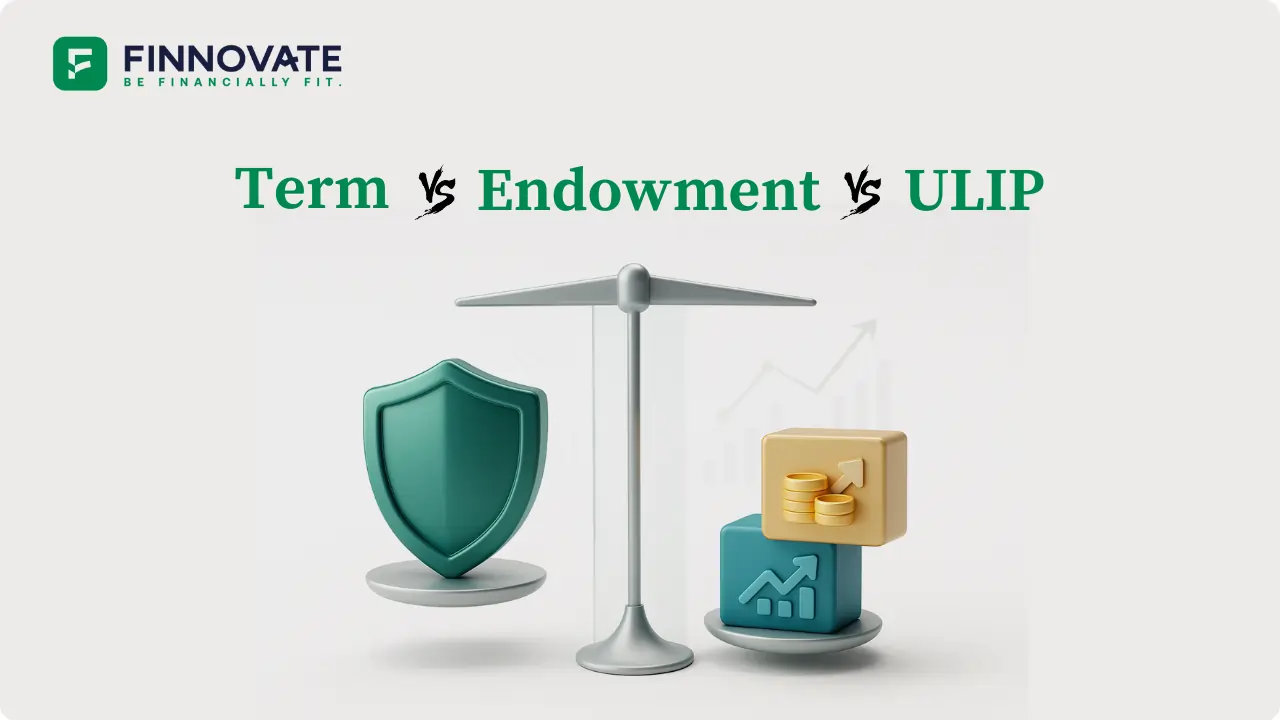

| Feature | Term Insurance | Endowment / ULIP / Money-back Policy |

|---|---|---|

| Purpose | Pure protection | Protection + savings |

| Premium | Low | High |

| Payout | Only on death | Death + maturity |

| Returns | None | Market / guaranteed |

| Transparency | Very high | Moderate |

| Best for | Income replacement | Wealth creation (with limited returns) |

Many people confuse term insurance with other life insurance products that mix savings with protection. The truth is - if you want to invest, use mutual funds or other instruments.

If you want to protect, buy term insurance.

Myth 1: “It’s a waste if I survive.”

Fact: You don’t say health insurance is a waste if you don’t fall ill. Term insurance works the same way - it’s protection, not profit.

Myth 2: “My company’s group insurance is enough.”

Fact: Employer-provided covers are temporary and limited. When you change jobs or retire, that protection ends.

Myth 3: “Term plans are expensive.”

Fact: A 30-year-old can get ₹1 crore cover for under ₹900 per month. That’s cheaper than your OTT subscription.

Myth 4: “Only married people need it.”

Fact: Even single professionals with parents, siblings, or loans need protection against income loss.

Start with a quick self-check, then move to a consult:

It’s a life insurance plan that pays your family a fixed amount (sum assured) if you pass away during the policy term. It’s the cheapest and most effective way to secure your family’s future.

No. Term insurance doesn’t return premiums - because it’s a pure protection plan. If you want refund options, look for “Return of Premium” variants (at a higher cost).

Term insurance is for protection; endowment is for savings. Keep protection and investment separate - that’s smarter financial planning.

Yes, most insurers allow top-up cover or life-stage benefits when you marry, buy a house, or have children.

Yes. All insurers are regulated by IRDAI, and online term plans are secure, cheaper, and paperless.

Disclaimer: This article is for educational purposes only and not a solicitation to buy or sell any insurance product. Finnovate Financial Services Pvt. Ltd. is a SEBI-registered RIA offering unbiased financial planning services.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Indian banks earned over ₹20,000 crore distributing insurance in FY26. HDFC Bank led at ...

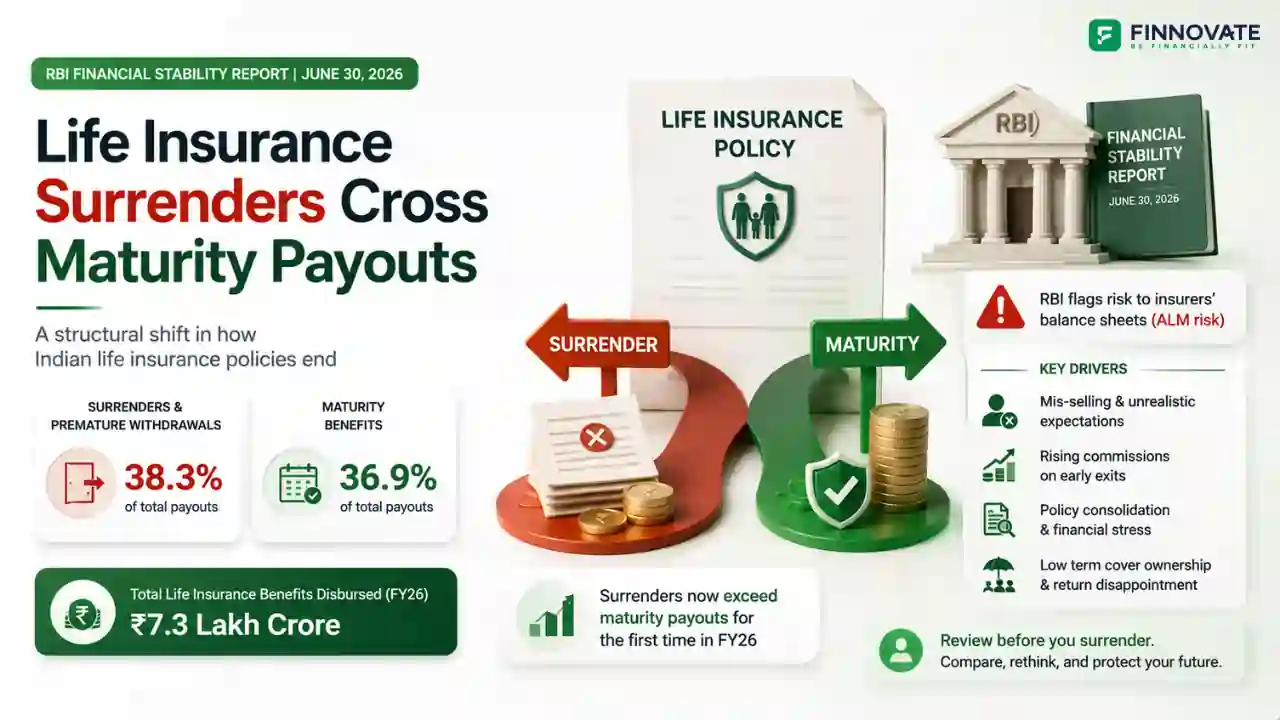

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare Term Insurance, Endowment, and ULIP in a clear, unbiased way. Understand costs, co...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...