Why India Is Buying More Oil on the Spot Market After the 2026 Middle East Crisis

India's crude imports shifted fast after the 2026 Iran war. Russia's share hit 52-54% by J...

09 July 2026

What

exactly is the yield curve?

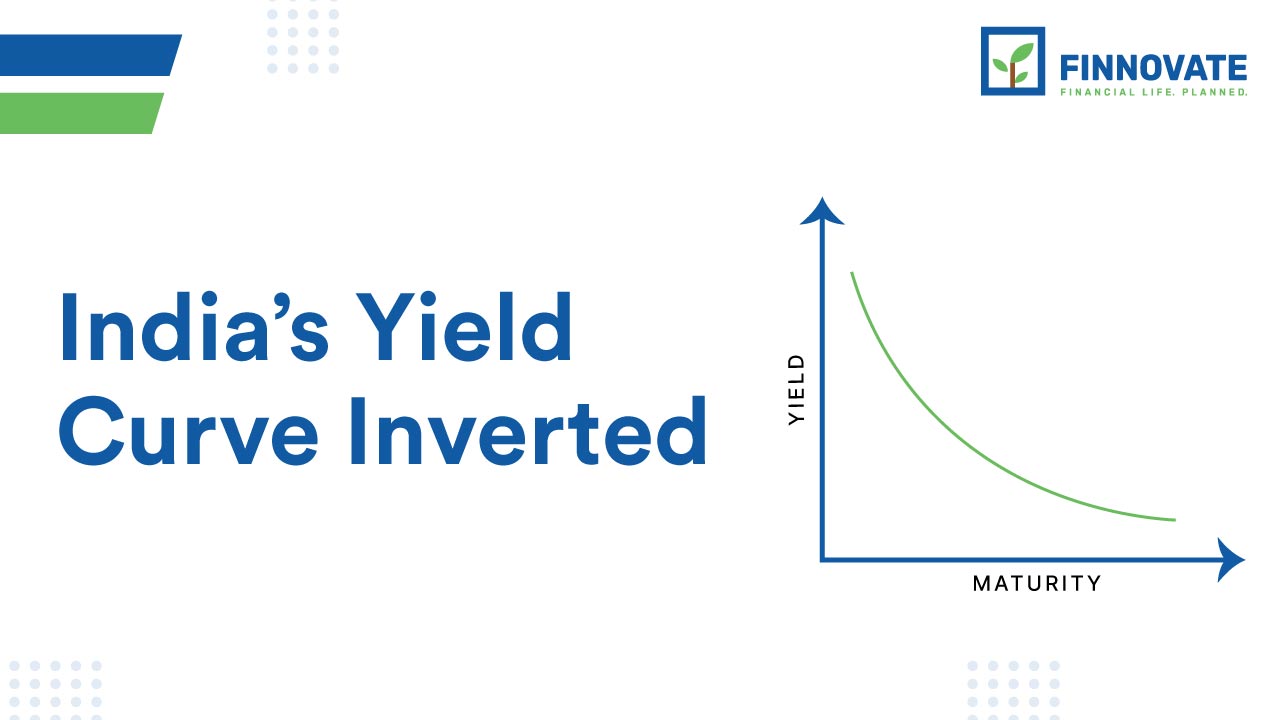

Yield curve is the relationship between the yield on bonds and its tenure. This yield curve is normally upwards sloping since longer tenure bonds carry more of risk and hence the yields are higher as compared to shorter tenure bonds. The positive slope of the yield curve shows this relationship. We are talking of a positive slope to the yield curve in the normal market conditions. However, in any market there are exceptions and the inversion of yield curve is an exception.

Why does yield invert?

Before we get to the reasons for the inversion of yield curve, how exactly is inversion measured? As yield inversion is hard to measure, most markets use a proxy like the spread of short tenure bonds over long tenure bonds. In India, the normal benchmark is the spread between the 364-day treasury bill yield and the benchmark 10-year bond yield. Last week, this spread turned negative, with the yield on the 364-day treasury bill going marginally above the 10-year bond yield, when it touched 7.48%. The 364-day T-Bill yield in India has rallied from 6.9% to 7.48% in 2023, while the 10-year yield has been tad rangebound.

What

does inversion indicate?

Studies in the US have shown that the yield curve inverts a couple of quarters ahead of an actual economic slowdown. Interestingly, this relationship has held in majority of the cases in the last 100 years, which is what gives this measure some degree of credibility. Also, in the Indian context, the inversion of yield curve happened for the first time since the year 2015. Normally, the yield curve gets inverted when the demand for the bonds at the short end of the yield curve is much more than the demand for bonds at the long end. That would normally happen only when the level of confidence in the long-term investing in bonds is weak; which may be the case.

Is yield curve inversion a worry?

In the Indian context this yield curve inversion may not be that simple. For starters, India has a rather distorted yield curve. For instance, we have risk-free instruments like government small savings schemes. These not only offer higher rates, but the tax breaks on such bonds under Section 80C tends to make them inordinately high-yielding debt investments. Secondly, though the Indian debt markets are well over $1 trillion, the trading depth and liquidity is still too narrow. Hence, the pricing may be driven by just a handful of highly influential players. Yield curve may not be that simple in India, but the signal cannot really be ignored at this time.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No comments yet. Start the conversation. What would you add?

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

India's crude imports shifted fast after the 2026 Iran war. Russia's share hit 52-54% by J...

FPIs sold $5.21 billion from Indian equities in June 2026. But BFSI turned net buyer at $3...

Amazon Now is targeting 100 Indian cities with 1,000+ micro-fulfilment centres. But the re...

RBI replaced its NBFC-UL scoring system with a single ₹1 lakh crore asset test on June 2...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...