Category III AIF in India: Strategies, Tax and PMS Comparison

Pitched a Category III AIF when you already have a PMS? Read the post-tax comparison befor...

05 May 2026

Updated: May 2026 | For HNIs, NRIs and Professionals

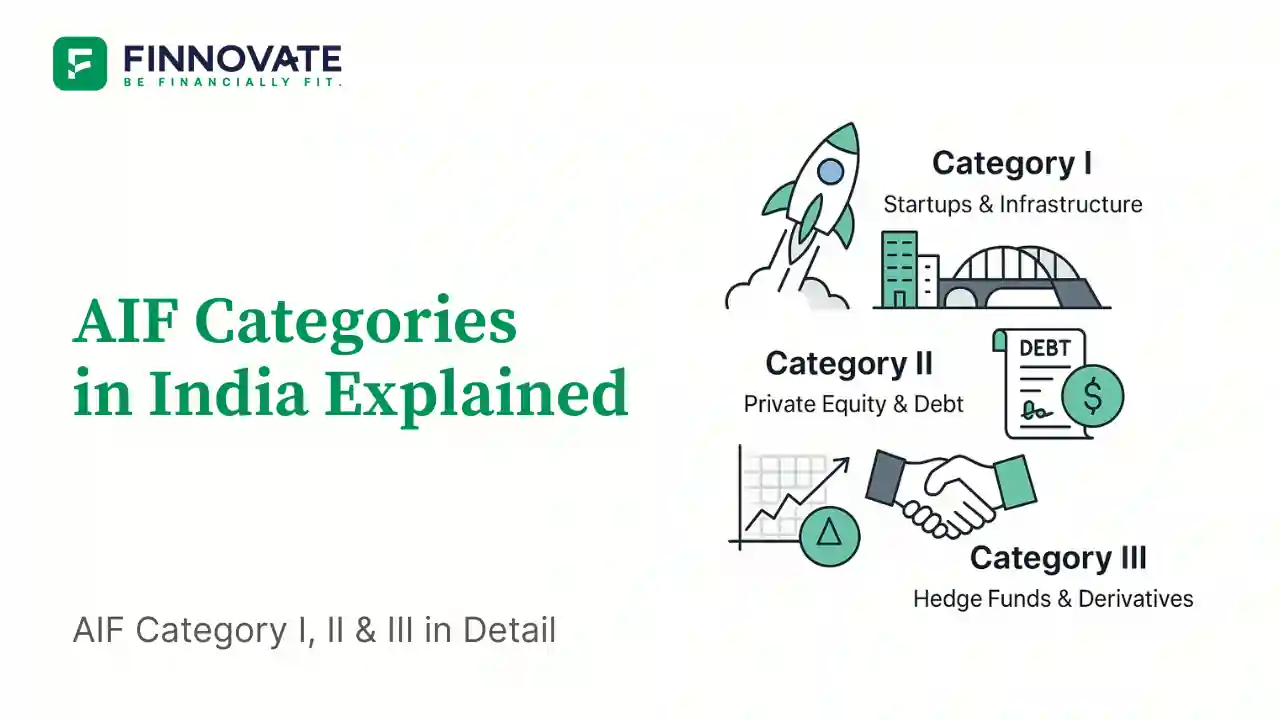

Think of AIF categories as three different lanes, not three versions of the same product. A Category I venture capital fund, a Category II private credit fund and a Category III long-short fund can all be SEBI-registered AIFs, but they work very differently.

SEBI classifies Alternative Investment Funds into three categories. Category I covers venture capital, SME, infrastructure and social venture funds. Category II covers private equity, private credit, real estate and fund of funds. Category III covers complex trading strategies such as long-short equity, arbitrage and derivative-linked funds.

The category decides the investment mandate, risk profile, use of leverage, liquidity structure and tax treatment. So when someone says, “This is an AIF,” your next question should be, “Which category?”

AIFs are not one single product class. The SEBI category determines what the fund can invest in, whether it can use leverage, whether it is usually open-ended or close-ended, how long money may remain locked, and how income may be taxed.

For example, a Category II private equity fund may lock capital for 7 to 10 years and offer pass-through taxation for non-business income. A Category III long-short fund may allow periodic redemption if it is open-ended, but it may be taxed at the fund level depending on the fund structure.

Permitted assets, leverage, tax treatment, open-ended or close-ended structure and regulatory incentives all flow from the AIF category.

Within the same category, two funds can have very different managers, fees, risk controls, portfolio quality and outcomes.

If you are new to AIFs and want the basics first, read the AIF Beginner's Guide.

Category I AIFs invest in sectors that SEBI considers socially or economically beneficial for India. These funds usually direct capital toward early-stage businesses, SMEs, infrastructure and social enterprises.

Invest in early-stage, unlisted start-ups and high-growth ventures. Many companies may fail, but a few winners can drive the overall fund return.

Invest in very early-stage start-ups. These are usually riskier than later-stage venture funds because the businesses are still proving their model.

Invest in small and medium enterprises that need growth capital but are not yet large or listed companies.

Invest in infrastructure projects such as roads, power, logistics or related assets. These may have long gestation periods.

Invest in organisations that aim to solve social problems while also generating financial returns.

| Parameter | Category I |

|---|---|

| Structure | Close-ended; minimum 3-year tenure |

| Typical actual tenure | Often 7 to 12 years, depending on strategy and exits |

| Leverage | Not permitted for investment; operational borrowing only within permitted rules |

| Tax treatment | Pass-through under Section 115UB for non-business income; income is taxed in investor's hands based on its nature |

| Finance Act 2025 update | From AY 2026-27, securities held by Category I AIFs are expressly treated as capital assets |

| Minimum investment | Rs 1 crore for standard investors; lower threshold for eligible employees/directors as per rules |

| Regulatory position | Encouraged category due to start-up, SME, infrastructure and social sector focus |

Category II is the broadest AIF category. It includes private equity, private credit, real estate, debt funds and fund of funds. In practice, this is the main category for HNIs and institutions seeking private market exposure in India.

Invest in unlisted growth-stage or mature companies. Returns depend on business growth, valuation at entry, and exit through IPO, strategic sale or secondary transaction.

Lend to companies through structured debt, mezzanine financing, distressed debt or other credit instruments. Returns may come mainly from interest income and fees.

Invest in residential or commercial real estate projects or assets. Returns depend on developer quality, project stage, sales, rental income and market conditions.

Invest in other AIFs rather than directly in companies or assets. This can spread exposure across managers, strategies and vintages, but may add another fee layer.

| Parameter | Category II |

|---|---|

| Structure | Close-ended; minimum 3-year tenure |

| Typical actual tenure | Often 5 to 10 years depending on strategy |

| Leverage | Not permitted for investment; operational borrowing only within permitted rules |

| Tax treatment | Pass-through under Section 115UB for non-business income; income is taxed in investor's hands based on its nature |

| Finance Act 2025 update | From AY 2026-27, securities held by Category II AIFs are expressly treated as capital assets |

| Minimum investment | Rs 1 crore for standard investors; lower threshold for eligible employees/directors as per rules |

| Regulatory position | No specific sector mandate; broadest category by strategy |

Category III AIFs use complex or diverse trading strategies. These may include listed equity, long-short strategies, arbitrage, derivatives and other market-linked approaches. This category may use leverage within SEBI limits and may be open-ended or close-ended depending on the fund terms.

Invest mainly in listed equities using a stock selection approach. They may look similar to PMS strategies, but the fund structure and taxation can differ.

Take both long and short positions. The goal is to generate returns that may be less dependent on overall market direction, but manager skill becomes very important.

Try to benefit from price differences across related instruments, cash-futures spreads, merger situations or index-related opportunities.

Private Investment in Public Equity. These funds invest in listed companies through negotiated private placements, usually with specific terms and lock-ins.

| Parameter | Category III |

|---|---|

| Structure | Open-ended or close-ended, depending on fund terms |

| Liquidity | Open-ended structures may offer periodic redemption; close-ended funds follow fund terms |

| Leverage | Permitted up to 2x NAV within SEBI limits |

| Tax treatment | No Section 115UB pass-through. In many common trust structures, tax may be paid at fund level, often at Maximum Marginal Rate where applicable. Check the fund tax note. |

| TDS | Not the same as Category I/II pass-through TDS. Check the fund's tax note and distribution statement. |

| Minimum investment | Rs 1 crore for standard investors; lower threshold for eligible employees/directors as per rules |

| Regulatory position | Most flexible category for listed-market and derivative-linked strategies |

Category III vs PMS: Category III and PMS may both invest in listed equities, but they are not the same. PMS securities are usually held in the investor's demat account. Category III is a pooled structure. Taxation, transparency, reporting and liquidity can differ materially.

| Feature | Category I | Category II | Category III |

|---|---|---|---|

| Primary focus | Start-ups, SMEs, infrastructure, social ventures | Private equity, private credit, real estate, fund of funds | Listed equity, long-short, arbitrage, derivatives |

| Structure | Close-ended only | Close-ended only | Open-ended or close-ended |

| Leverage | Not permitted for investment | Not permitted for investment | Permitted up to 2x NAV within SEBI limits |

| Typical tenure | Often 7 to 12 years | Often 5 to 10 years | Varies; open-ended funds may allow periodic redemption |

| Liquidity | Very low | Low | Low to medium depending on structure |

| Tax: non-business income | Pass-through to investor under Section 115UB | Pass-through to investor under Section 115UB | No Section 115UB pass-through; fund-level tax may apply depending on structure |

| Finance Act 2025 | From AY 2026-27, securities treated as capital assets | From AY 2026-27, securities treated as capital assets | No similar pass-through change |

| Risk type | Business survivability risk | Credit, valuation and exit timing risk | Market volatility, strategy and leverage risk |

| Risk level | High | Medium to high | High |

| Minimum investment | Rs 1 crore | Rs 1 crore | Rs 1 crore |

AIF category selection is not about ranking Category I, II and III from best to worst. It is about matching the fund category to the role the allocation should play in your portfolio.

Category I may be relevant if you want exposure to start-ups, SMEs, infrastructure or impact-led sectors. The horizon is usually long and outcomes can be uneven.

Category II is often the starting point for investors looking at private equity, private credit, real estate or fund of funds. Liquidity and tax impact should be checked carefully.

Category III may suit investors who want listed-market strategies beyond traditional mutual funds or PMS. But leverage, taxation and fund-level structure need special attention.

| Investor situation | Category worth exploring | Key consideration |

|---|---|---|

| Wants start-up or venture exposure | Category I | Long horizon and high failure risk |

| Wants private equity or private credit exposure | Category II | Lock-in, income type and tax impact |

| Wants listed-market strategy beyond PMS/MF | Category III | Compare taxation, transparency and liquidity with PMS |

| High-income investor | Category I/II may be more tax-flexible | Income type matters; interest-heavy funds can still be tax-costly |

| NRI investor | All categories, subject to compliance | Check FEMA, DTAA, TRC, Form 10F and TDS process |

Still comparing AIF categories? Review the category, tax treatment, liquidity and risk profile before committing capital. AIFs should fit the plan, not just the return pitch.

We review your income, goals, tax bracket, liquidity needs and investment horizon before discussing any instrument.

Book a ConsultationSEBI classifies AIFs into Category I, Category II and Category III under the SEBI (Alternative Investment Funds) Regulations, 2012. Category I covers venture capital, SME, infrastructure and social venture funds. Category II covers private equity, private credit, real estate and fund of funds. Category III covers complex trading strategies including long-short equity, arbitrage and derivative-linked funds.

The categories differ in investment mandate, leverage permission, tax treatment, structure, liquidity and typical risk. Category I and II usually have pass-through taxation for non-business income and cannot use leverage for investment. Category III may use leverage within SEBI limits and may be taxed at fund level depending on structure.

Category II is the largest by committed corpus because it includes private equity, private credit, real estate and fund of funds. Category III has a large number of schemes and investors because many strategies operate in listed markets.

Category III AIFs use complex or diverse trading strategies, often in listed securities and derivatives. Common examples include long-only equity, long-short equity, arbitrage and market-neutral strategies. They may use leverage within SEBI limits.

Category II usually invests in private or unlisted assets such as private equity, private credit and real estate. It is close-ended and has pass-through taxation for non-business income. Category III usually focuses on listed-market or derivative-linked strategies, may be open-ended, may use leverage and may be taxed at fund level depending on structure.

Category I and II AIFs generally have pass-through tax treatment for non-business income under Section 115UB. Income is taxed in the investor's hands based on its nature. Category III does not get the same pass-through status and may be taxed at the fund level in many structures. Investors should check the fund tax note and consult a CA.

All three categories can carry high risk, but the type of risk differs. Category I has business survivability risk. Category II has credit, valuation and exit timing risk. Category III has market, strategy and leverage risk.

Yes. Category III AIFs are permitted to use leverage within SEBI limits, commonly discussed as up to 2x NAV. Category I and II AIFs are not permitted to use leverage for investment purposes, though operational borrowing may be allowed within permitted rules.

The minimum investment is generally Rs 1 crore for standard investors across AIF categories. Eligible employees or directors of the AIF or its manager may have a lower threshold, subject to applicable rules and fund documents.

Both Category I and Category II generally have pass-through tax treatment for non-business income under Section 115UB. There is no automatic category-level tax winner between the two. The actual tax outcome depends on the income type, such as capital gains, interest or dividend, and the investor's tax profile.

Disclaimer: This article is for educational purposes only. It does not constitute investment advice, tax advice, legal advice, a recommendation, or an offer to buy or sell any securities or financial instruments. AIF category details are based on SEBI (Alternative Investment Funds) Regulations, SEBI circulars/master circulars, Finance Act 2025 and publicly available AIF statistics. Please read all offer documents carefully and consult a qualified Chartered Accountant and a SEBI-registered investment adviser before making any investment decision.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Pitched a Category III AIF when you already have a PMS? Read the post-tax comparison befor...

SEBI’s March 2026 AIF reporting overhaul introduces an Annual Activity Report and a limi...

Learn how Alternative Investment Funds (AIFs) are taxed in India. A complete guide to Pass...

Learn what Alternative Investment Funds (AIFs) are, how they work in India, AIF categories...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...