Section 143(1) Intimation Explained: Refund, Demand and Next Steps

Received a Section 143(1) intimation? Understand CPC adjustments, refunds, tax demands, re...

24 July 2026

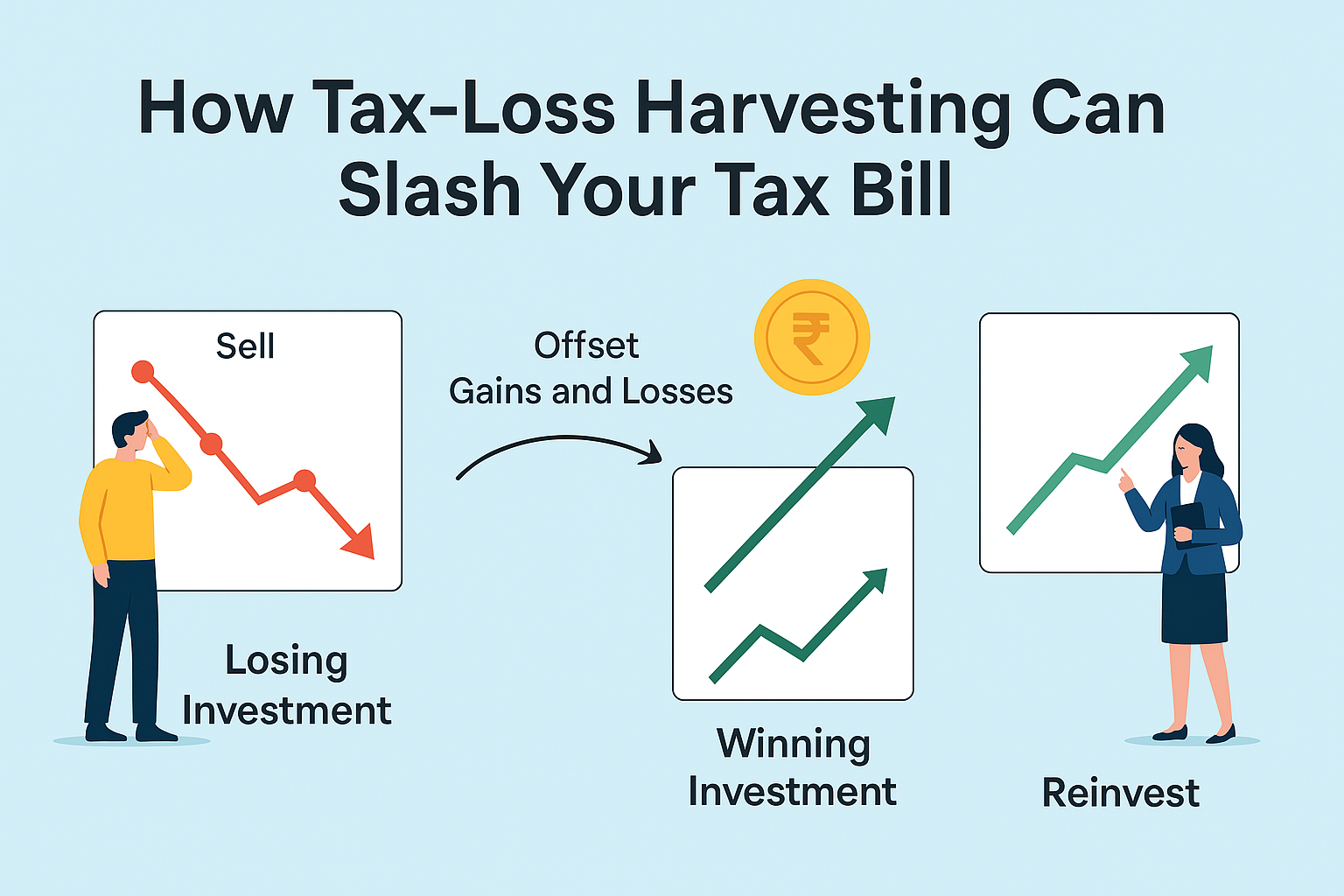

When investments fall in value, the instinct is to hold and wait. But selling a loss-making position before the financial year ends has a concrete tax benefit: that loss can reduce the tax payable on gains elsewhere in the portfolio. This is tax harvesting, or tax-loss harvesting.

It is not a loophole. It follows directly from how the Income Tax Act treats capital loss set-off and carry-forward. This guide covers how it works for both stocks and mutual funds, the rules that apply in FY 2025-26, and the situations where harvesting makes sense and where it does not.

Table of Contents

Tax harvesting is an umbrella term for two related strategies that use the capital gains framework of the Income Tax Act to manage tax liability.

Tax-loss harvesting means selling an investment that is currently below its purchase price, realising a capital loss. That loss can then be set off against capital gains realised elsewhere in the same financial year, reducing the net taxable gain. If losses exceed gains, the surplus can be carried forward for up to 8 assessment years.

Tax-gain harvesting (sometimes called tax-gain booking) means the opposite: selling a profitable long-term holding within the annual ₹1.25 lakh LTCG exemption threshold, paying zero tax on that gain, and reinvesting. This resets the cost of acquisition higher, reducing the taxable gain when the position is eventually sold for good.

Paper losses sitting on a demat account or an unredeemed mutual fund unit have no tax effect. The position must actually be sold before March 31 of the financial year for the loss to be available for set-off in that year.

The July 2024 Budget revised both the rates and the LTCG exemption threshold. The pre-2024 figures (STCG 15%, LTCG 10%, exemption ₹1 lakh) no longer apply. These are the current rates for transfers on or after July 23, 2024.

| Asset Type | Holding Period | STCG Rate | LTCG Rate | Annual Exemption |

|---|---|---|---|---|

| Listed equity shares, equity MFs, business trust units (STT paid) | STCG: up to 12 months; LTCG: more than 12 months | 20% (Section 111A) | 12.5% (Section 112A) | ₹1.25 lakh on LTCG only |

| Other assets: gold, property, unlisted shares | STCG: up to 24 months; LTCG: more than 24 months | Slab rate | 12.5% without indexation (Section 112) | None |

| Debt-oriented MFs (Section 50AA: over 65% debt exposure) | Any holding period | Slab rate regardless of holding period | None | |

All rates are base rates before surcharge and 4% cess. The ₹1.25 lakh exemption applies only to equity LTCG under Section 112A. Debt-oriented MF gains are taxed at the investor's applicable income tax slab rate, which means the tax saved per rupee of debt fund loss depends on the investor's slab, not a fixed rate.

The Income Tax Act specifies exactly which losses can be used against which gains. The rules are not symmetric, and getting them wrong is one of the most common errors in ITR filing.

| Loss Type | Can Set Off Against | Cannot Set Off Against |

|---|---|---|

| Short-Term Capital Loss (STCL) from stocks or MFs | Both STCG and LTCG (any asset class, same head) | Salary, business income, rental income, or any other income head |

| Long-Term Capital Loss (LTCL) from stocks or MFs | LTCG only | STCG, salary, business income, or any other income head |

| MF loss (equity) vs stock gain | Yes. Cross-asset set-off is allowed within the same STCL/LTCL rules. A mutual fund STCL can offset stock STCG or LTCG; an MF LTCL can offset stock LTCG | Same restrictions as above apply |

| F&O losses (non-speculative business loss under Section 43(5)) | Any income head except salary, including capital gains, within the same year | Salary income; cannot be carried forward if ITR is filed late |

| Intraday / speculative trading losses | Speculative income only (intraday profits) | Capital gains, salary, or any other head |

Neither STCL nor LTCL can reduce salary, business income, rental income, or income from other sources. This is a firm rule under Section 74 of the Income Tax Act. Capital losses stay within the capital gains head only.

If capital losses are not fully absorbed in the year they arise, the unabsorbed amount carries forward to future years.

Mutual fund capital losses follow the same STCL and LTCL rules as direct equity. An equity MF held for 12 months or less generates STCL on sale at a loss; held for more than 12 months, it generates LTCL. Cross-asset set-off is permitted: a mutual fund loss can offset a stock gain, and a stock loss can offset a mutual fund gain, provided the STCL/LTCL classification is respected.

A switch instruction, even within the same AMC, counts as a full redemption followed by a fresh purchase for tax purposes. The gain or loss is crystallised in the year of the switch, not when the new units are eventually sold.

Equity funds held under one year typically carry a 1% exit load. This cost directly reduces the net tax saving. Factor it into the calculation before deciding whether selling is worthwhile.

Each SIP instalment is a separate acquisition lot with its own date, NAV, and holding period. The overall fund value can be positive while units purchased at elevated NAVs are sitting in loss. This creates harvesting opportunities even in broadly rising markets, particularly for SIP portfolios that have been running for two or more years.

Redemptions follow FIFO: the oldest units are always sold first. Within a single folio, there is no mechanism to skip older units and redeem only recent ones. This matters because older units in a long-running SIP tend to be in profit. A standard redemption from such a folio will typically crystallise a gain, not a loss.

The practical check: before any redemption, pull the lot-wise capital gains report from the broker or AMC (Zerodha Console, Groww P&L, or a CAMS/KFintech statement). This shows exactly which units FIFO will sell first and whether they are in profit or loss. Where the FIFO units are in loss, harvesting is straightforward. Where they are in profit, a partial redemption or a folio-specific approach may be needed, and a Chartered Accountant's guidance is worth seeking.

| Item | Amount |

|---|---|

| STCG from Stock A (sold after 8 months) | ₹50,000 |

| STCL from Stock B (sold after 9 months, at a loss) | (₹30,000) |

| Net taxable STCG | ₹20,000 |

| STCG tax at 20% | ₹4,000 |

| STCG tax without harvesting | ₹10,000 |

| Tax saved by harvesting | ₹6,000 |

A salaried investor in FY 2025-26 has the following capital gains position before harvesting:

| Item | Before Harvesting | After Harvesting |

|---|---|---|

| LTCG from Nifty index fund (held 18 months) | ₹2,50,000 | ₹2,50,000 |

| LTCL from sectoral fund (held 15 months, underperformed) | Not realised | (₹80,000) realised |

| Net LTCG after LTCL set-off | ₹2,50,000 | ₹1,70,000 |

| Less: ₹1.25L annual exemption (Section 112A) | (₹1,25,000) | (₹1,25,000) |

| Taxable LTCG | ₹1,25,000 | ₹45,000 |

| LTCG tax at 12.5% | ₹15,625 | ₹5,625 |

| Tax saved by harvesting | ₹10,000 | |

Note: Brought-forward losses from prior years (if any) would be set off before the ₹1.25 lakh exemption is applied. Confirm the exact sequencing with a Chartered Accountant.

| Item | Detail |

|---|---|

| Investor's LTCG position mid-year from a large-cap fund | ₹1,10,000 (below ₹1.25L threshold) |

| Tax payable on this LTCG | Nil (within exemption) |

| Action: sell the units, book the ₹1,10,000 gain, reinvest immediately | New cost base is now the higher current NAV |

| Benefit: future gain is computed from the new higher cost | Reduces future taxable LTCG when eventually sold |

| Tax paid now | Nil |

This strategy is most effective when done annually and consistently. The ₹1.25 lakh exemption resets every financial year and cannot be carried forward if unused.

For long-term equity investors, the annual ₹1.25 lakh LTCG exemption under Section 112A is a recurring planning tool. Selling profitable holdings up to this threshold each year, paying zero tax, and immediately reinvesting resets the cost of acquisition without any tax outgo. Over multiple years this progressively reduces the taxable embedded gain in the portfolio.

The exemption applies per financial year and cannot be accumulated or carried forward. An investor who does not use it in a year simply loses that year's benefit.

Tax harvesting is a mathematical exercise, not a ritual. The decision should be driven by actual numbers, not calendar proximity to March 31.

The basic calculation: estimated tax saving = loss to be harvested multiplied by the applicable rate (20% for STCG, 12.5% for LTCG, or slab rate for debt MFs). From this, subtract all transaction costs: brokerage, STT, GST on brokerage, and any exit load. If the net figure is positive and meaningful relative to the effort, harvesting makes sense.

| Harvest | Skip |

|---|---|

| You have meaningful STCG taxable at 20% to offset | Your only gains are LTCG below ₹1.25 lakh (nothing taxable to offset) |

| You have LTCG above ₹1.25 lakh and an LTCL available | You have LTCL but no LTCG to use it against this year |

| Transaction costs are clearly less than the tax saved | Exit loads, STT, and brokerage exceed the tax benefit |

| A similar substitute investment is available to maintain exposure | Selling permanently exits a high-conviction position with no good substitute |

| The loss-making holding is near its short-term threshold (selling now books STCL, which is more flexible) | Selling resets a holding that is close to crossing the 12-month LTCG threshold (converts future LTCG at 12.5% into STCG at 20%) |

| You have debt MF losses and are in the 30% slab (each ₹1L of loss saves ₹30,000) | Your income is below the basic exemption and you pay no capital gains tax anyway |

The worst approach is harvesting automatically every March without checking whether you have taxable gains to offset, whether the loss type matches the gain type, or whether selling will convert future LTCG into STCG.

Tax harvesting decisions depend on your full portfolio, income level, and existing carry-forward losses. Our advisory team can help you map the right approach for your specific situation.

Book a Tax Planning CallTax harvesting means using realised capital losses to reduce the tax you pay on capital gains in the same financial year. If you have made profits on some investments and losses on others, you can sell the loss-making ones before March 31 to offset the gains and pay tax on the net amount rather than the gross profit. The term also covers tax-gain harvesting, where you book profitable long-term gains within the annual ₹1.25 lakh LTCG exemption to reset your cost base tax-free.

Yes. Capital losses and capital gains fall under the same income head regardless of whether the instrument is a stock or a mutual fund. A mutual fund STCL can offset stock STCG or LTCG. A mutual fund LTCL can offset stock LTCG. The STCL/LTCL rules apply to the loss, not to the instrument type.

The set-off rules are the same. The practical differences are in execution. Mutual fund redemptions follow FIFO, which means a blanket redemption often crystallises gains from older units rather than losses from recent ones. For SIP portfolios, a targeted redemption of only the loss-making lots is needed. Mutual funds also carry exit loads (typically 1% for equity funds held under a year) which reduce the net benefit. Switches between schemes are treated as redemptions for tax purposes even within the same AMC.

Yes, and SIP portfolios often have more harvesting opportunities than lump-sum investments. Each SIP instalment is a separate acquisition lot with its own date and NAV. Units purchased at higher NAVs during market peaks may be in loss even if the overall fund has gained. Reviewing the lot-wise breakdown on the broker or AMC portal before redeeming allows a SIP investor to identify and redeem only the loss-making tranches while leaving the profitable lots intact.

No, not under the current Income Tax Act 1961 for FY 2025-26. Long-term capital losses can only be set off against long-term capital gains. They cannot reduce short-term gains. The final enacted Income Tax Act 2025 preserves this same restriction for brought-forward losses through its savings clause, which requires adherence to the old-Act set-off rules.

Both STCL and LTCL can be carried forward for up to 8 assessment years from the assessment year in which the loss was first computed. The condition is that the ITR for the loss year must be filed by the due date under Section 139(1). A late return forfeits carry-forward for that year's losses permanently.

The annual exemption under Section 112A for LTCG from listed equity shares, equity-oriented mutual funds, and business trust units is ₹1.25 lakh per financial year. Gains up to this amount in a year are tax-free. This was revised upward from ₹1 lakh effective July 23, 2024 and applies only to LTCG under Section 112A, not to STCG or to LTCG on other assets.

No. Capital losses, whether short-term or long-term, can only be set off against capital gains. They cannot reduce salary, business income, rental income, or income from other sources. F&O losses are treated differently: they are classified as non-speculative business losses and can be set off against most income heads except salary within the same financial year.

Yes. Tax harvesting follows directly from the set-off and carry-forward provisions of the Income Tax Act, 1961. It is a recognised and legal approach to managing capital gains tax liability. The tax department has not challenged ordinary tax-loss harvesting by individual investors. The relevant caution is GAAR (General Anti-Avoidance Rules), which applies to artificial arrangements with no genuine economic substance. This is not triggered by standard year-end harvesting of genuine portfolio losses.

Disclaimer: This article is for general information and educational purposes only. It does not constitute investment advice, tax advice, or a recommendation to buy, sell, or hold any security or fund. Capital gains tax rates, set-off rules, and carry-forward provisions described here are based on the Income Tax Act, 1961 as amended, applicable for FY 2025-26 (AY 2026-27). The final enacted Income Tax Act 2025 preserves the Section 74 set-off restrictions for brought-forward losses; the broader transitional relief proposed in the draft Bill did not become law. Tax rules may change in subsequent budgets or notifications. Please consult a qualified Chartered Accountant or SEBI-registered investment adviser before making any tax-related or investment decision.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Received a Section 143(1) intimation? Understand CPC adjustments, refunds, tax demands, re...

Zero tax on a ₹14.65 lakh salary is real, but only if your employer contributes EPF on f...

Changed jobs in FY 2025-26? See why combining two Form 16s can create a tax shortfall past...

Compare ESOP vs RSU taxation in India: perquisite tax, capital gains, TDS rules, and the n...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...