Section 143(1) Intimation Explained: Refund, Demand and Next Steps

Received a Section 143(1) intimation? Understand CPC adjustments, refunds, tax demands, re...

24 July 2026

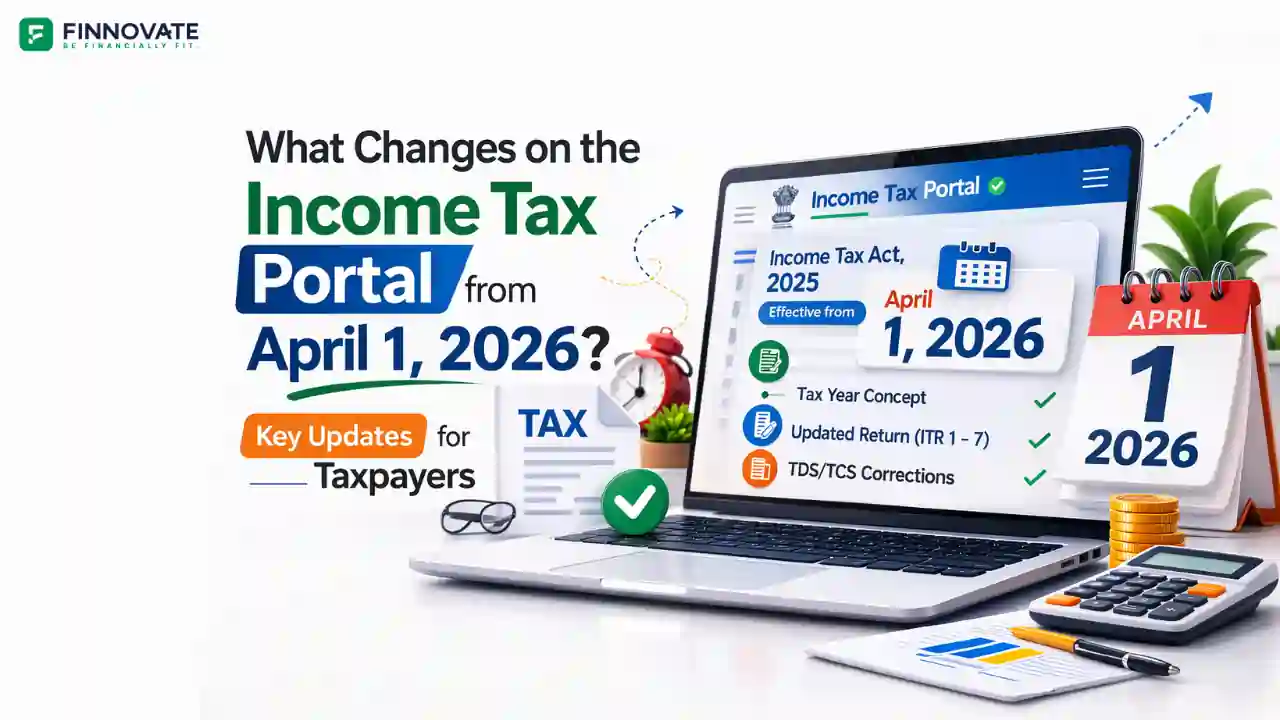

India’s income tax system is entering a new legal framework from April 1, 2026. The official Income Tax portal now states that the Income-tax Act, 1961 stands repealed effective 01.04.2026 under Section 536 of the Income Tax Act, 2025. At the same time, the portal is already carrying important transition updates, including a deadline for older TDS/TCS correction statements and the availability of Updated Return utilities.

This is a major change, but it should be understood correctly. The shift is not mainly about a dramatic visual redesign of the portal. The bigger change is the legal and compliance framework behind it. For taxpayers, salaried employees, professionals, business owners, and deductors, this matters because filing terminology, correction timelines, and the broader tax structure are moving into a new format.

The most important confirmed change is the move to the Income Tax Act, 2025, effective from April 1, 2026. Official PIB material says the new Act simplifies language, removes obsolete provisions, and restructures the law into a more streamlined format.

One of the biggest structural changes is the introduction of the term Tax Year. Under the new law, Tax Year replaces both Assessment Year and Previous Year. This is meant to reduce confusion and make tax reporting easier to understand. Instead of dealing with separate earning-year and assessment-year terminology, taxpayers will now work with a single reference concept.

For portal users, this means that over time, the filing environment, help content, and tax references are expected to align with this simplified structure.

One of the clearest action points already visible on the portal relates to TDS/TCS correction statements.

The official homepage says deductors and collectors should submit correction statements for FY 2018-19 Q4 to FY 2023-24 Q3 by 31.03.2026. It also says that from 01.04.2026, such filings become time-barred because of the repeal of the 1961 Act. The same notice adds that under Section 397(3) of the new Income Tax Act, 2025, corrections are allowed within two years from the end of the relevant tax year.

This is especially important for employers, finance teams, clinics, firms, and businesses that have pending correction work. The practical takeaway is simple: older TDS/TCS mismatches should not be carried forward casually into the new framework.

In many cases, the bigger risk is not lack of awareness. It is delay.

The transition is not only about future law. Some filing tools are already live.

The Income Tax portal’s latest news section says that Excel Utilities for filing Updated Return in ITR-1 to ITR-7 for AY 2025-26 are available now for filing. The homepage also carries a similar update about Updated Return utilities across ITR Forms 1 to 7.

This shows that the portal is already operating with transition-linked updates, not merely announcing them in advance.

For taxpayers, this means the system is already moving in practical terms. It is not only a policy headline anymore.

It is easy to assume that "portal changes" means a redesigned dashboard or a fresh filing interface. That may happen gradually in parts, but the stronger evidence right now points to something deeper.

What is clearly supported by official sources is this:

So the more accurate way to explain the change is this: the portal is moving into a new legal and compliance backbone, and users should expect filing logic, terminology, and process references to gradually reflect that.

The broader direction of reform is simplification. PIB has said that the new tax framework aims to make the law more accessible and less complex. It also said simplified Income Tax Rules and Forms are part of the reform process.

That suggests taxpayers may gradually see cleaner structures, easier references, and more straightforward filing support over time.

At the same time, it is important not to overstate what is final. Some process-related changes are still at the proposal stage. PIB has said that extending the return revision timeline from 31 December to 31 March is proposed, and that filing timelines are to be staggered. Under Finance Bill 2026, the fee for revised returns filed after nine months is confirmed at ₹5,000 for taxpayers with income above ₹5 lakh, and ₹1,000 for those with income at or below ₹5 lakh - this is a specific confirmed figure, not a vague or nominal charge. Until final notified rules and due dates are published, such points should be treated carefully.

For salaried individuals, the portal may continue to feel familiar in daily use. You may still log in, file returns, check refund status, review tax credits, and work through pre-filled information in broadly similar ways.

However, a few things deserve closer attention:

The offline utility and filing manuals also continue to show a strong reliance on pre-filled data and user verification, which means accuracy checks on the taxpayer side will remain important.

For business owners, self-employed professionals, clinics, and employers, the transition is more operational.

If your work involves payroll, vendor deductions, TDS compliance, or correction statements, then the March 31, 2026 correction deadline becomes especially important. Older unresolved deductions or filing mismatches will become permanently impossible to correct once the March 31, 2026 window closes. Under the new Act, these years stand irrevocably time-barred from April 1, 2026 - no correction will be accepted regardless of genuine errors or financial hardship.

This makes the current period a useful time to review deduction records, clean up old errors, and make sure pending correction work is not left to the last minute.

Whenever a major tax transition happens, confusion is common. A few mistakes are especially worth avoiding.

The most important point is to separate what is already confirmed from what is still being rolled out. Right now, the legal shift, the Tax Year concept, the TDS/TCS correction warning, and Updated Return utilities are the clearest confirmed items.

Before April 1, 2026, taxpayers should review whether any older TDS/TCS correction statements are pending, check whether an Updated Return filing is relevant, and stay alert to official updates on the portal.

Those who want to understand the new framework better should also refer to the official support material around the Income Tax Act, 2025 and the Tax Year concept.

The goal is not to overreact. It is to be prepared.

Disclaimer: This article is for general information and educational purposes only. It does not constitute tax, legal, or financial advice. Tax rules, filing processes, and notified forms may change. Please refer to official government sources or consult a qualified tax professional before taking action.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Received a Section 143(1) intimation? Understand CPC adjustments, refunds, tax demands, re...

Zero tax on a ₹14.65 lakh salary is real, but only if your employer contributes EPF on f...

Changed jobs in FY 2025-26? See why combining two Form 16s can create a tax shortfall past...

Compare ESOP vs RSU taxation in India: perquisite tax, capital gains, TDS rules, and the n...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...