SIP Stability or Stagnation: What the 2026 AMFI Data Actually Shows

SIP inflows hit a record ₹32,087 crore in March 2026. Yet the stoppage ratio crossed 100...

01 June 2026

Not long ago, SIPs were the default choice for retail investors. They were simple, consistent, and quietly powerful. You invested every month, the market did its ups and downs, and rupee cost averaging did the heavy lifting.

But that behaviour is changing. And not in a good way.

Retail investors are increasingly trying to “time” the market, shifting from SIPs to lumpsum bets, and stopping SIPs at a much higher rate than before. It looks smart in the moment. Over the long run, it usually hurts outcomes.

One clear signal is coming from SIP folio trends. The share of incremental SIP folios as a percentage of overall incremental folios has been falling in recent months.

In simple terms, fewer new folios are SIP-led and more investors are opting for lumpsum investing, hoping to catch market dips and avoid market highs.

This could be a one-off. But the data suggests a broader stagnation. More retail investors want the thrill of timing, even if the probability of doing it right is low.

The more worrying signal is the SIP stoppage ratio.

SIP stoppage ratio is the ratio of total SIPs stopped in a month to the fresh SIPs started in that month.

Historically, this number stayed in a manageable range:

But something changed after the clean-up of inactive SIP folios, completed in April 2025.

Since May 2025, the SIP stoppage ratio has been consistently above 75%, and has averaged above 75% for the last 7 months.

That means the new “normal” is now worse than the pandemic peak. And that is not a great signal for long-term retail wealth creation.

The reason is not complicated. For many investors, SIPs feel boring.

You invest the same amount whether the market is up or down. There is no “move” to make. No thrill. No feeling of control.

So some investors try to improve the SIP model by doing this:

The logic sounds appealing. Indian markets have been in a longer-term bull run, so if you can time tops and bottoms even with “some” precision, you could earn better returns than a plain SIP.

The problem is that this works only in theory. In real life, most people don’t time consistently. They hesitate at bottoms and get confident at peaks. That’s human behaviour.

Trying to time the market is like trying to catch every good moment in a long movie. You may succeed sometimes. But you don’t control the plot.

Market timing only improves results if you can repeatedly buy near bottoms and avoid near tops. That requires skill, speed, and discipline. Most retail investors don’t have all three consistently.

Equity returns are not evenly spread across days or months. A small number of sharp up-moves contribute a large part of long-term returns. If you pause your SIP during volatility, you often miss those recovery bursts.

SIPs are designed for long-term goals. They reduce the need to make repeated decisions and they build discipline. When you start “tweaking” SIPs based on mood and headlines, you may derail the goal itself.

Here’s a simple real-world pattern:

The irony is simple: the months you feel most unsure are often the months where SIP discipline helps the most.

If you want your long-term wealth to grow, the focus should be on persistence, not timing.

Markets will do what they do. Your job is to stay consistent. Timing is a waste of time. Persistence is the edge.

SIP stoppage ratio is the number of SIPs stopped in a month compared to the number of new SIPs started in the same month.

Pausing SIPs during volatility can lead to missed recovery phases and fewer units accumulated at lower prices, which can weaken long-term outcomes.

It can, but only if timing is done consistently and correctly. For most retail investors, the odds of repeating this over years are low.

For long-term goals, staying consistent with SIPs and reviewing the portfolio periodically is usually more effective than reacting to short-term market moves.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

SIP inflows hit a record ₹32,087 crore in March 2026. Yet the stoppage ratio crossed 100...

India's household savings in equities and MFs rose from 2% to 15.2% between FY12 and FY25,...

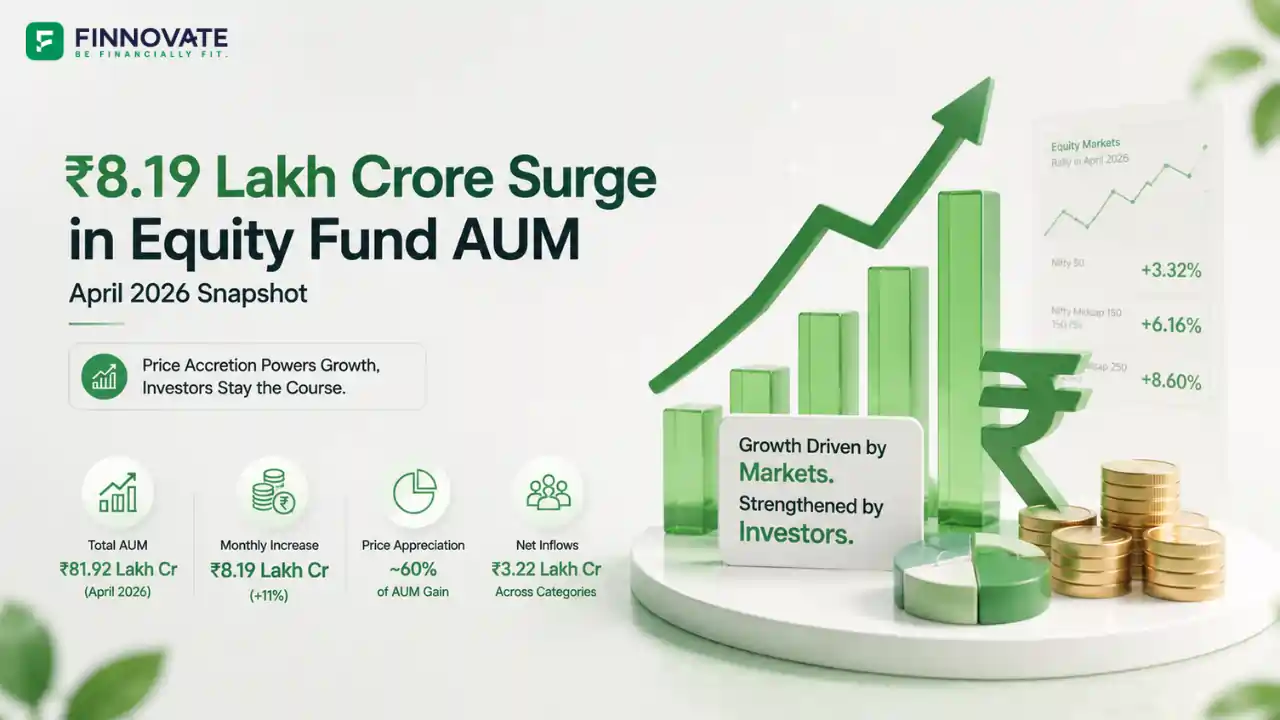

Mutual fund AUM jumped 11% to ₹81.92 lakh crore in April 2026. But 60% of the ₹8.19 la...

Passive fund flows hit Rs 20,082 crore in April 2026, down 33% from March. Equity passive ...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...