Category III AIF in India: Strategies, Tax and PMS Comparison

Pitched a Category III AIF when you already have a PMS? Read the post-tax comparison befor...

05 May 2026

Updated: May 2026 | For HNIs, NRIs and Professionals

An Alternative Investment Fund, or AIF, is not just a bigger mutual fund. It works differently, locks your money differently, charges differently, and carries risks many first-time investors do not expect.

India's AIF industry has grown rapidly. As of December 2025, total AIF commitments stood at around Rs 15.74 lakh crore, with more than 1,700 SEBI-registered AIFs in the country. For high-income investors, business owners, doctors, NRIs, and professionals who want exposure beyond mutual funds, PMS, fixed deposits, and listed equity, AIFs can open access to private equity, private credit, venture capital, real estate, infrastructure, and complex market strategies.

But AIFs are not suitable for every investor. They usually require a minimum commitment of Rs 1 crore, may lock capital for several years, charge higher fees, and may involve lower liquidity and higher risk than traditional products.

This guide is for you if: you have been pitched an AIF, are comparing AIF vs PMS vs mutual funds, want to understand Category I, II and III AIFs, or want to know what to check before committing Rs 1 crore or more.

An Alternative Investment Fund is a privately pooled investment vehicle registered with SEBI. It collects money from sophisticated investors and invests that money according to a defined investment strategy.

In simple terms, an AIF pools capital from a smaller group of high-net-worth investors and deploys it into opportunities that are usually not available through normal mutual funds. These may include private equity, venture capital, structured credit, real estate, infrastructure, distressed debt, pre-IPO opportunities, or hedge-style listed market strategies.

Private equity, venture capital, real estate, private credit, distressed assets, infrastructure, derivatives, and listed equity using complex strategies.

AIFs are not mass-market investment products. They raise money through private placement and usually require a minimum commitment of Rs 1 crore.

This is one of the most important parts for first-time AIF investors. Investing in an AIF is not like buying mutual fund units in one click. Many AIFs work on a commitment and drawdown model.

AIFs are not meant for every investor. They may be suitable only when your core financial base is already strong.

Simple test: If locking Rs 1 crore for several years can disturb your family goals, children's education, retirement, business liquidity, or emergency needs, an AIF may not be the right first step.

Before selecting an AIF, it is important to understand how it differs from mutual funds and portfolio management services.

| Feature | AIF | Mutual Fund | PMS |

|---|---|---|---|

| Minimum investment | Usually Rs 1 crore | Often starts from Rs 500 | Rs 50 lakh |

| Investor type | HNIs, institutions, sophisticated investors | Retail and HNI investors | HNIs |

| Asset access | Private equity, private credit, real estate, complex strategies | Mainly listed securities | Mainly listed securities |

| Liquidity | Low in many structures | High for open-ended funds | Moderate |

| Ownership model | Pooled fund units | Pooled fund units | Securities held in investor's demat account |

| Transparency | Periodic reporting | Public factsheets and NAV | Portfolio-level visibility |

| Fees | Higher; management fee plus carry | Expense ratio | Management fee and/or performance fee |

| Taxation | Depends on category and income type | Depends on mutual fund type and asset class | Usually investor-level taxation |

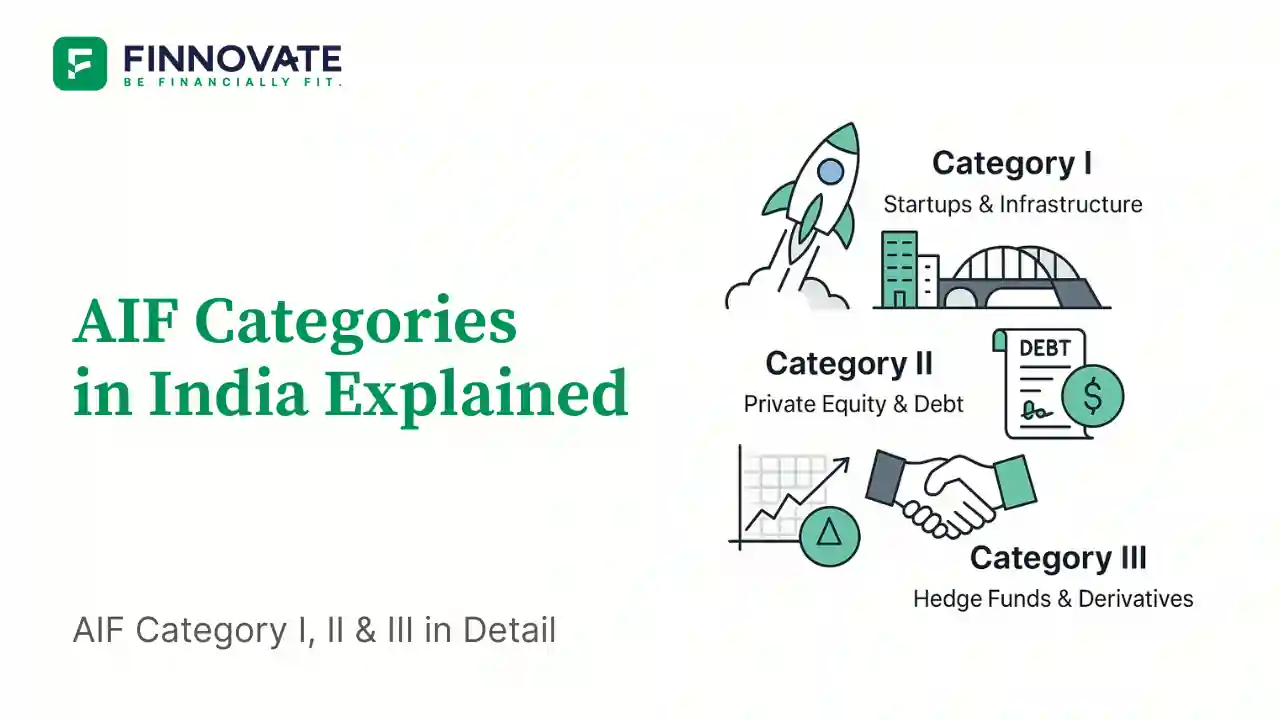

SEBI classifies AIFs into three categories. The category affects the type of strategy, use of leverage, risk level, and tax treatment.

| AIF category | Simple meaning | Common strategies | Typical risk |

|---|---|---|---|

| Category I | Funds investing in sectors considered socially or economically useful | VC, angel funds, SME funds, infrastructure funds, social venture funds | High |

| Category II | Private market and real asset strategies without leverage for investment | Private equity, private credit, real estate, fund of funds | Medium to high |

| Category III | Complex market strategies, often listed-market or derivative-linked | Long-short, arbitrage, PIPE, derivatives, hedge-style funds | High |

Category I AIFs invest in start-ups, early-stage ventures, SMEs, infrastructure, and other sectors considered beneficial to the economy. These funds may receive certain regulatory or policy incentives. Risk can be high because many underlying investments are early-stage or long-gestation.

Category II is the largest AIF category by commitments. It includes private equity funds, private credit funds, real estate funds, debt funds, and funds of funds. These funds do not use leverage for investment, except for permitted temporary borrowing for operational needs.

Category III AIFs may invest in listed equities, derivatives, arbitrage, long-short strategies, or other complex strategies. They may use leverage within permitted limits. These funds can be open-ended or close-ended depending on fund structure.

AIFs are designed for sophisticated investors. The most important entry barrier is the minimum investment commitment.

| Investor type | Minimum commitment | Eligibility note |

|---|---|---|

| Standard investor | Rs 1 crore | Resident Indian, NRI, foreign investor, company, trust or institution, subject to applicable rules |

| Employee or director of AIF / Manager | Rs 25 lakh | Reduced threshold due to professional involvement |

| Accredited investor | May get flexibility depending on structure | Subject to SEBI accreditation criteria and fund terms |

Each AIF scheme generally has a cap on the number of investors, and the fund manager or sponsor must maintain continuing interest as required under SEBI rules. These requirements are meant to align the fund manager's interest with investors.

AIFs usually cost more than mutual funds. The fee structure can significantly reduce the investor's final return, so it must be understood before investing.

| Fee type | Typical range | Meaning |

|---|---|---|

| Management fee | 1% to 2.5% per year | Annual fee paid to the fund manager for managing the fund |

| Performance fee / carry | 15% to 20% of profits above hurdle | Manager's share of returns above the agreed hurdle rate |

| Hurdle rate | Often 8% to 12% | Minimum return investors should receive before carry applies |

| Setup / operating expenses | Varies by fund | Legal, audit, custodian, administration and fund operating costs |

AIF investments are not highly liquid. This is not a small detail. It is one of the most important things to understand before investing.

| Category | Structure | Typical liquidity picture |

|---|---|---|

| Category I | Close-ended | Usually long lock-in, often 5 to 10 years |

| Category II | Close-ended | Usually long lock-in, often 5 to 10 years |

| Category III | Open-ended or close-ended | May offer periodic redemption if open-ended, subject to fund terms |

Capital can remain locked for several years. There may be no easy exit before the fund tenure ends.

If you fail to meet a capital call, penalties may apply. These can include interest, dilution, loss of rights, or other consequences stated in the PPM.

The success of an AIF depends heavily on the fund manager's ability to source, evaluate, manage, and exit investments at the right time.

Some AIFs may hold concentrated exposure across sectors, companies, stages, or strategies. A few poor outcomes can affect overall performance.

High fees and carry can reduce the gap between gross return and investor-level net return. Always review the net return illustration.

Category III AIFs may use leverage within permitted limits. Leverage can increase gains but can also amplify losses during adverse markets.

The Private Placement Memorandum, or PPM, is the most important document to read before investing in an AIF. It explains the fund's strategy, fees, risks, rights, restrictions, tax position, and investor obligations.

Yes, AIFs must be registered with SEBI before operating. SEBI regulation covers registration, fund structure, disclosure, minimum corpus, sponsor commitment, conflict rules, periodic reporting, and investor grievance mechanisms.

But SEBI registration does not mean capital protection. It does not mean guaranteed returns. It does not mean the fund cannot lose money.

Important difference: SEBI regulation improves oversight and disclosure. It does not remove market risk, liquidity risk, execution risk, or the possibility of capital loss.

We review your income, goals, tax bracket, liquidity needs, and investment horizon before discussing any instrument.

Book a ConsultationAn AIF is a privately pooled investment vehicle registered with SEBI. It collects capital from sophisticated investors and invests according to a defined strategy, such as private equity, venture capital, structured credit, real estate, infrastructure or complex market strategies.

For most standard investors, the minimum commitment is Rs 1 crore. Employees or directors of the AIF or its manager may have a lower threshold. Accredited investors may receive flexibility depending on SEBI rules and fund structure.

Not necessarily. AIFs are more flexible and can access alternative assets, but they also have higher minimum investment, lower liquidity, higher fees, and higher complexity. Mutual funds remain more suitable for most retail investors.

In PMS, securities are usually held in the investor's own demat account and the minimum investment is Rs 50 lakh. In an AIF, money is pooled into a fund structure, the minimum is generally Rs 1 crore, and the fund may invest in broader alternative assets depending on category.

Category I includes venture capital, SME, infrastructure and social venture funds. Category II includes private equity, private credit, real estate and fund of funds. Category III includes complex listed market strategies, long-short funds, arbitrage and derivative-based strategies.

Yes. AIFs must be registered with SEBI under the SEBI (Alternative Investment Funds) Regulations, 2012. However, SEBI regulation does not guarantee returns or protect capital.

Yes. AIFs can carry illiquidity risk, manager risk, execution risk, concentration risk, fee drag, leverage risk and tax complexity. They are suitable only for investors who understand these risks. Please consult a SEBI-registered investment adviser before investing.

Tax treatment depends on the AIF category and income type. Category I and II AIFs generally have pass-through treatment for non-business income. Category III AIFs are often taxed at the fund level, depending on structure. See the AIF Taxation Guide for full details.

Yes, NRIs can invest in AIFs subject to applicable FEMA, RBI, KYC, tax and fund documentation requirements. DTAA benefits may apply depending on income type and treaty conditions.

Check the fund category, strategy, manager track record, fees, lock-in, capital call terms, default clauses, tax treatment, liquidity, conflicts of interest and risk factors in the PPM before investing.

Disclaimer: This article is for educational purposes only. It does not constitute investment advice, tax advice, legal advice, a recommendation, or an offer to buy or sell any securities or financial instruments. AIF investments are subject to market risks, illiquidity, and significant lock-in periods. Industry data is based on SEBI AIF statistics and publicly available industry reports. Please read all offer documents carefully and consult a qualified Chartered Accountant and a SEBI-registered investment adviser before making any investment decision.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Pitched a Category III AIF when you already have a PMS? Read the post-tax comparison befor...

SEBI’s March 2026 AIF reporting overhaul introduces an Annual Activity Report and a limi...

Learn how Alternative Investment Funds (AIFs) are taxed in India. A complete guide to Pass...

Learn about the three SEBI-approved AIF categories in India – Category I, II & III. Unde...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...