How to Choose a Financial Advisor in India: 10-Step Guide

Learn how to choose a financial advisor in India. Verify SEBI registration, fees, experien...

16 July 2026

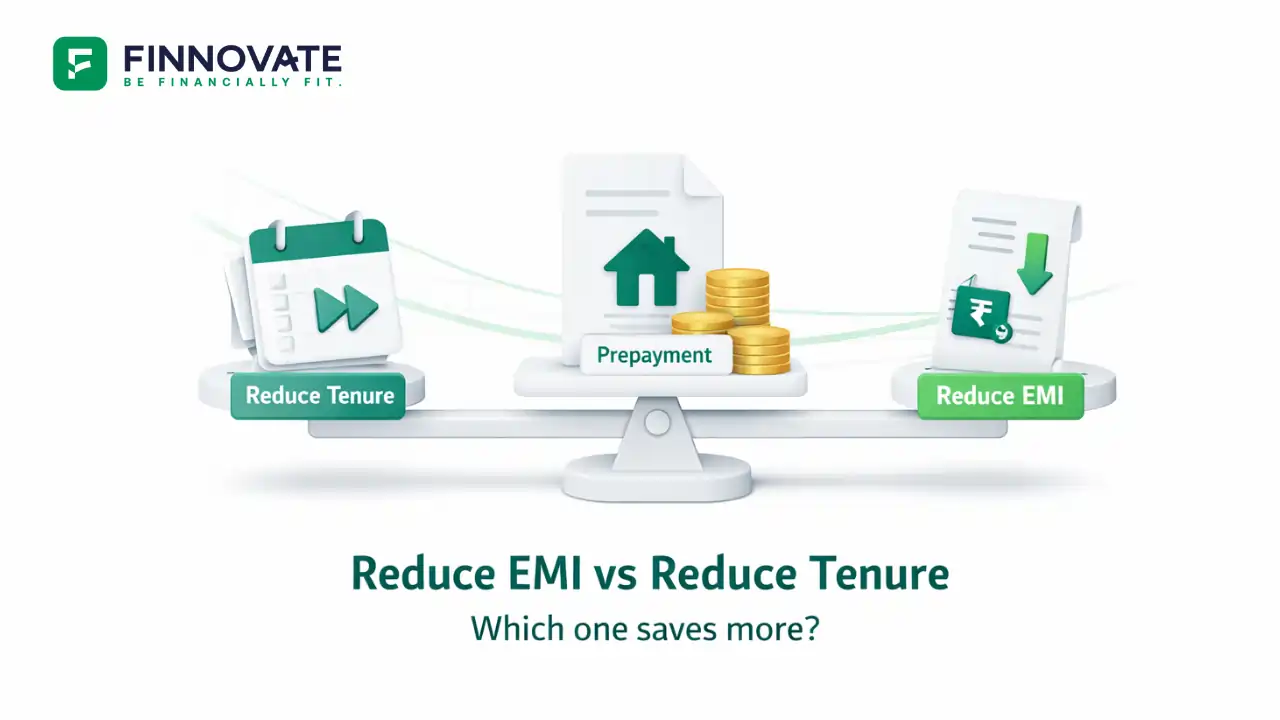

You make a part-prepayment on your loan. The bank gives you a choice.

Option 1: Reduce your EMI.

Option 2: Reduce your tenure.

Both feel like a win. But they don’t work the same way.

If your goal is to pay less total interest, reducing tenure usually helps more. If your goal is to free up monthly cashflow, reducing EMI helps more.

This guide explains the difference in simple terms, shows how the math behaves, and gives you a quick checklist. If you want to run your own numbers, you can use Finnovate’s Loan Prepayment Calculator and EMI Calculator.

Reducing tenure usually saves more total interest.

Because you keep paying the same EMI, you finish the loan earlier, and the lender gets fewer months to charge you interest.

Reducing EMI mainly improves monthly cashflow.

Your monthly burden reduces, but the loan often continues for the same number of years, so interest keeps running longer.

So the real question is not “which is better?”

It’s “what problem am I solving right now?”

In most loans, especially home loans, your early EMIs are mostly interest and less principal.

So when you reduce principal early, you reduce future interest on a larger base. That’s why early prepayments usually have a bigger impact than late ones.

Every month, interest is calculated on your outstanding principal.

So after you prepay, two paths open up:

Both save interest compared to doing nothing, but the first option usually saves more.

Let’s use a clean illustration.

Now you prepay ₹2,00,000 this year.

Your lender gives you two choices.

You continue paying around ₹50,700 per month.

Because you prepaid principal, the loan finishes earlier. That usually means:

This option typically gives the maximum interest saving, because your monthly payment stays strong and more of each EMI starts hitting principal sooner.

Your EMI reduces, maybe to around ₹48,700 (illustrative).

You feel lighter every month, which can genuinely help. But:

So you still save interest, but usually less than tenure reduction.

Many people pick EMI reduction and then spend the EMI savings. That cancels a big part of the long-term benefit.

If you choose EMI reduction, add one rule.

Don’t consume the savings. Redirect it to:

Choose reduce tenure if most of these are true:

Choose reduce EMI if most of these are true:

Think of EMI reduction as “breathing room first.” You can still switch to tenure reduction later.

You don’t have to lock yourself into one choice forever.

If you’re in a tight phase, reduce EMI for 6–12 months.

Use the freed-up cashflow to:

When you’re ready, plug your updated numbers into the Loan Prepayment Calculator and check what the next prepayment can do.

If you want maximum interest saving but feel nervous:

You get faster loan closure, without feeling exposed.

Choose reduce tenure if:

Choose reduce EMI if:

If you feel 50-50:

1. Which saves more interest: reducing tenure or EMI?

In most cases, reducing tenure saves more total interest because you finish the loan faster.

2. Can I switch later?

Yes. You can reduce EMI now and later use prepayments to reduce tenure, or do the reverse.

3. Does part-prepayment always reduce total interest?

Usually yes, because your principal reduces. But the size of benefit depends on timing, rate changes, and how the lender applies it.

4. Is monthly extra payment better or an annual lump sum?

Both can work. Monthly extras build discipline. Lump sums from bonuses can reduce principal sharply. The best choice depends on your cashflow pattern.

5. Should I prepay if I can invest instead?

It depends on your risk tolerance, liquidity needs, and comfort level. Many people prefer a balanced approach rather than an all-or-nothing decision.

Disclaimer: This article is for general educational purposes only. It does not consider your personal financial situation, risk profile, tax status, or specific loan terms. Please review your loan documents and decide based on your own circumstances.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Learn how to choose a financial advisor in India. Verify SEBI registration, fees, experien...

EPF stops. Group health lapses. Advance tax starts. Here's what actually disappears when y...

Goal-based financial planning links every investment to a specific life goal. Learn what i...

No SSY for boys? Here is what works instead. PPF, equity SIPs, NPS Vatsalya and post offic...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...