NPS for Government Employees: Contribution, Tax and Withdrawal Rules

Understand NPS for government employees, including Central Government contributions, tax b...

04 August 2026

If you are in your 40s and still asking "have I done enough for retirement?" you are not alone. In India, most people delay retirement planning until their 40s because of career priorities, family responsibilities, or lack of awareness.

The good news is that even without the early compounding years, you still have 15 to 20 strong earning years ahead. With the right strategy, it is possible to build a solid retirement corpus. This guide covers how late-start retirement planning in India can still secure your financial independence.

Starting retirement planning in your 40s: the essentials

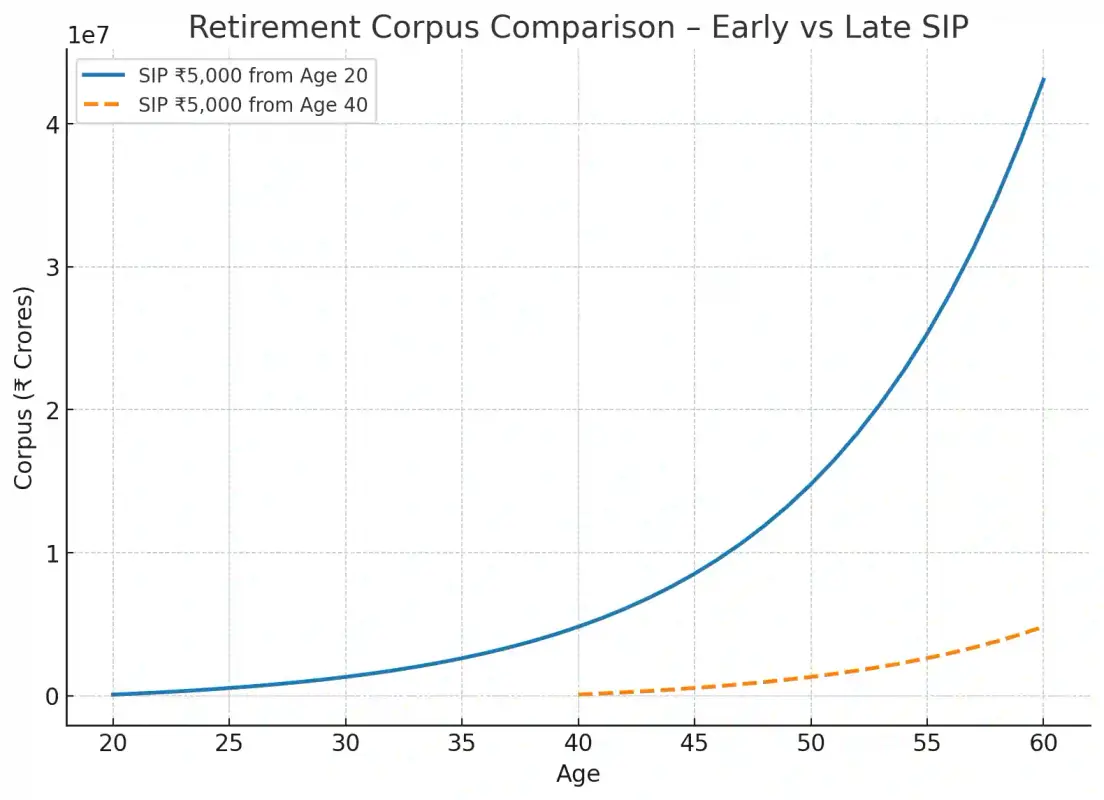

Early starters get the compounding advantage. The gap between starting at 20 versus starting at 40, even with the same monthly SIP amount, is striking:

Doubling the SIP to Rs 10,000/month at age 40 gives approximately Rs 87.4 lakh over 20 years. To reach the same Rs 4.34 crore corpus starting at 40, you would need approximately Rs 50,000/month for 20 years.

Figures based on 11% CAGR, monthly compounding. Past performance is not indicative of future returns. These are illustrative projections only.

Key lesson: Time is the most powerful variable in wealth creation. Late starters can still build a meaningful corpus, but it requires a materially higher savings rate and a clear plan.

When starting at 40, balancing realistic goals with an aggressive savings rate becomes critical.

Focus on inflation-adjusted targets. Rs 1 crore today will have the purchasing power of approximately Rs 32 lakh in 20 years at 6% inflation.

Use conservative return assumptions. A range of 10 to 12% CAGR for equity-heavy portfolios is a reasonable planning figure, not a guaranteed outcome.

Is X crore enough to retire in India at 40? A widely used FIRE framework suggests a corpus of approximately 25 to 33 times your annual expenses (the 3% to 4% withdrawal rate rule). For annual expenses of Rs 12 lakh, this implies a corpus range of Rs 3 crore to Rs 4 crore. However, for a 40-year-old with a potential 45-plus year retirement horizon, many financial planners apply a more conservative 3% to 3.5% withdrawal rate, implying Rs 3.4 crore to Rs 4 crore for the same expenses. Healthcare inflation and sequence-of-returns risk over a longer horizon make a larger buffer prudent. Please consult a SEBI-registered investment adviser to determine the right target for your situation.

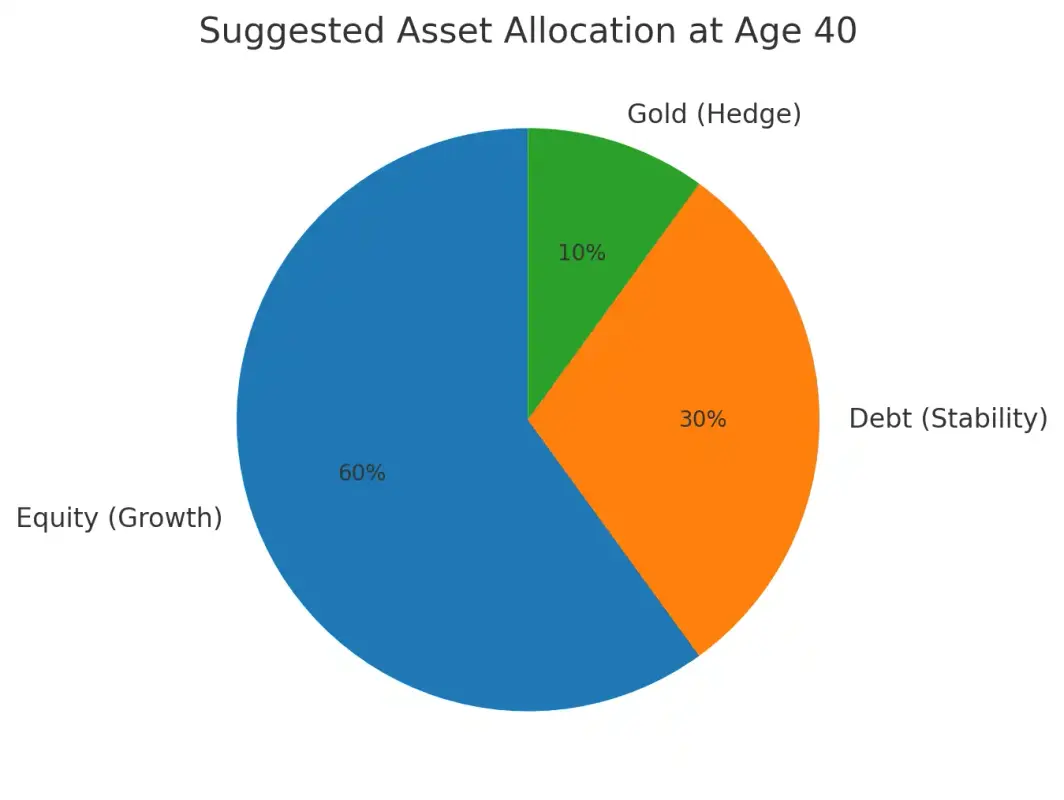

At 40, the portfolio needs to balance growth with stability. A broad allocation framework that is commonly discussed for this life stage:

| Asset class | Suggested allocation | Instruments | Role in portfolio |

|---|---|---|---|

| Equity | 55 to 60% | Index funds, flexi-cap funds | Long-term growth, inflation-beating returns |

| Debt | 25 to 30% | EPF, PPF, NPS Tier-1, debt funds | Stability, capital protection, regular income |

| Gold | 10% | Sovereign Gold Bonds, Gold ETFs | Inflation hedge, portfolio diversification |

| Real estate / REITs | Optional | REITs, rental property | Secondary income, inflation-linked returns |

Example allocation at age 40: 60% Equity | 30% Debt | 10% Gold. See the asset allocation guide for a deeper framework.

High-interest loans materially reduce the money available for compounding.

Example: Redirecting a Rs 25,000 monthly EMI into a SIP at 11% CAGR for 20 years could build approximately Rs 2.18 crore.

A retirement plan built without adequate protection can unravel quickly.

Post-tax return is what matters in the long run, not the headline gross return.

With 15 to 20 years left, errors in planning, asset allocation, or product selection can have large compounding consequences.

Early retirement at 50 is possible, but it demands a high savings rate and a deliberate plan from the day you decide.

This trajectory is realistic only for high-income earners with disciplined, low-lifestyle-inflation habits. Please use the FIRE Calculator to model your specific scenario.

Starting at 40 or even 45 is not ideal, but it is far from hopeless. The same principles apply whether you are 40 or 45: higher savings rate, equity-led portfolio, clear corpus target, and a disciplined plan. The key difference from a 25-year-old is that there is less room for course correction, which makes getting the strategy right earlier more valuable.

With discipline over the next 15 to 20 years, financial independence at retirement remains a realistic outcome.

Want to know how much you need to invest monthly?

Use the Retirement Calculator or schedule a free call with a Finnovate adviser to build a plan around your specific numbers.

It requires a savings rate of 50 to 60% of income and an equity-heavy portfolio for most income levels. For most people, retiring at 60 with a 20-year investment runway is a more achievable target. Use the FIRE Calculator to model your specific scenario.

At 11% CAGR over 20 years, reaching Rs 5 crore requires approximately Rs 57,000/month and Rs 6 crore requires approximately Rs 69,000/month. These are illustrative projections. Actual outcomes depend on the funds chosen, market performance, and consistency of investment. Please consult a SEBI-registered investment adviser for personalised planning.

NPS offers a mix of equity and debt, an additional Rs 50,000 tax deduction under Section 80CCD(1B), and structured long-term accumulation. It is a reasonable component of a retirement portfolio, particularly for the debt and tax-efficiency layer. It works best as part of a broader plan rather than as the sole retirement instrument.

For a middle-class lifestyle in a metro city, Rs 5 to 6 crore by age 60 is a commonly cited planning range, accounting for inflation and healthcare. For early retirement at 40 with a 45-plus year horizon, the corpus requirement is meaningfully higher and should be modelled against your specific annual expenses and withdrawal rate assumption.

SIP brings discipline and rupee-cost averaging across market cycles. A lumpsum, when available (from a bonus, property sale, or inheritance), can accelerate catch-up if deployed into a diversified portfolio promptly. Both approaches are valid and many investors use both simultaneously.

A commonly cited benchmark is approximately 2 to 3 times your annual income in savings or investments by age 40. This is a starting reference, not a precise rule. The right figure depends on your target retirement age, expected expenses, and existing financial obligations. Use the Finnovate Retirement Calculator for a personalised estimate.

Disclaimer: This article is for educational purposes only. SIP corpus projections use assumed 11% CAGR and monthly compounding and are illustrative only. Actual returns will vary. Investments are subject to market risks. Past performance is not indicative of future returns. Please consult a SEBI-registered investment adviser before making any investment or financial planning decision.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Understand NPS for government employees, including Central Government contributions, tax b...

Compare NPS Tier 1 vs Tier 2 on withdrawals, tax benefits, contributions, equity limits an...

Understand NPS withdrawal rules 2026 for normal exit, premature withdrawal, partial withdr...

Two retirees, same corpus, same returns, same withdrawals - yet very different outcomes. S...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...