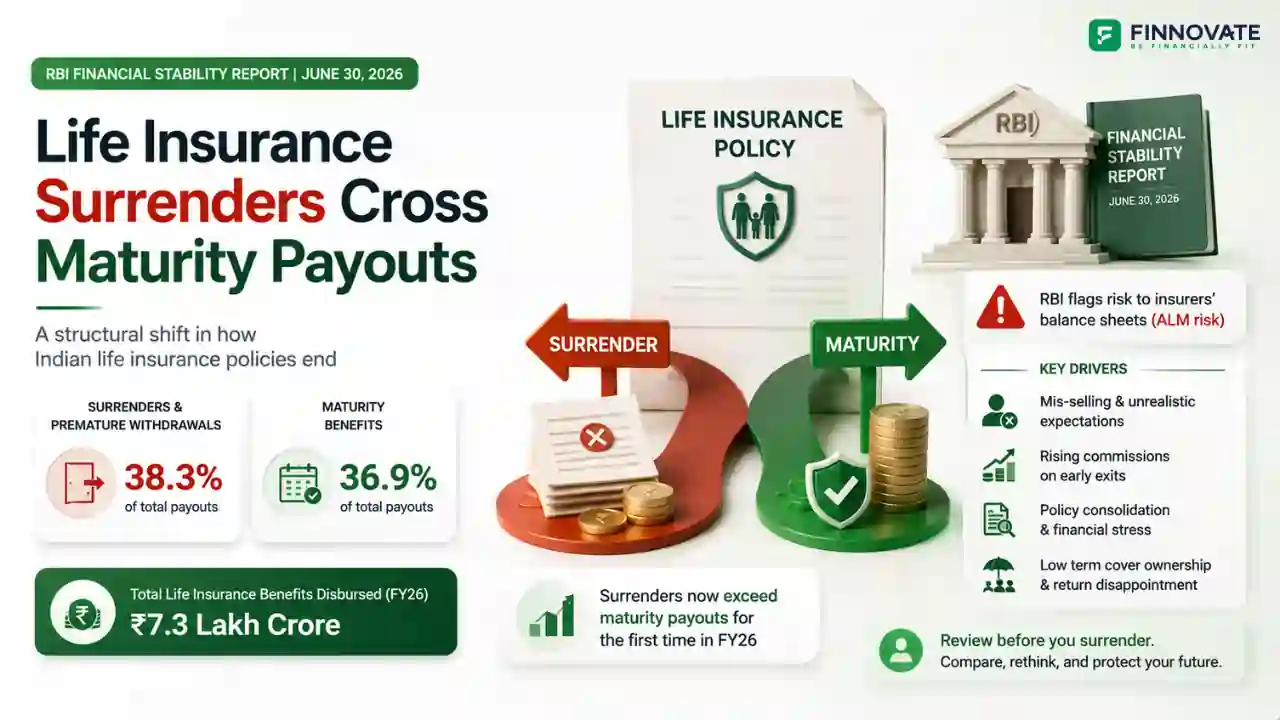

Life Insurance Surrenders Now Exceed Maturity Payouts in FY26

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

07 July 2026

When you think of financial planning, health insurance is one of the most critical pillars. But relying solely on your Mediclaim policy might leave gaps. With rising healthcare inflation and increasingly complex treatment procedures, it's crucial to think beyond just a traditional health policy.

Let’s explore why extra medical funds are essential and how you can systematically create them.

Your first line of defence is a comprehensive health insurance policy. Whether you opt for individual covers or a Family Floater, the objective is to mitigate hospitalization and treatment costs.

A Family Floater Plan is generally more economical, offering a larger shared cover for a lower premium. But remember, hospitalisation costs have skyrocketed, and inadequate coverage can derail your financial goals. That’s why health insurance forms the core of every good financial plan, but not the whole.

Here’s why you must build a backup medical corpus alongside your Mediclaim:

The hospital you visit during an emergency might not be on your insurer’s network. This means upfront payment before reimbursement.

Policy limits may get exhausted, especially with multiple hospitalisations within a year.

Many non-hospitalisation costs (like medicines, consumables, diagnostics) are not covered under standard policies.

Co-payments and deductibles mean you still pay a portion of the bill from your pocket.

So, how do you prepare for these out-of-pocket expenses?

Your emergency fund, typically 5–6 months’ income, acts as a financial buffer. Ideally, this fund should sit in liquid mutual funds or high-interest savings accounts for quick access.

Pro Tip: Always replenish the fund after usage to maintain its strength.

Leverage your Section 80D tax benefits for both your family and senior citizen parents. Here’s how:

If you claim ₹75,000 in deductions (₹25,000 for self/family + ₹50,000 for parents), and you fall in the 31.2% tax bracket, your annual tax savings = ₹23,400.

Invest that amount (₹2,000/month) in a balanced or hybrid mutual fund SIP @10% CAGR.

In 10 years, you’d build a corpus of ₹4.03 lakhs, without additional burden.

Today’s life insurance policies offer critical illness riders, which can cover major medical conditions like cancer, stroke, and heart attacks.

These riders are essential because:

Such illnesses involve long-term care and income loss.

Your health policy might not fully cover them.

Adding these riders is a cost-effective way to prepare for high-impact health events.

Super top-ups allow you to expand your health coverage without drastically increasing premiums.

For example:

Base policy: ₹5 lakhs

Super top-up: ₹25 lakhs (kicks in after ₹5 lakhs are used)

Total cover: ₹30 lakhs at a fraction of the standalone cost.

This also helps you preserve your no-claim bonus (NCB) and avoid buying entirely new policies for higher coverage.

Health insurance is the foundation, but true financial preparedness means building layers of safety — emergency funds, tax-optimised savings, strategic riders, and top-ups.

Think of it as a 360-degree health shield. Because when health issues arise, you want to be focused on recovery — not repayments.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare Term Insurance, Endowment, and ULIP in a clear, unbiased way. Understand costs, co...

Compare family floater vs individual health insurance in India - costs, coverage, pros & c...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...