How to Choose a Financial Advisor in India: 10-Step Guide

Learn how to choose a financial advisor in India. Verify SEBI registration, fees, experien...

16 July 2026

“Will my money double in 5 years?”

“What’s better - high returns or long-term investing?”

If you've asked these questions, you're not alone. Every investor - beginner or seasoned - wants to know one thing: how fast and how far will my money grow?

Let’s settle the debate with real data, simple logic, and one powerful insight that has built fortunes silently:

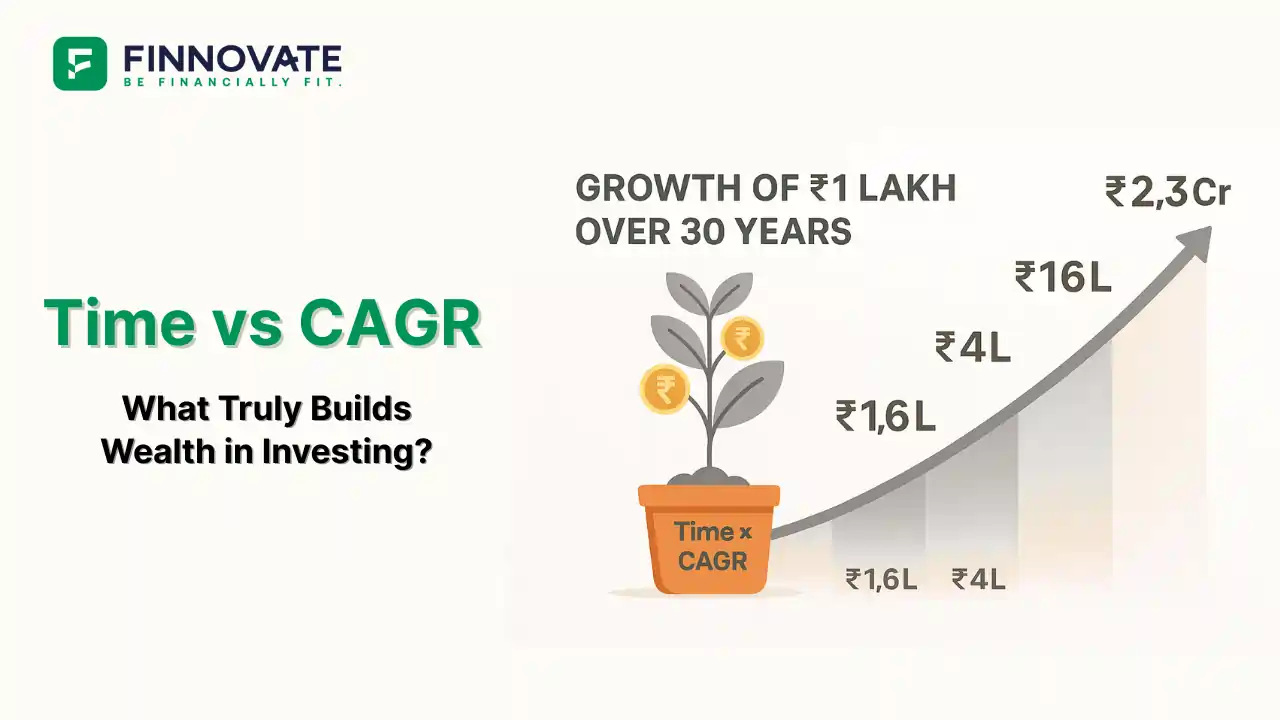

Wealth isn’t just about how much you earn - it’s about how long you stay invested.

We often hear the term CAGR (Compound Annual Growth Rate), which tells you how much your investment grows each year on average. But here's the kicker:

Let’s break this down with numbers.

This table shows the growth of ₹1 lakh if left untouched for 2 to 30 years, assuming different CAGR rates (pre-tax):

| Holding Period | At 5% | At 10% | At 15% | At 20% | At 25% |

|---|---|---|---|---|---|

| 2 Years | ₹1.1L | ₹1.2L | ₹1.3L | ₹1.4L | ₹1.6L |

| 5 Years | ₹1.3L | ₹1.6L | ₹2.0L | ₹2.5L | ₹3.1L |

| 10 Years | ₹1.6L | ₹2.6L | ₹4.0L | ₹6.2L | ₹9.3L |

| 15 Years | ₹2.1L | ₹4.2L | ₹8.1L | ₹15.4L | ₹28.4L |

| 20 Years | ₹2.7L | ₹6.7L | ₹16.4L | ₹38.3L | ₹86.7L |

| 25 Years | ₹3.4L | ₹10.8L | ₹32.9L | ₹95.4L | ₹264.7L |

| 30 Years | ₹4.3L | ₹17.4L | ₹66.2L | ₹237.4L | ₹807.8L |

Source: FundsIndia. Rounded for simplicity. Pre-tax, pre-inflation.

Let’s say you invest ₹1 lakh today.

Now extend the same to 30 years:

That’s not just the effect of a better return - it’s the amplification power of time.

Good point. If inflation averages 6%, your real return at 10% CAGR is just ~4%. And taxes (like 10% LTCG on equity) can eat into gains.

But remember:

So while CAGR matters, time gives it wings.

Q: What matters more - time or returns?

A: Both matter. But time has a larger multiplier effect than small jumps in return.

Q: Can I invest later with higher CAGR and still catch up?

A: Possible, but difficult and riskier. It’s safer to start early and stay invested.

Q: What if I can only invest small amounts?

A: No problem. Compounding works on even ₹5000. Time is your biggest ally.

Get a personalized investment projection. See how small steps today can grow into crores tomorrow. No product pushing - just pure planning.

Disclaimer: The returns shown here are for illustration only. Actual results vary based on market conditions, asset allocation, taxation, and individual behavior. Always consult a registered advisor before investing.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Learn how to choose a financial advisor in India. Verify SEBI registration, fees, experien...

EPF stops. Group health lapses. Advance tax starts. Here's what actually disappears when y...

Goal-based financial planning links every investment to a specific life goal. Learn what i...

No SSY for boys? Here is what works instead. PPF, equity SIPs, NPS Vatsalya and post offic...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...