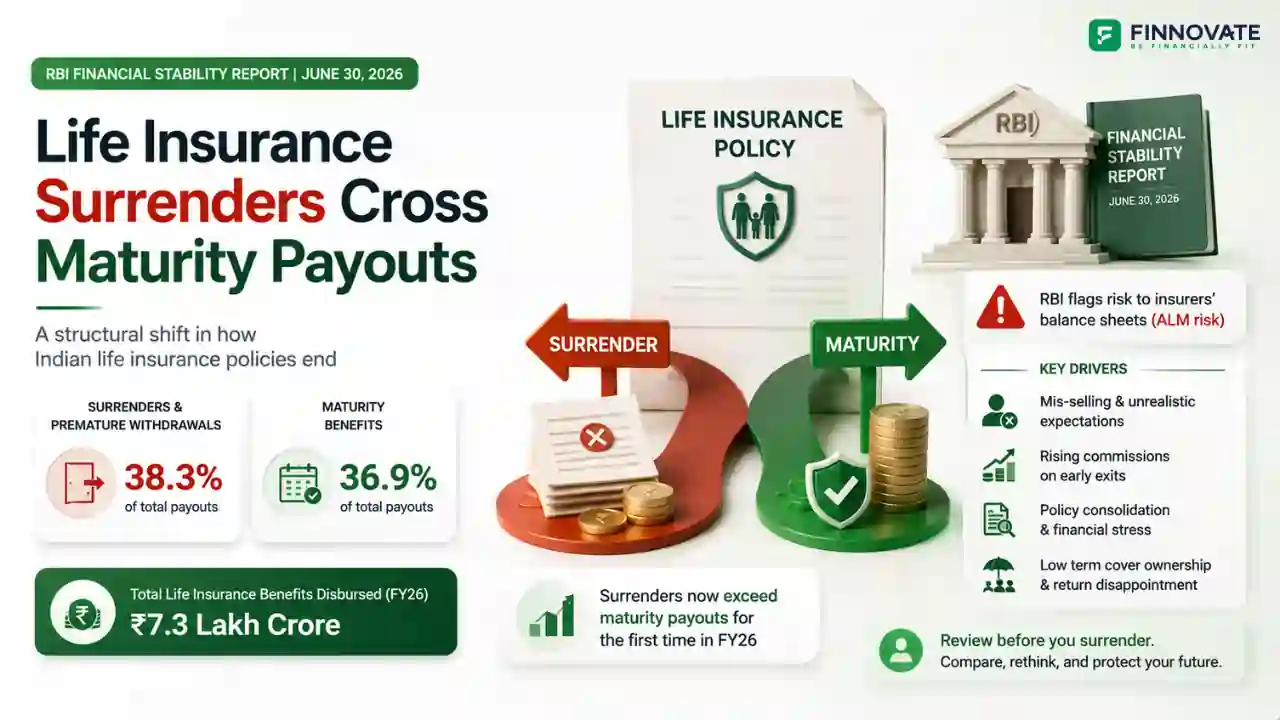

Life Insurance Surrenders Now Exceed Maturity Payouts in FY26

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

07 July 2026

In today's discussion with Radhika, Shantanu, and Priya, we explored the critical importance of investing for our life goals, like funding our children's education or planning for retirement. But before we dive into investing, it’s essential to first get risk out of our lives.

One of the main risks is income loss. If you're the primary earner in your family and something happens, what will your dependents do? To secure your family’s future, the first step is to identify:

We also discussed how to quantify risk using two methods:

This helps us determine the optimum amount of term insurance needed to replace lost income if something happens to the earning members of the family.

Next, we examined health insurance. It’s important to ensure that all dependents are covered with adequate health insurance. Relying on just your employer’s health insurance is not enough—having a personal health insurance policy is always a wise move. In case there’s a history of critical illness in your family, it’s a good idea to add a critical illness cover to your policy.

We also discussed the importance of having personal accident and disability cover. When we are young, the chance of loss of income due to accidents is higher than sickness, so having this coverage helps mitigate that risk.

To summarize, the key elements of a robust risk plan are:

With these measures in place, we can greatly reduce the risk that our families carry. In the next series, we will discuss an important topic in personal finance: estate planning.

Check out the video below for a detailed explanation of today’s discussion:

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Surrenders made up 38.3% of life insurance payouts in FY26, ahead of maturity benefits at ...

India's 2025 insurance law passed by Parliament didn't extend open architecture to individ...

Compare Term Insurance, Endowment, and ULIP in a clear, unbiased way. Understand costs, co...

Compare family floater vs individual health insurance in India - costs, coverage, pros & c...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...