Wealth Creation in India: Meaning, Strategies, Examples & How to Start

Learn what wealth creation means, why saving isn't enough, and how to build long-term weal...

05 August 2025

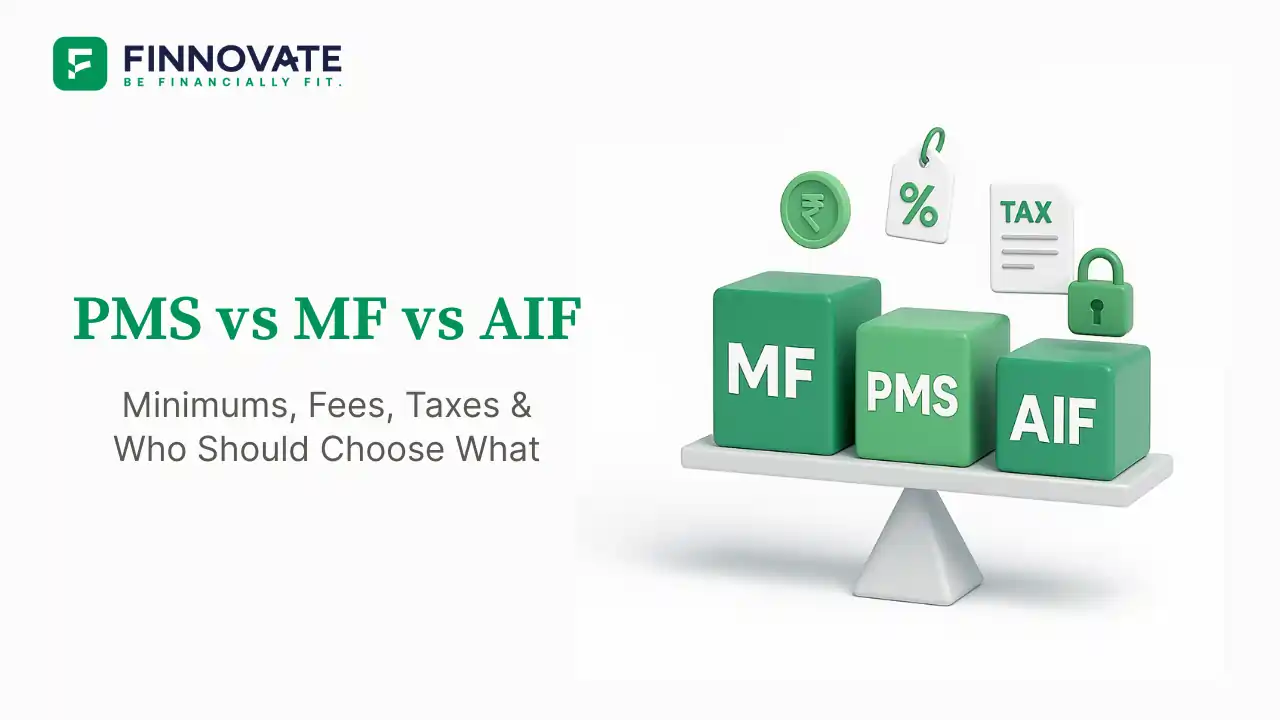

Many investors hear “Mutual Fund, PMS, AIF” and feel lost. This guide explains the basics, minimum amounts, fees, taxes, liquidity, and who each option suits. By the end, you’ll know which bucket to explore first.

Education only. This is not investment, legal, or tax advice.

A pooled product for retail investors. You can start small, even with a SIP. A fund manager invests for many investors together.

Your money buys shares and other securities that sit in your own demat or account, managed by a professional. The minimum ticket is high.

A pooled product for larger investors using specialised strategies such as private equity, credit, or long–short. The fund document (PPM) lists fees, risks, and rules.

The minimums are very different. Mutual funds let you start small. PMS and AIF are built for larger cheques. Read the idea first, then confirm numbers in the table.

| Product | Minimum investment | Notes |

|---|---|---|

| Mutual Fund | ₹100–₹500 (typical SIP) | Retail product; easy start |

| PMS | ₹50,00,000 | Regulatory minimum |

| AIF (Cat I/II/III) | ₹1,00,00,000 | PPM may specify exceptions (e.g., employees/directors). Check latest terms. |

Note: Some accredited or special cases may follow different thresholds. Always check the fund’s latest PPM and SEBI circulars.

Fees change your net returns. Compare what is charged and how it is shown to you.

You pay an all-in fee called the Total Expense Ratio (TER) inside the fund. It is already reflected in the NAV, so you do not see a separate bill.

Common items are a yearly management fee, a performance fee (over a hurdle, often with a high-water mark), brokerage, custody, audit, and GST on fees.

Tip: Ask for a one-page fee illustration showing your capital, the hurdle, when performance fees start, and every other cost.

Fees include a management fee and a performance fee (carry) as per a distribution waterfall shown in the PPM. All fees and expenses must be disclosed in the PPM. Read this section line-by-line.

India simplified capital-gains slabs in July 2024. Rates differ for short-term and long-term gains. The date of sale matters.

| Instrument | STCG | LTCG | Notes |

|---|---|---|---|

| Equity MF / Listed equity / PMS equity (eligible under 112A) | 20% | 12.5% over a ₹1.25 lakh annual exemption | Applies where equity conditions (like STT) are met |

| AIF Category I/II | Investor-level (pass-through for most income) | Investor-level | Business income, if any, may be taxed at fund level |

| AIF Category III | Fund-level tax | Fund-level tax | Distributions to investors are usually post-tax |

What to remember: Sales before July 23, 2024 follow old rates; sales on or after that date follow the new 20% / 12.5% rule (with the higher ₹1.25 lakh LTCG exemption for eligible equity).

High liquidity in open-ended schemes. Daily NAV and factsheets make tracking simple.

High transparency. Holdings sit in your demat and cash account, managed on your behalf. Exits are normal market trades; product lock-ins are uncommon (check your agreement for exit loads, if any).

Often close-ended with a fixed tenure or lock-ins. Statements are periodic. Treat it like a long-term commitment.

| Feature | Mutual Fund | PMS | AIF |

|---|---|---|---|

| Minimum ticket | ₹100–₹500 (SIP) | ₹50L | ₹1Cr |

| Fees | TER inside NAV | Mgmt% + Perf% + costs | Mgmt% + Carry + costs |

| Reporting | Factsheets / NAV | Full holdings via demat and statements | PPM-driven statements |

| Liquidity | High (open-ended) | Market-linked; no typical product lock-in | Low–Medium (tenure / lock-ins common) |

Assume ₹50 lakh invested for one year in an equity strategy. These are sample numbers to show the flow. Your fee letter and tax profile decide actual results.

Note: For PMS and AIF, always review a tabular fee illustration and the latest tax memo before investing.

PMS, Mutual Funds, and AIFs all serve different investor needs. The right choice depends on your investment size, tax strategy, and long-term goals. Get a one-on-one consultation to identify what works best for you.

Schedule a Call With Our ExpertsThere is no single winner. PMS suits larger portfolios that want customisation and direct ownership. Mutual funds suit smaller, simpler, and more liquid needs. For a more detailed one-on-one comparison, read our blog on Mutual Fund vs PMS

Usually no. ₹50 lakh is the current regulatory minimum.

Typically ₹1 crore. Some special cases exist as defined in the PPM or latest rules. Always check the latest document.

Like listed equity when conditions are met: STCG 20%, LTCG 12.5%, with a ₹1.25 lakh annual exemption for eligible equity gains.

Generally no. Category III AIFs are typically taxed at the fund level. Investors receive post-tax distributions.

Disclaimer: This article is for education only. It is not investment, legal, or tax advice. Tax treatments depend on your facts and can change with law. Please consult a SEBI-registered professional.

No spam. Only new posts, simple explainers, and practical money checklists for busy professionals.

Finnovate is a SEBI-registered financial planning firm that helps professionals bring structure and purpose to their money. Over 3,500+ families have trusted our disciplined process to plan their goals - safely, surely, and swiftly.

Our team constantly tracks market trends, policy changes, and investment opportunities like the ones featured in this Weekly Capsule - to help you make informed, confident financial decisions.

Learn more about our approach and how we work with you:

No spam. Only new posts, simple explainers, and practical money checklists.

You may also like

Learn what wealth creation means, why saving isn't enough, and how to build long-term weal...

Confused between wealth and asset management? Learn the key differences, practical example...

Explore the differences between DIY and professional wealth management. Learn the benefits...

Financial planning vs wealth management explained in simple words - differences, who needs...

Popular now

Learn how to easily download your NSDL CAS Statement in PDF format with our step-by-step g...

Learn what SIF investment means in India, SEBI rules, Rs 10 lakh minimum investment, avail...

Looking for the best financial freedom books? Here’s a handpicked 2026 reading list with...

Clear guide to mutual fund taxation in India for FY 2025–26 after July 2024 changes: equ...