SIP Stability or Stagnation: What the 2026 AMFI Data Actually Shows

SIP inflows hit a record ₹32,087 crore in March 2026. Yet the stoppage ratio crossed 100...

01 June 2026

Wealth maximization means growing the value of a business or an individual’s assets over time. In financial terms, it's the process of increasing the net present value (NPV) of future cash flows to maximize long-term shareholder or personal wealth.

In simpler words:

It's not just about earning more - it's about making your wealth grow consistently, sustainably, and in a way that outpaces inflation and taxes.

For businesses, it means focusing on increasing market value, not just accounting profits.

For individuals, it means growing net worth using smart asset allocation, compounding, and disciplined investing.

In the Indian context, wealth maximization is especially important because:

To understand wealth maximization fully, let’s break down the financial logic behind it.

A rupee today is worth more than a rupee tomorrow. That's why wealth-max strategies focus on NPV (Net Present Value).

NPV = Present Value of Future Cash Inflows - Initial Investment

If NPV > 0 → the investment adds to wealth.

EVA = Net Operating Profit After Tax - (Capital Invested × Cost of Capital)

A positive EVA means you're generating returns over your cost of capital.

Real-life example:

If your investment in a mutual fund grows at 12% while inflation is at 6% and your cost of capital is 8%, you are adding real wealth.

| Feature | Profit Maximization | Wealth Maximization |

|---|---|---|

| Focus | Short-term earnings | Long-term value creation |

| Time Horizon | Quarterly/Annual | Multi-year or lifetime |

| Key Metric | Net Profit | Share price / Net Worth / NPV |

| Risk Consideration | Often ignored | Carefully managed |

| Stakeholder Impact | Primarily for owners | For shareholders + investors |

For businesses, wealth maximization = shareholder value.

For individuals, it = growing net worth with smart investing.

Spread investments across:

Leverage compounding. A 10-year delay can reduce your final corpus by 50–60%.

Read: Basics on Mutual Funds & SIPs

Use ELSS, NPS, HUF, and capital gains exemptions to reduce tax drag.

Ensure your wealth is protected via Wills, Trusts, or nomination structures.

HNIs and business owners often use structured debt to create wealth by investing in high-growth assets (AIFs, startups, real estate).

India has a well-regulated ecosystem for wealth management:

| Regulator | Relevance |

|---|---|

| SEBI | Regulates mutual funds, PMS, AIFs, stock brokers |

| RBI | Controls macroeconomic levers affecting rates |

| IRDAI | Regulates insurance products used in wealth protection |

| Income Tax Act | Guides tax-efficient planning under 80C, 80D, 54F, etc. |

Also, fintech-led platforms now offer PMS, mutual funds, and global investing with low friction.

A 35-year-old doctor wants to retire at 55. He invests ₹50,000/month in equity SIPs for 20 years.

He beat inflation, avoided tax drag, and achieved financial freedom.

Now compare this to parking the same money in FDs at 6% post-tax: Final corpus is barely ₹35L.

Wealth maximization is not about chasing returns - it’s about structured, goal-driven, tax-smart investing that builds sustainable prosperity.

Still unsure where to begin? Talk to a SEBI-registered planner or take our free FinnFit test to get a roadmap.

Q. Is wealth maximization only for the rich?

A. No. Even a ₹2,000 SIP over 25 years creates significant wealth.

Q. Can mutual funds alone help me maximize wealth?

A. Yes, if used with proper asset allocation and long-term mindset.

Q. How do I measure if I’m actually maximizing wealth?

A. Track XIRR, NPV of investments, and net worth over time.

Disclaimer: This article is for informational purposes only and does not constitute investment, tax, or legal advice. Please consult a SEBI-registered financial advisor before making any investment decisions.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

SIP inflows hit a record ₹32,087 crore in March 2026. Yet the stoppage ratio crossed 100...

India's household savings in equities and MFs rose from 2% to 15.2% between FY12 and FY25,...

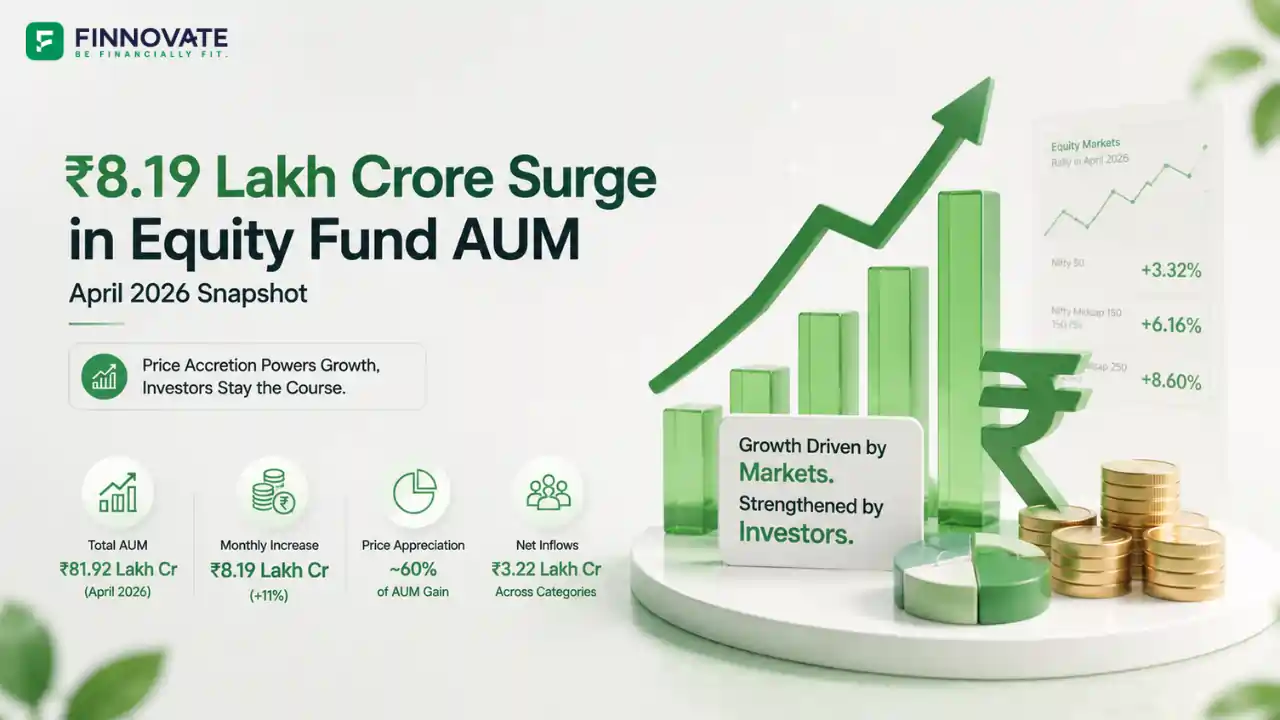

Mutual fund AUM jumped 11% to ₹81.92 lakh crore in April 2026. But 60% of the ₹8.19 la...

Passive fund flows hit Rs 20,082 crore in April 2026, down 33% from March. Equity passive ...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...